Activision-Blizzard $ATVI

Is ATVI a great business in a temporary fiasco?

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

What they do

Activision-Blizzard is a well known publisher and developer of video games. The company was the result of a merger between Activision and Vivendi Games in 2008. It’s publicly traded on the Nasdaq under the ticker symbol ATVI 0.00%↑. It has a market cap around 50 billion USD and an enterprise value around 42 billion USD.

The business operates as a holding company for the 5 major business units:

Activision Publishing - the original Activision video game publishing and development business most known for the Call of Duty franchise

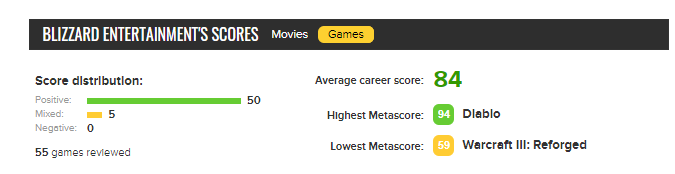

Blizzard Entertainment - game developer most known for Starcraft, Warcraft, Hearthstone, Overwatch and Diablo series

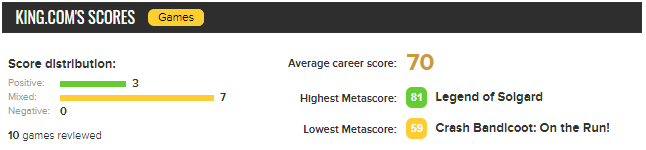

King - social game developer and publisher best known for Candy Crush Saga

Major League Gaming - esports professional gaming league

Activision Blizzard Studios - TV and film studio (rather insignificant)

Recent troubles

The management team and the board has gotten themselves in a world of trouble recently. There have been several lawsuits, staff protests and an SEC investigation. The nature of the problem is harassment and a terrible and potentially unsafe work environment for its staff. The allegations span many years and involve top management, including top executives such as the CEO, Bobby Kotick.

Kotick has initially had the support of the board, despite it being quite clear that he has overseen this culture for quite a long time. He has been the CEO for 30 years since acquiring a major stake in Activision in 1991. Apparently, he needed more than 3 decades to learn to do better and has promised to make things right going forward. Mr. Kotick owns just shy of 4 million shares that he has been granted or purchased over his tenure.

Given the nature and severity of the accusations, it’s hard to imagine a real turnaround with the current board and CEO still there. If there’s a path to success in ATVI’s future, it certainly doesn’t involve Kotick and his buddies. He has recently claimed he’s willing to step aside if he can’t fix things quickly. I’m not sure what that means as he’s obviously part of the problem.

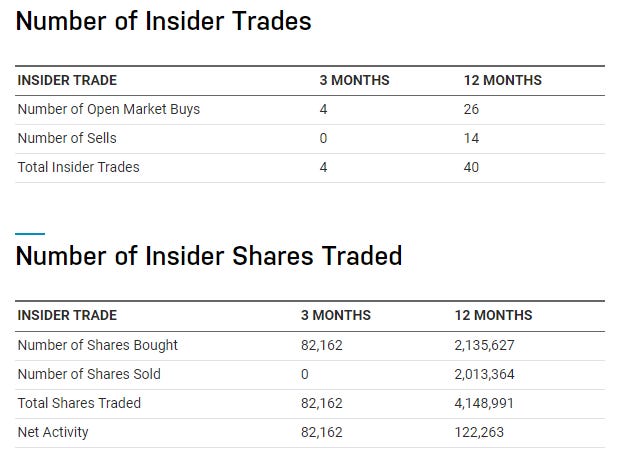

Insiders haven’t been selling in the last few months and have actually bought some shares with the recent price drop. Over the past year, there has been buying and selling.

Financials

Past decade revenue growth rate has been 11% per year.

Gross margins have been increasing from 35% to 70% as sales have moved more and more digital and there is tremendous operating leverage in the industry, as long as your game is a reasonably sized hit. As soon as the development and marketing costs are covered, every marginal sale is pure profit (more or less). Adding to this is the benefit of King’s mobile games around Candy Crush Saga which are cash cows. In addition, there has been the trend of successful games having long legs, filled with lots of microtransactions and season passes, of which Call of Duty and some Blizzard games have excelled at.

Return on invested capital has not been as high as one might hope at around 10-15%. This is likely a reflection of games being hit-or-miss and some taking larger investments than originally planned. They may need to look to acquisitions to fuel more growth going forward, and they have the cash to do it.

The balance sheet is net cash. Currently, the company is sitting on 9 Billion in cash with no short term debt and around 3 billion in long term debt. As it is expected that the businesses will continue to generate cash even through a mediocre output of new games, you can expect the cash to build until they find a good home for it. At this point, it would seem development acquisitions or a stock buyback would be good places to deploy some of this cash.

