AutoCanada $ACQ

A beaten down auto dealer rollup

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

Executive Summary

AutoCanda Inc. owns and operates car dealerships, service, and collision centers across Canada and Illinois. The business trades on the TSX under the symbol $ACQ. The business is headquartered in Edmonton, Alberta and was founded in 2006.

AutoCanada has a relatively stable underlying business that can be scaled for a long time with acquisitions of a fragmented market. There has been a lot of churn within the sector due to macroeconomic fears and a prolonged supply chain constraining OEM production of new vehicles since 2020. The stock price is beaten down, sales volumes should normalize over the next few years and the company is going to the buy back a lot of the shares outstanding.

This report will outline in detail:

the business model

the business quality

management quality

capital allocation

a view on valuation

risks of the business

investment thesis risks

By The Numbers

*Note: all figures in Canadian dollars, unless otherwise stated.

Market cap: 691 m $

Enterprise Value: 2.44 b $

Gross Margin (5 year avg): 16%

Operating Margin (5 year avg): 2.5%

EPS: 5.6$

P/E (5 year avg earnings): 20

P/E (LTM earnings): 5.2

What They Do

ACQ owns and operates franchised 62 new car dealerships in 8 provinces in Canada and 18 in 1 US state (Illinois). They have 25 brands in their Canadian operations and 16 in the US.

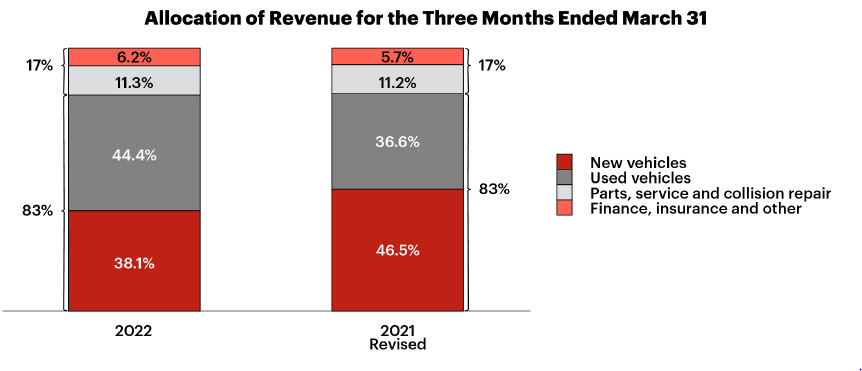

Revenue Mix

Revenue is dominated by new and used sales. They dwarf the revenue in financing and parts and collision. What is interesting is that new sales haven’t grown too much but used continue to go up. Due to the supply chain constraints from OEMs, new sales have been slowed, driving up current used prices. The longer this goes on, the longer used prices will stay elevated. The used market inventory is yesterday’s new car supply. Eventually, the balance will mean revert but it may take another few years to stabilize.

