Copart Moat Review

I've never met a wreck I didn't like

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

Disclosure: I own shares of Copart CPRT 0.00%↑ in my personal accounts and therefore am likely to be biased in some ways when discussing this business. This is not meant as investment advice.

"The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage."

Warren E. Buffett

Copart is a duopoly in its industry and enjoys durable competitive advantages that are relatively well understood by shareholders and other analysts and investors alike. The real question at this point is the durability of this advantage - the “Moat” and if it is getting wider or narrower with time.

Founded in 1982 Copart has grown from one yard in the US into a global force in the industry with over 200 yards in 11 countries. It boasts more than 175,000 vehicle sales a day at its auctions. Unlike its only real competitor IAA, Copart strategically owns its own land which offers long term control over this capital intensive part of its business. Its operations are self-described as follows:

Copart, Inc. provides vehicle suppliers, primarily insurance companies, with a variety of services to process and sell salvage vehicles through auctions. The Company offers salvaged vehicles that are primarily sold to licensed dismantlers, rebuilders, and used vehicle dealers. Copart serves customers worldwide.

Moat Analysis

In order to judge a competitive advantage, we must understand the real meaningful few drivers behind these advantages and mix qualitative underlying aspects with quantitative KPI’s and financial outcomes. There are a few indications about why Copart may have sustainable competitive advantages in its business and there could be data to suggest if these are getting stronger or weaker:

Network effects: Copart clearly benefits from its position in the middle of buyers and sellers. And as the number of buyers and sellers increases, the value of the platform increases for both. This has thus far enabled a strong network effect, making it a steep hill to climb for new entrants. In my view, this is the most meaningful competitive advantage and it is tough to see any small player disrupting it. IAA is being sold to Richie Bros. Auctions and may no longer have the same singular focus that it has had as a stand-alone entity so the threat from IAA appears to be weakening, for the time being at least

