Atlas Engineered Products $AEP.V

Truss me; you’ll want to read this

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

DISCLOSURE: Please note that I own shares in Atlas Engineered Products. This is only a discussion of my current thoughts on the business and is not advice of any kind.

Some people might be reluctant to look at the serial acquirers because they believe acquisitions often destroy value. I held this view myself for a long time. I unlearned it when I started to study companies that had great success acquiring other companies -- lots of other companies over a long period of time.

- Chris Mayer, Woodlock House Family Capital

Atlas Engineered Products is a microcap listed on the TSX Venture exchange. It has a market cap of roughly 50 million CAD and enterprise value a few million more. It is founder led and is a serial acquirer rolling up a very fragmented industry. Needless to say, the stock is thinly traded so this is not for the quick hand trader.

Atlas was founded in 1999 by its current CEO and was taken public in 2017 as a reverse takeover on the venture exchange. The company owns 7 separate manufacturing locations across Canada that it has acquired. The company operates in a traditionally low tech, fragmented industry exposed primarily to new residential construction but also is correlated to renovations and smaller commercial and light-industrial and agriculture related construction

.

The company designs, builds and distributes engineered wood products. The primary products consist of roof trusses but are expanding with the industry to include more and more prefab construction components including floor trusses, wall panels and joists.

Rollup a Fragmented Industry

Estimates have Atlas at around 2% of a 2.5 billion dollar market. The market of truss manufacturers is fragmented partly due to the high costs in shipping large heavy products like roof trusses over long distances. For these reason, these businesses are very regional, local even. While there aren’t high barriers to entry, the local market is the extent of the business for most players so they tend to be small for this reason alone. Because of their small size, they are often underinvested, under-utilized and cannot compete with scaled operations such as Atlas which has a network to cover some of the expenses as well as expertise in both design, sales and operating practices.

Atlas themselves are still small and can be patient and buy up small businesses for 10’s of millions at low multiples where there isn’t much capital chasing these deals. Needless to say, the opportunity set is large. And that is just in Canada. They could eventually do the same thing south of the border, should they chose to do so.

Canadian Housing Crunch

With a rising interest rate environment, housing has certainly cooled in Canada. This means that growth rates for new construction has slowed but likely not as much as resale volume. The demand for housing in Canada are not expected to slow over the next decade due to immigration and other factors like a cohort of millennials and younger people needing to move out.

Its really too early to tell how long and to what extent the housing dip will take hold. New construction has dropped but not as much as the drop in price might suggest as these are mostly resale prices. Regardless of all this, its important to remember that Atlas is exposed primarily to new construction, not resale, and the price is not as AS significant as its an input cost tied to demand. Price is much more impactful on home builders’ margins, although this will pressure prices for trusses.

A risk to be sure. Probably a short term impact.

Tailwinds

Canada has high hopes for growth with immigration over the next decade. There is an added demand for housing that is caused by a glut of 20 something year olds moving out from the nest. There may be a short term risk of a housing shock but in the longer term, more residential housing is needed. Coupled with a constrained housing supply will make not only new housing starts rise but will also make prefab construction ever more valuable as it will continue to grow share of the construction techniques.

Buy Low and Improve

Atlas has been able to pay an average price of 4x EBITDA for acquisitions. These are mature, small, unsophisticated business operations. They are able to take advantage of a lack of succession and a lack of drive to grow the business in the smaller businesses that they will target. They are able to add sales teams, take advantage of expertise and best practice, introduce efficiencies in operations that reduce costs and add to the capacity of the assets. In addition, Atlas is able to offer engineering services and a wider array of tangentially related products which should also help get return customers and larger clients.