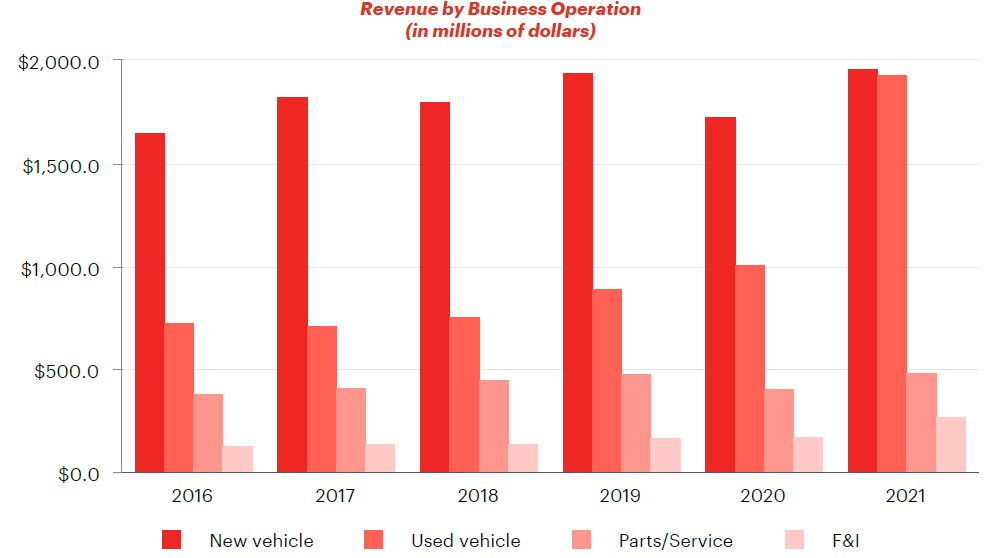

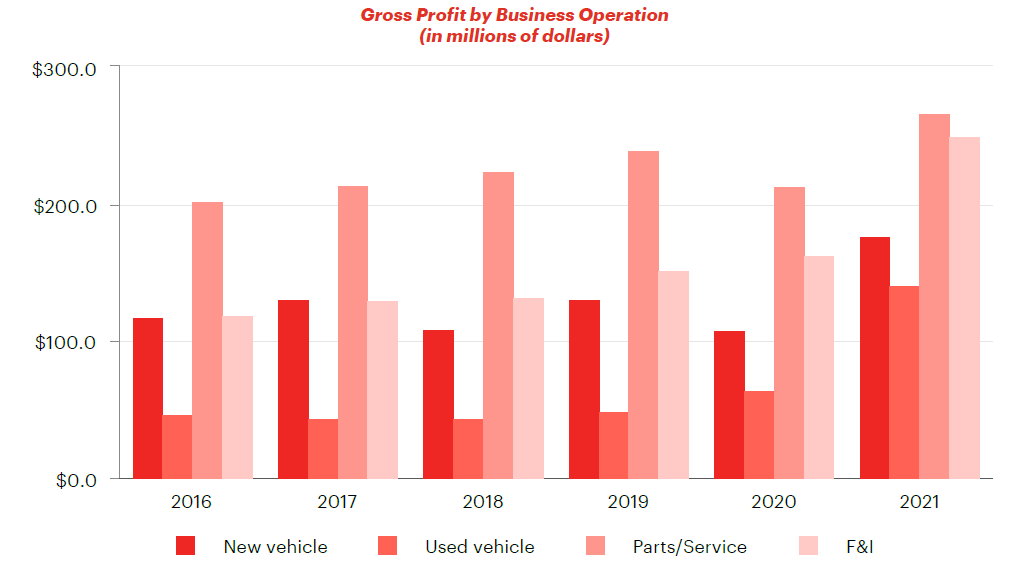

Now compare over a similar time frame, the gross profits derived from each segment. This is a clear picture of where the profits originate for the business.

