Big Brother Is Watching You

The Compounding Engine of Zedcor's Fleet

Disclaimer: I own stock in Zedcor at the time of writing. This content is not intended as advice of any kind

The telescreen received and transmitted simultaneously. Any sound that Winston made, above the level of a very low whisper, would be picked up by it; moreover, so long as he remained within the field of vision which the metal plaque commanded, he could be seen as well as heard. There was of course no way of knowing whether you were being watched at any given moment.

-Quote from the book, 1984

I previously wrote about Zedcor and (now) painfully erred in deciding to pass on it. I have since corrected that mistake and it is a reasonable size holding in my portfolio today. I decided I should take a fresh look at it, as if I didn’t look at it before. For those keeping track at home, Zedcor is about a 10X from when I wrote about it. If you have found value in my writing, I would urge you to consider becoming a paid sub as I continue to work to find and uncover high quality investment ideas.

Zedcor $ZDC.V

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data.

The Setup

Here’s a question: what would you pay to avoid hiring security guards?

Not because there’s anything wrong with security guards as people—but because as a business model, it’s a mess. High turnover. Rising wages. No-shows. And the kicker: they’re expensive as hell. We’re talking $18,000 to $36,000 per month for 24/7 coverage at a single site.

Now imagine you could get better security outcomes—verified security, not just a warm body in a chair—for $1,200 to $3,400 per month. That’s a 25% to 60% cost saving, and you’re getting AI-powered cameras, live monitoring, and the ability to stop crimes before they happen.

This is the business Zedcor has built. And if they execute on what they’re setting up for 2026 and beyond, we could be looking at one of those rare opportunities where you catch a company right at the inflection point.

What Zedcor Actually Does

Zedcor makes and deploys the MobileyeZ platform—essentially a self-contained surveillance tower that combines solar power, batteries, high-res cameras, AI processing, and 4G/5G connectivity. These aren’t your typical “dumb” security cameras. They’re monitored 24/7 by trained operators in Calgary and Houston who can see what’s happening in real-time and respond immediately.

When someone tries to break into a construction site or steal copper wire from a storage yard, the AI flags the motion, a human operator verifies it’s a real threat (not a raccoon), and they can do a “talk down” via loudspeakers. According to Zedcor’s data, 95% of crimes are stopped right there. If the intruder persists, police get called with a detailed description—not just “motion detected,” but “white male, red hoodie, black pickup truck, license plate visible.”

The elegance here is simple: you’re replacing expensive variable costs (labor) with a fixed capital asset (the tower) and a highly scalable monitoring operation.

The Strategic Backstory: From Energy Services to Security Tech

Rewind to 2021. Zedcor was primarily an energy services rental company—the kind of business that looks boring on paper and bleeds cash when oil prices drop. Management made a gutsy call: sell off the energy rental division for $11.3 million and go all-in on Security & Surveillance (S&S).

This wasn’t just an asset sale. It was a purification of the business model. They paid down debt, got their debt-to-EBITDA under 2.0x, and refocused the entire organization on building out the MobileyeZ platform across North America.

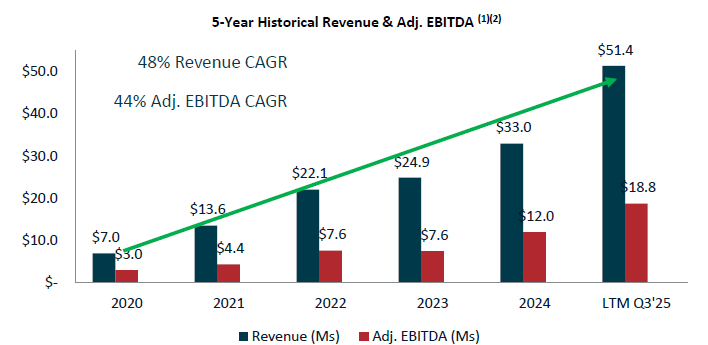

2022 was the proof-of-concept year. Revenue from continuing operations jumped 63% to $22.1 million. Adjusted EBITDA hit $7.6 million—an 87% increase over 2021. Utilization rates on their MobileyeZ towers stayed above 90%, which is a great signal for any rental-style business. By the end of 2022, they had 506 units deployed and were expanding into Ontario and Manitoba.

The foundation was set. Now came the hard part: scaling.

2023: The Pipeline Cliff (And How They Navigated It)

For years, Zedcor had been heavily concentrated in a couple massive pipeline security projects, including Trans Mountain. When those projects wound down in late 2023, the company faced a classic “lumpy revenue” problem—hundreds of towers suddenly coming off contract, needing to be redeployed.

Management’s response? Go hyper-aggressive on customer diversification. They expanded the sales force, ramped up marketing, and signed over 190 new customers across industries like commercial construction, retail, and automotive logistics.

Despite the headwind, they still grew revenue to $24.9 million and held Adjusted EBITDA flat at $7.6 million. Margins compressed a bit (down to 30.5%) because they were investing in the infrastructure to manage a higher volume of smaller accounts, but the strategic work was critical. They were de-risking the business by spreading revenue across dozens of customers instead of two mega-projects.