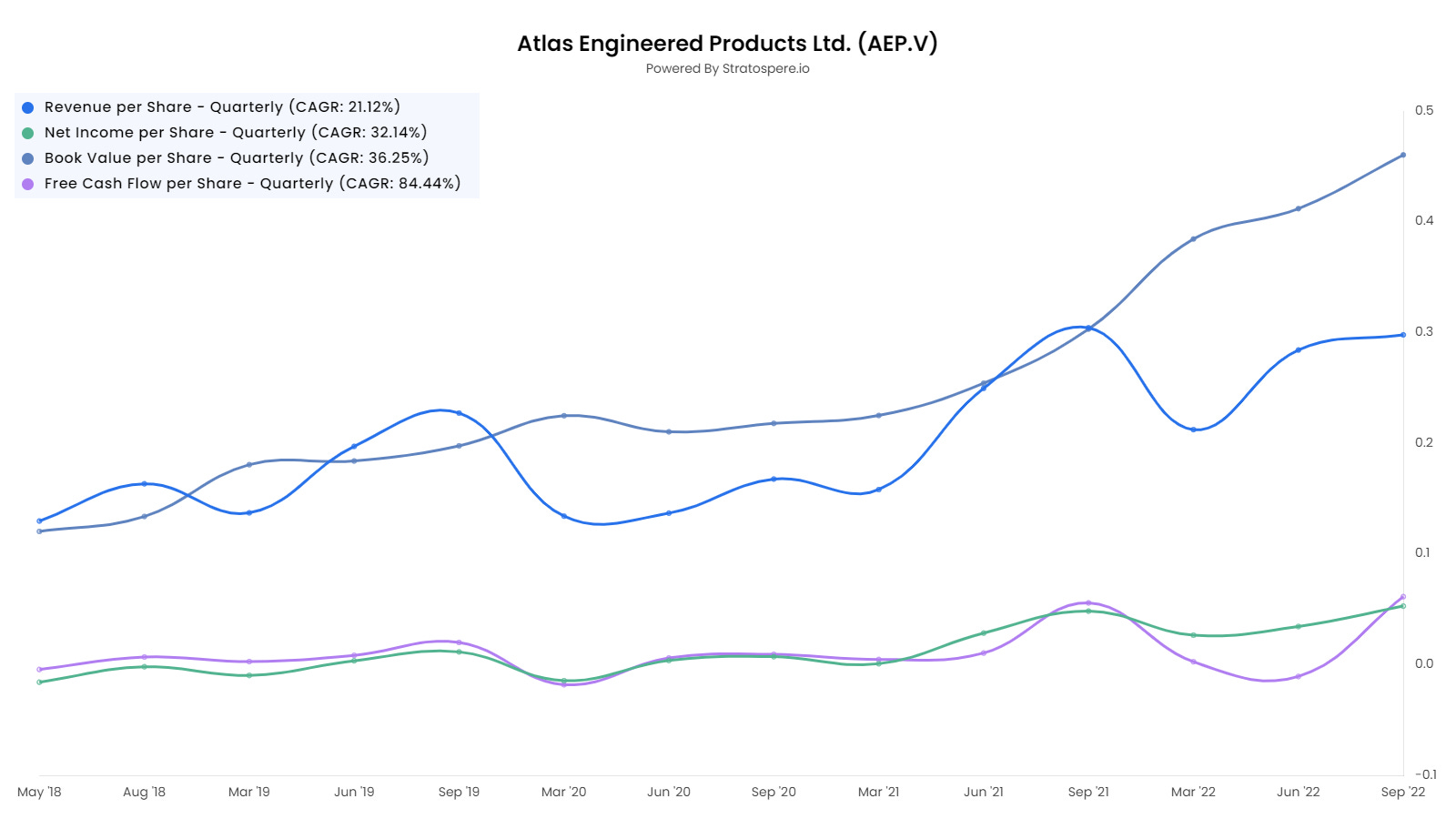

They have been able to in some instances improve revenues over a few years by 2x and gross margins from 20% all the way to 30%. This is likely something that they will get better at in terms of speed of improvements over time as they learn to do it better and more quickly with more and more acquisitions.

Insiders

Insiders own around 18% of the stock. Hadi Abassi is the founder with decades of experience. Starting with one shop and ultimately taking his baby public in 2017, he has real skin in the game with around a 10% stake. He seems to understand capital allocation better than the vast majority of not only microcap business leaders, but CEO’s in general. When speaking about future growth, he is clearly not interested in top line growth for growth’s sake. He is only interested in profit and often refers to taking things slow and focusing on improving profits in the most efficient way possible with the capital funds where they make sense.

Capital Allocation

Small acquisitions and capex for operational improvements in the newly acquired businesses is likely the long term reinvestment opportunity that is likely to stay available. With the depressed valuation recently, they have consistently been purchasers of their own stock with an NCIB renewed in November 2022 for 4.7 million shares good till the end of 2023 which represents 10% of the float.

When it comes to acquisitions, they are taking it slow, recognizing that there may be opportunities to continue to deploy cash at meaningful returns simply by improving operations at existing facilities. Hadi has mentioned buying in existing markets, for instance in between two locations as a way to reduce some shipping costs where those locations currently share some product production. He has also pointed to interest in the US market over the next few years. The US market is huge but there could be more challenges integrating and operating there compared to the well known Canadian market.

Historically, they have been good allocators. ROE and ROA in the 30-40% and 10-20% range.

Valuation Thoughts

The price of the stock has runup significantly since I started looking at it and since I initially purchased. It still trades around a 5-6X P/E. This isn’t the type of business that should fetch a huge multiple so I wouldn’t consider a huge upside from appreciation in valuation at this point, although multiples can go high with the current stock price momentum, so who knows.

Buybacks should continue to add value for the foreseeable future in my opinion, although not as beneficial as months ago. At some point, I would look to see them do more acquisitions as the better option for risk-adjusted returns.

Organic growth should run with the demand for new housing supply in Canada over the long term; likely low-mid single digits. Current earnings yield is ~15% and with buybacks at the right times and a patient acquisition strategy, it shouldn’t surprise anyone to be able to get 10-15% going forward (maybe more but I’m cautious with the exposure to the tough housing cycles that could hit them in the shorter term).

Finally, a nice chart to take it all in. The case for Atlas here is that there is a strong likelihood that the past few years of excellent execution and continued improvements is repeatable for quite a long time and they will also enjoy any continued secular tailwinds from housing supply/demand mismatch in Canada. Add on a management team that seems to understand capital allocation and you could have a real microcap gem here.

One more thing…

There’s an interesting free option in the future that could really help organic growth. Wall panels! Hadi eluded to this as being something they are being careful to not push too hard as it needs to be something builders are ready for. Wall panels are not currently used too much in North America but are adopted previously in places like Europe. The revenue for wall panels would basically be double that of the truss for the typical building (whoa…). I think there is no recognition of this possible outcome for Atlas at this stage and perhaps rightfully so. The other driver for this to occur in the industry is the lack of skilled and unskilled labor. Centralizing the fabrication of wall panels compared to the typical on site build would alleviate some of this pain so it could be a win-win for the whole industry. That being said, this is essentially a free option with potentially high upside and minimal downside.

If you enjoyed these charts, check out stratoshphere.io and use code SIMONH for a 25% discount on your first year.

That’s it for now, check back soon for more. As always, follow me on twitter and please share this with anyone who might interested in my work. My work is now completely free for all but there is an option for a low cost paid subscription as a way to support my work.

Thanks for sharing your insights!