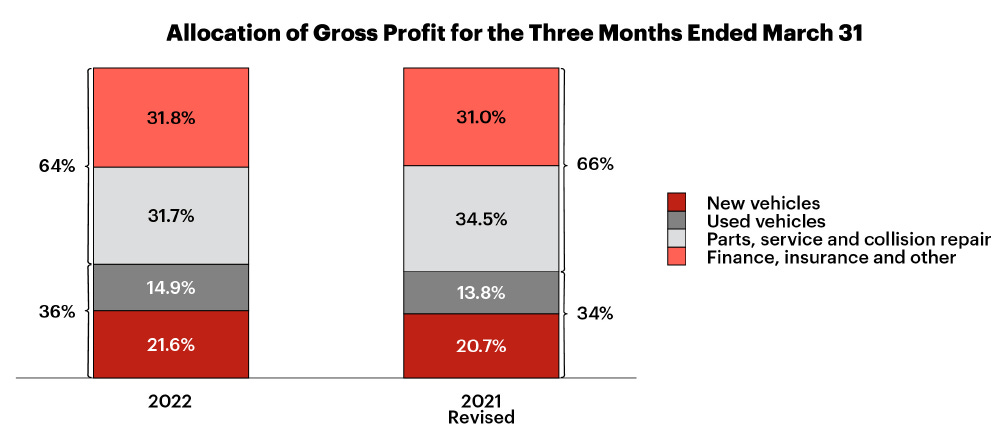

Gross margins are somewhat stable over time with new and used sales. They account for a lower portion of the gross profit as can be seen by the two charts below. Going forward, the company is going to focus a larger portion of its efforts on growing the parts and collision business and its internal finance operations, given the high margin and growth opportunities. If successful, gross margin (and subsequent operating and net margins) should increase. A driver for this success will be the focus on sales mix of used vehicle sales relative to new sales. As long as the supply chain issues with new vehicles remain, this should be relatively easy to maintain. It will be challenging in a good economy when supply chains are not constrained.

Used vehicle sales have been a significant focus of the Company as we strive for a 1:1 used-to-new retail ratio under the Project 50 initiative. The objective of Project 50 is to increase the average number of used vehicles sold at our dealerships to 50 per dealership per month. Used vehicle sales are typically less exposed to the cyclicality of the auto industry, as compared to new vehicle sales. Increasing our ratio of used-to-new vehicle sales is expected to diversify our revenue profile, as well as drive ancillary revenues in the higher margin PS&CR and F&I divisions.

- Excerpt from 2022 ACQ Annual Report

Recurring Revenues (Almost)

Parts, collision, and finance offers a better revenue stream partly because of its more recurring nature. Once you sign up for financing on a sale, the revenue comes in without any new sales required for the period of the contract. The parts and especially the collision businesses are much less discretionary compared with new or used vehicle sales and should offer some stability during economic downturns.

Purchasing a new, or even some used vehicles, is a very discretionary purchase in which customers do a ton of research and are very price sensitive as a result. This is why the margins aren’t great in this area. But what these sales do provide is better business after the initial sale.

Business Quality

Growth

Top line growth should continue as the company should have opportunities to acquire more dealers and collision centers. The industry overall likely won’t grow much beyond real GDP growth but they can continue to expand into a bigger piece of the pie by purchasing smaller and mid-sized players.

Bottom line growth should be assisted with some expansion to scale in their network and a focus towards the higher margin revenue streams. The top line margins have historically been very stable and just below some bigger businesses with similar models (a few percentage points opportunity).

Operating margins, and therefore income, was abnormally high due to supply constraints pushing up price for used cars. Expect this to come down when supply chains ease. Even with supply chains normalized, there is some opportunities for the industry to realize some structural changes to how customers use dealers which will lower operational costs on a more permanent basis. This includes more online interactions and preordering new and even used inventory.