Oh, and they opened a national HQ and assembly facility in Houston, Texas in November 2023. This wasn’t just a service center—it was the beginning of their manufacturing moat.

2024: The US Expansion Starts Paying Off

2024 was the year Zedcor’s “hub-and-spoke” model started proving itself in the US. They signed their first major national homebuilder (likely D.R. Horton, based on case studies) and several general contractors in Texas. By Q1, utilization was back up to 90% as the pipeline towers got redeployed into higher-margin urban and commercial sites.

Financially, it was a breakout year:

Revenue: $33.0 million (+32%)

Adjusted EBITDA: $12.0 million (+58%)

EBITDA margin: 36.4% (up from 30.5%)

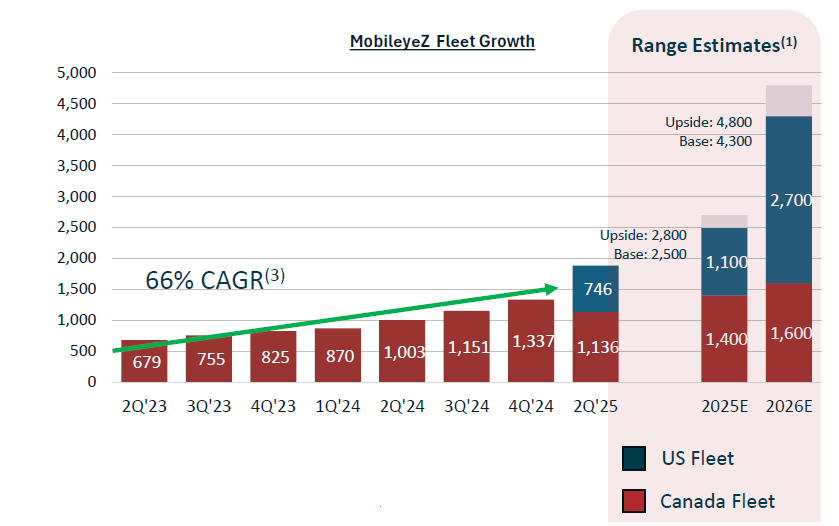

Fleet size: 1,333 units (up 62%)

The US contributed about 15% of revenue by year-end, and the trajectory was steep.

The big operational win was getting the Houston manufacturing plant dialed in. By bringing more component assembly in-house, they cut production costs by 15% to 20%. They also launched the 2024 Solar MobileyeZ model—a fully standalone unit with battery backup and AI at the edge. Faster deployment, lower maintenance costs. The flywheel was starting to spin.

2025: Hyper-Scaling and the Capital Fortress

2025 is when Zedcor went from “interesting small-cap” to “holy shit, they might actually pull this off.”

Two big capital moves:

February 2025: Closed a bought deal for $25.3 million at $3.35/share

October 2025: Secured a new $75 million revolving credit facility with National Bank (replacing the old $30M facility)

That’s $100+ million of liquidity to fund growth without significant dilution going forward. Smart.

Results for the first nine months of 2025:

Revenue: $41.0 million (+81% YoY)

Adjusted EBITDA: $14.8 million (36% margin, holding steady)

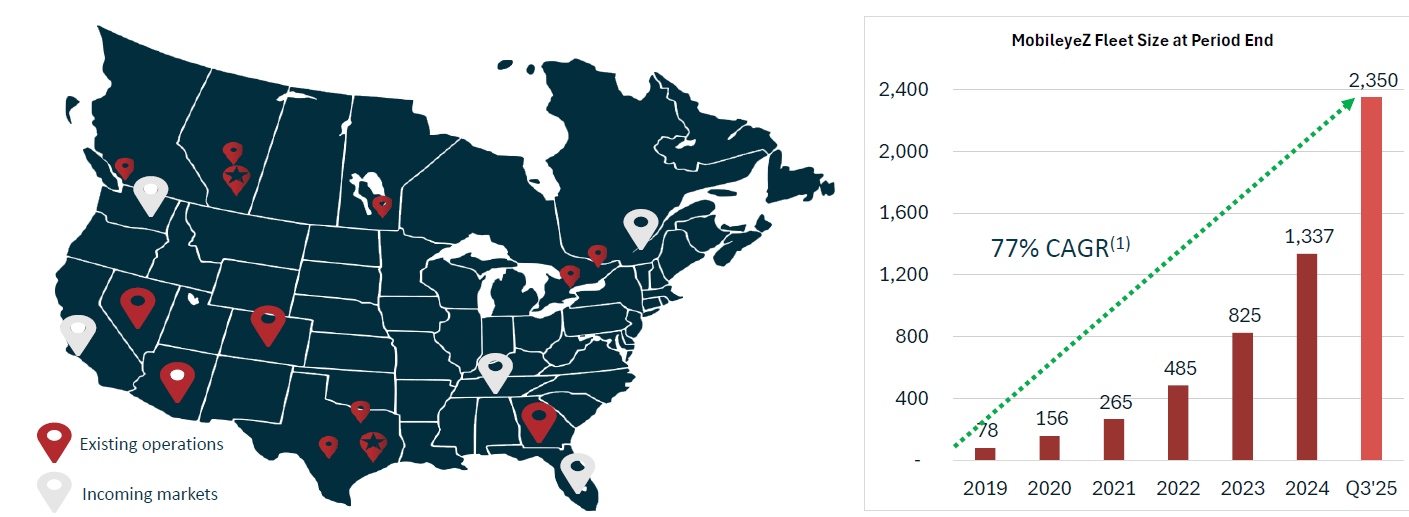

Fleet size: 2,351 units by end of Q3 (+88% YoY)