The share count has been relatively steady over the past decade or so. They did repurchase a sizeable amount of shares from 2009-2013 so there is a history of this capital allocation lever being pulled when deemed appropriate.

The dividend policy has been impressive. In 2010, the first year of dividends, there was 0.15$/share and this has grown at around 10% a year to present at around 0.47$/share. The current yield is 0.75% with the stock around 60$.

The current strength of the balance sheet, coupled with some reasonably good growth rates that should be able to be sustained for another while, seems like a low risk. With the cash, I would hope for good opportunities to grow via acquisitions but that might be a low return in today’s expensive and competitive world in the video game industry. Perhaps the best way to get returns is via an aggressive buyback program.

Operational metrics tracked include monthly active users (MAUs). As you can see, they are seasonal and have been flat year over year, which you would think is not a good sign. But if you consider the amount of lockdowns and lack of social gatherings in 2020 for these numbers to be in the same ballpark after 2020, is great. I wouldn’t expect amazing growth over the next year if re-openings continue but if they can maintain these metrics and improve gradually in the future, they will be doing well.

Moat - driven by IP

Blizzard Universe of IP - Diablo, World of Warcraft and Overwatch, among others is the Blizzard world of characters. They have traditionally been the masters of long life games where dedicated fans play for hundreds and even thousands of hours. The creativity in these universes is second to none and I believe this is a quality that is very difficult to replicate. If the world is moving to the metaverse, it would be hard to imagine that there isn’t a lot of value in these brands and properties.

Overwatch is the newest of these and has a sequel and a potential mobile game coming out soon. Sequels often don’t get the excitement of critics but often times, fans dish out lots of cold hard cash for these.

Diablo has a 4th game slated to come out next year and has been long awaited. Time will tell if it does well. The other properties have been getting retro treatments with remakes, etc. to mixed reviews.

Candy Crush Saga - There are definitely hardcore candy crush players that put hours of time into the game. Let’s just be honest, it’s an addictive cash cow. Whether you think it’s a fine piece of “art” in the video game world is really not the point.

Beyond candy crush saga, King hasn’t made significantly blockbuster hits to mention. They have been steadily bringing in around 2 billion in revenue since the creation of the game in 2012. Impressive, but don’t expect a slew of new blockbusters to ramp up growth from them.

Activision IP aka Call of Duty - the COD franchise has dominated first person shooters and has evolved over time to keep up with the trends in the industry. There is a loyal fanbase of hardcore and casual players. There is a strong esports presence and that trend is likely to continue.

The microtransactions and extra special editions and season passes have contributed significantly to the revenue and profit margins over the past decade. I would expect this continues as it is normalized but at a lower growth rate than in the past as competition becomes mature.

There is no doubt that Activision’s studios has not been able to get the same level of fandom as Blizzard but they have been super-successful despite this. The only other significantly successful series from them has been the Tony Hawk’s Pro Skater series which will never sell like a first person shooter or MMO/RPG.

Valuation and return potential

The driver for returns from here will be continued trust in the brand and good content from their studios. If the stock price stays low for a while, there is also a real opportunity to drive value via buybacks and dividend growth.

At the time of writing, the stock price sits around 60$. It has a p/e of 18, a p/s of 5 and EV/EBIT of 13. Whichever way you slice it, the business is on sale relative to its recent past as well as its competition. For comparison sake, Take-Two and EA sell for around 2X those multiples of earnings.

That being said, I don’t think this price is so cheap yet that it is providing adequate margin of safety by itself. I’d want to see signs of operational execution and management changes to address the current and longstanding issues with employees. On an absolute basis, the price you are paying is fair but not unprecedented for this business (not the deal of a lifetime it might initially seem like if you only look at a 12 month stock chart).

The million dollar question - “is this temporary?”

While the troubles are serious and a problem for all stakeholders in the business including shareholders and employees, I believe there will be an opportunity to right the ship if the Management team and some or all of the board is replaced. Otherwise, there will be a lot of stink in the air and it will be very difficult (not impossible). This is certainly not something I can predict, but those are the signs that I would look for. I would also look to any big name talent at the studios and what they do. These would be the creative directors and producers, etc. If top talent is willing to stay and/or move to Activision-Blizzard, that likely says a lot. If they are heading for the exits, that’s also a telling sign.

Note: I don’t own any shares of ATVI at the time of writing (November 2021).

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

If you liked what you have read, please share, comment, and tell your friends. I’m always looking for feedback on my ideas and writing so please follow me on twitter as well! I’m @MoS_Investing on twitter.

Thanks,

Simon