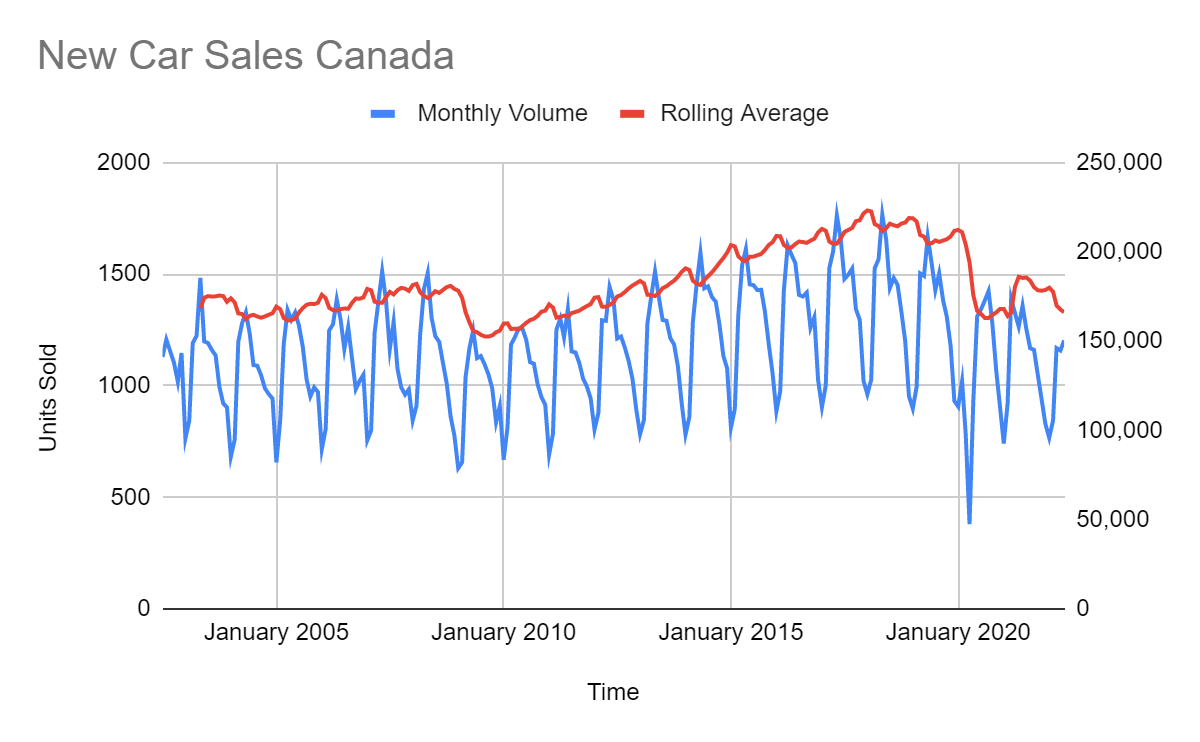

Exposure to Cycles

New and used car sales are inherently seasonal, peaking in May and June each year. More broadly, the seasonally adjusted volumes will be impacted by the broader health of the economy; specifically the consumer wallet. The following chart shows new car sales from Canada (data from Stats Canada). You can see declines in 2009 due to economic recession and again in 2020 due to supply shortages. There is some chance of a recession and associated decline but the longer term trend means that sales volumes should be up again in a few years as a glut of aging vehicles need to be replaced.

Moat

Car dealers actually enjoy a regional moat for their businesses. In one area there isn’t typically two dealers offering the same products. In some ways there are still lots of competition. Buyers will shop around and compare a Dodge to a Ford if they are thinking about buying a new truck, for instance. But the same is not true if someone is buying or servicing a Porsche or a Mercedes-Benz. To this end, part of the business enjoys a regional monopoly of sorts.

Management Quality

Capital Allocation

The dividend was cancelled as a response to the pandemic related shutdowns and associated business interruptions. It appears that this decision was based on risks to debt covenants and restrictions and as a cautionary strategic choice. There is no signal that the dividend will be reinstated in the near term. It appears that management is currently focused on share repurchases.

The share repurchases under a repurchase program has been ongoing and is now coupled with a modified Dutch auction between 22-25$ per share. The auction is set to close by 4th of August, 2022 and will spend up to $100,000,000 (14% of the market cap).

As of May 2022, there were 26,134,095 common shares issued and outstanding. The plan repurchased just shy of 900,000 shares (3%) in the first quarter of 2022. If share price stays relatively depressed, then it is a good thing for remaining shareholders who hold on for longer periods. The business will need to balance debt payments with share repurchases going forward as they have used debt to fund the repayments to date.