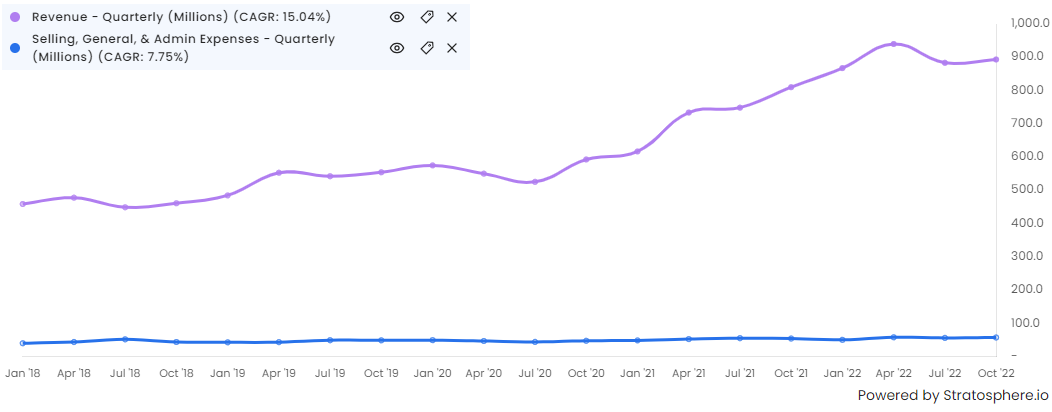

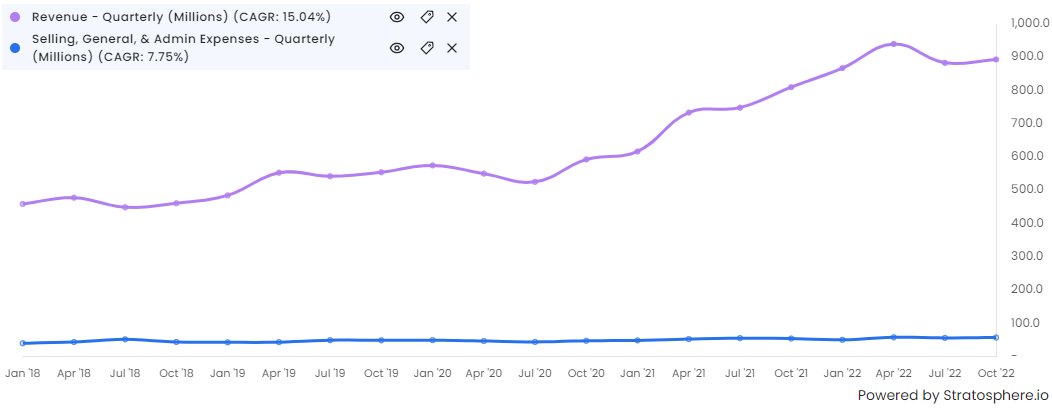

Copart Revenue Growth .

Customer relationships: Copart has built strong relationships with a wide range of customers, including insurance companies, fleet operators, and salvage vehicle buyers. These relationships can be a source of competitive advantage, as they may make it more difficult for competitors to win business from these customers. This one is one of the most important and meaningful advantages. These relationships will depend on maintaining the dominant scale and continuing to offer superior value in its network compared with smaller competitors

Copart SG&A Expense relatively flat Scale: Copart has a large and growing global scale, with 200 locations, up from 175 in 2016. It has continued to expand into new countries. This scale allows the company to spread its fixed costs which can be seen in its operating margins expanding steadily over time. This advantage likely has marginally diminishing returns within the near future as there are fewer high quality markets to enter. There are plenty of markets but not all will work out as well as previous strongholds, in my opinion

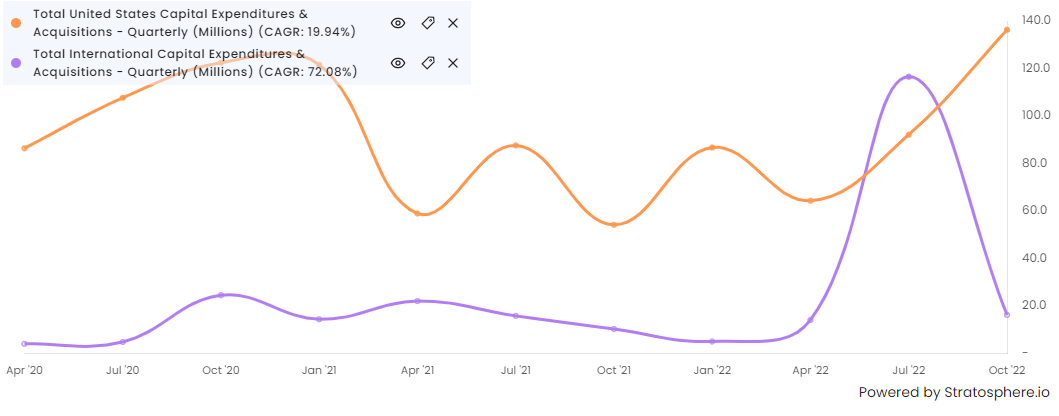

Copart US and Intl. Capex - lumpy but strong .

Technological advantage: Copart has invested heavily in technology, which it can because of its scale and long term orientation. It has previously been a leader in its use of its online auction platform and has begun implementing advanced data analytics and machine learning techniques to become more efficient, reduce friction with customers and improve operating costs. This one is the least durable competitive advantage in my opinion as it can be replicated over time with capital investments by competitors.

If you enjoyed these charts, check out stratoshphere.io and use code SIMONH for a 25% discount on your first year.

That’s it for now, check back soon for more. As always, follow me on twitter and please share this with anyone who might interested in my work. My work is now completely free for all but there is an option for a low cost paid subscription as a way to support my work.

One insight I'd offer concerning IAA vs Copart.

IAA operates in a much worse location than Copart does in Minnesota. The Rice Street location for IAA is in a high poverty & crime area of St Paul. Copart operates in East Bethel where yard intrusion is much less likely.

I drive by both locations frequently. Rice St for work. EB when visiting family. Rice St is definitely a less secure environment. You can see inside the entire yard from on the bridge near it. You can not see inside of Copart from outside. The fence is tall, and wall-covered, rather than IAA's simple chain link fences.

I'd venture to guess IAA operates where it does out of necessity rather than choice, and the opposite is true of Copart.