US revenue contribution: 36% (up from ~15% in 2024)

They produced 1,016 towers in the first nine months alone. That’s more than double their entire 2022 fleet, built in less than a year. And they’ve opened new service centers in Denver, Phoenix, and Las Vegas, all showing “rapid growth” in their first year.

The 50-Tower-per-Week Manufacturing Moat

Here’s where things get really interesting.

As of February 2026, Zedcor’s new Houston manufacturing facility is fully operational. It’s 50% bigger than the old site, and they’ve ramped production to over 50 towers per week.

Do the math: 50 towers/week × 52 weeks = 2,600 towers per year.

For context, it took them several years to build their first 1,000 units. Now they can build twice that in a single year.

This is a massive competitive advantage:

Enterprise orders: A national account asking for 500 units? Done in 10 weeks, without disrupting other deliveries.

Geographic speed: They can supply new service centers in California, Florida, and Georgia simultaneously, ensuring sales teams have inventory on day one.

Unit economics: Centralizing manufacturing for all of North America in one facility drives volume discounts on cameras, sensors, steel, etc.

Plus, they’ve de-risked the supply chain. They pre-ordered the bulk of their cameras and 35% of their steel for 2025/2026 before tariffs hit. And since raw steel is less than 10% of total tower cost, they’re insulated from commodity volatility.

The Labor Arbitrage Play (And Why It Works)

Let’s talk about why this business model is so compelling.

The traditional physical security market is trapped in a low-margin, high-churn model that relies on human guards. Wages are rising—$15 to $40/hour depending on the market—and labor shortages are chronic. To provide 24/7 coverage at a single site, you need 168 hours of labor per week, costing $18,000 to $36,000 per month.

A MobileyeZ tower, including 24/7 live verified monitoring, costs $1,200 to $3,400/month. That’s $1.64 to $4.66 per hour.

This isn’t a marginal improvement—it’s a structural cost advantage that gets more compelling as labor costs rise and budgets tighten.

And the security outcomes are better.

Traditional “blind” alarm systems have a 95% false alarm rate. When every motion sensor triggers a generic alert, police stop responding quickly, and the whole system becomes useless (”alarm fatigue”).

Zedcor’s approach uses AI to filter out irrelevant motion (animals, shadows, passing cars) and only alerts human operators to real threats. Once verified, operators do an immediate “talk down” via speakers, which resolves 95% of incidents before they escalate. If the intruder persists, police get a detailed description—much higher priority than a blind alarm.

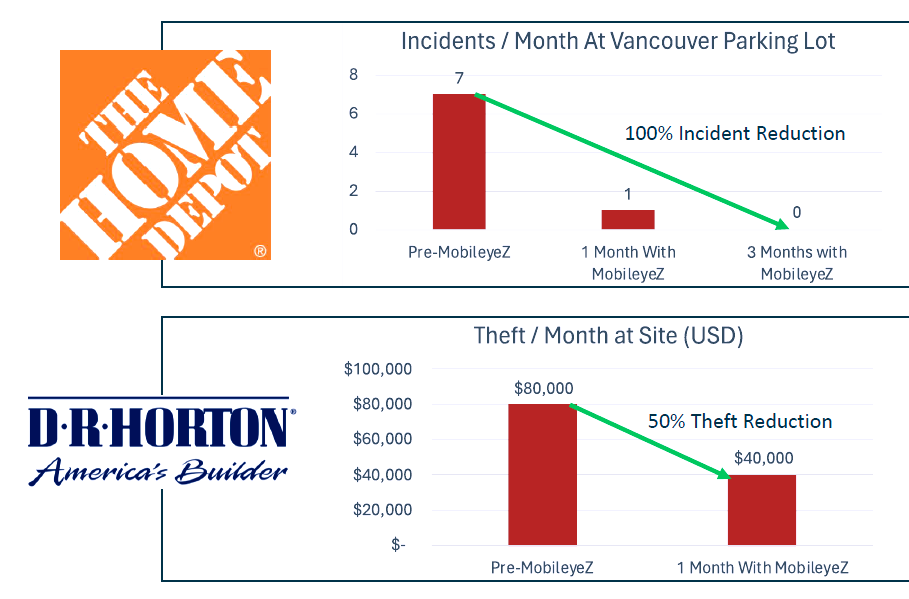

The case study with D.R. Horton showed a 50% reduction in theft and $1 million in savings for a single division over 10 months. That’s the kind of ROI that gets CFOs excited.