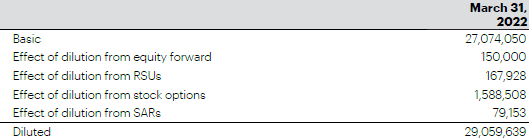

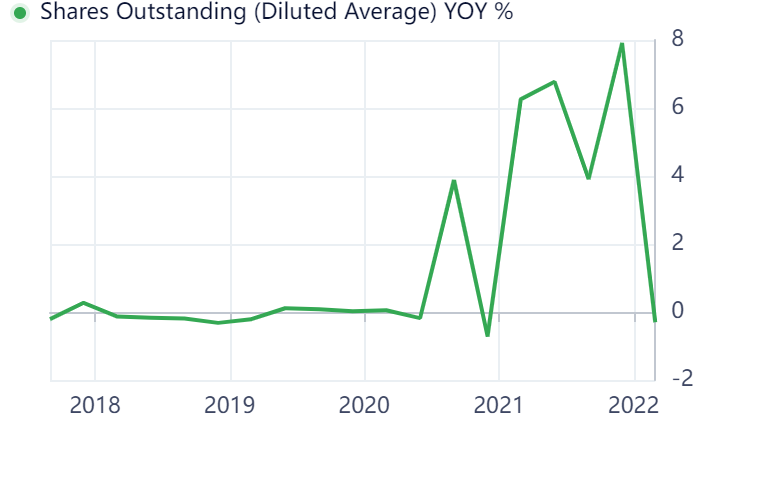

Share dilution will also occur similar to how it has occurred in the past due to stock awards and options grants. Diluted share count results in just under 10% impact to shareholders currently.

The chart below illustrates that recently share dilution was significant. What’s interesting is that this occurred at a local high in the stock price (50-60$).

Use of Debt

Debt to EBITDA is higher than some of the similar industry car dealerships (see table in valuation section). That being said, they appear to be handling it relatively well. What should help is a trend of credit ratings increases which will allow relatively good interest rates, even in an increasing rates world.

On April 14, 2021, Standard & Poor's Ratings Services ("S&P") issued a research update whereby it revised the Company’s outlook to stable, raised the issuer credit rating to 'B' from 'B-' and raised the rating of the Company's 2025 Notes to 'B' from 'CCC+'. On January 12, 2022, S&P issued a research update whereby it affirmed the Company's outlook as stable, revised the issuer credit rating to "B+" from "B" and assigned a 'B+' rating to the Company's Senior Unsecured Notes.

- ACQ 2022 Annual Report

The debt facilities include $1.3 billion in credit facilities, the bulk of which is wholesale floor financing, and is extended to 2025. There is also $350 million in senior unsecured notes due in 2029 at 5.75% per annum (lowered from 8.75% on a previous deal).

Personally, I would like to see the company de-risk the business by allocating some of the cash of share repurchases towards debt repayment.

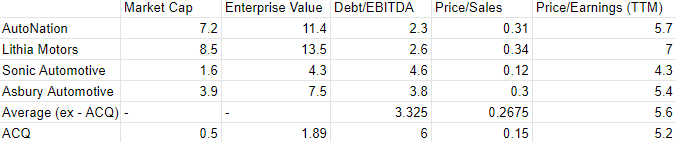

Valuation

The easiest way to get a sense of the valuation might be to compare to similar public companies with a proven track record. The table below is a quick look at comparing relative valuations.

The opportunity for ACQ will definitely be to reduce both the overall cost of its debt service and therefore be able to reinvest and grow per share. It is currently looking like it will do this with buybacks and some acquisitions and an operational focus towards financing products, used car sales and increase in service, parts and collision centers. The benefit that ACQ has is that it is still very small and has less competition in Canada compared to the US. The downside of course is that Canada is a smaller market overall.

Chances are high that the earnings yield at current prices is inflated (over-earning) but this can continue for a little while longer. If the business can continue to grow out of a downturn, investors will do well. The focus on the better revenue streams should help weather these storms and manage the debt load.

I think its conservative to think that a normalized earnings yield is closer to 5-10% and the that repurchases and debt repayment and acquisitions can slowly grow the bottom line, then it seems reasonable that you could get a 10% return at today’s prices, even in some not amazing economic scenarios. The upside would be much higher if margins can stay elevated for longer in combination with share repurchases.

Personally, I’d want to see debt be reduced going forward and then focus on allocating capital towards repurchases and collision centers to improve the resilience of the business. For now, the business quality isn’t high enough for me to take any sizeable position but this doesn’t mean it won’t work out well.

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

That’s it for now, check back soon for more. As always, follow me on twitter and please share this with anyone who might interested in my work. My work is now completely free for all but there is an option for a low cost paid subscription as a way to support my work.