Dentalcorp $DNTL.V

Open wide…for a dental rollup!

Upfront disclosure: I currently own a small number of shares in this business. None of this is financial advice but rather a way for me to write out what I think at the time.

Have you ever wondered what it would be like to own a business that could potentially continue to grow for the next few decades, consistently get repeat business and not be put at risk by economic recessions? An interesting small-ish company that is relatively unknown could be of interest to you! Read on for more on Dentalcorp.

What do they do?

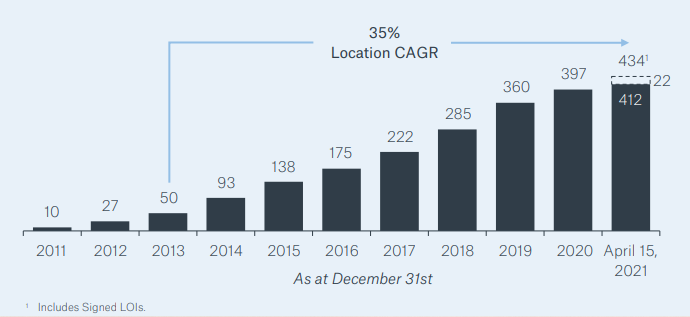

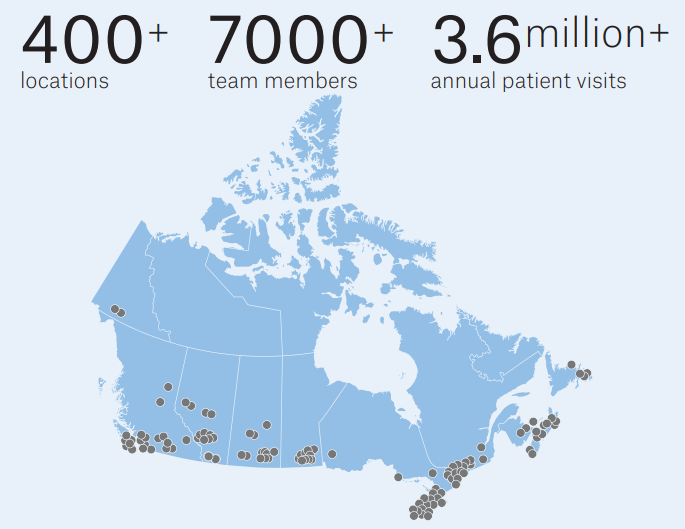

Dentalcorp has been buying and operating dental practices in Canada since 2011. They have just recently become public in 2021 at around a 2.5 billion Canadian dollar valuation. They started with just a few practices and have steadily grown to over 400 locations in Canada. They have focused on dentistry and related services and will continue to do this for the foreseeable future.

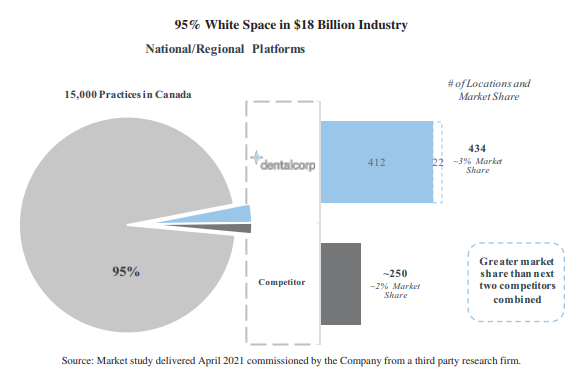

The company has grown to have about 3% of the total Canadian market and don’t really have any sizable competition. They claim that approximately 95% of the market in Canada is still privately owned individual practices, mostly owned by one or several of the dentists running the shops.

They have recently raised funds to support operations as well as future growth prospects. The IPO on the TSX venture exchange raised just shy of a billion dollars to restructure some of the company’s debt and fuel future acquisitions.

Do they make money?

Gross margins seem to be very good at close to 50%. I imagine these will be consistent and non cyclical given the steady nature of the business and benefits of scale to the business.

There isn’t significant free cash flow showing in part because of the growth and increases in operating costs but as the company comes out of the COVID years, the gross income (over 300 million$) should start showing up more and more as operating income and free cash flow. The recent cash raise from the private placement and IPO should help bridge the gap to a point where more and more earnings are reported and growth continues.

Are there reinvestment opportunities?

Yes, definitely.

Basically, the entire thesis here is inorganic growth via continuation of the acquisition strategy. From the investor presentation the company presents a 35% CAGR for locations. I think more realistically, this number has to come down (and it does if you ignore the tiny 2013 base number of 50). That being said, double digit CAGR for the next decade is not outside the realm of the imagination. They quote 15,000+ locations in Canada as potential targets. This means, even if they grow locations 5 times from the current 400ish, they will still only penetrate 15% of the current market. The fact is that Canada will continue to grow in size over the next few decades and the use of dental services will continue to be strong, leading to more and more locations overall. They quote over 2% growth in the market (not terribly high) but consistent.

You should expect modest organic growth with better cost management, some minor network effects, growth of GDP, etc. but I don’t think this is overall going to be impactful for returns (I suspect the organic growth to keep up with inflation for sure).

There are other options for growth should the number of practices willing to sell at reasonable prices reduce significantly. They could venture to other geographic areas… obviously the US is a huge market. The US would be more challenging as the medical industry is not the same model as Canada. In Canada, there is less risk of payment problems due to the nature of the system. Typically, in Canada, patients pay and get reimbursed by their insurance coverage (sometimes submitted by the dental practice). This is not the case in the US. In most cases there is a copayment system that is more complicated and has more risk of delayed or disagreements regarding payments.

The other areas where growth could come from in the future is other similar health related industries within Canada. The company hints at a desire to explore future options in the veterinarian, optometry or dermatology clinic industries which share some of the features of the dentistry industry (repeat business, patient direct payment model, etc.) The opportunities here include a desire from the owners to sell for similar reasons as the dentists - reduction in administrative burden, risk reduction from regularity issues, succession and retirement strategies, and the enjoyment of lots of money now!

Is there a risk of a blow up?

The underlying businesses are certainly not a fad. People will continue to have teeth into the future for… well, for as long as homo-sapien evolution allows. There is no automated software tech that will be disrupting the need for a dentist or dental hygienist or other specialty care anytime soon.

There is some risk that competition could come in and disrupt the network that dentalcorp currently enjoys and is growing. That wouldn’t be quick or easy however.

One thing to watch is the debt. The company does have debt. Given the somewhat predictable nature of the underlying businesses, some smart use of debt is welcomed. The recent IPO and private placements have raised significant cash to restructure previous debt and to fuel future growth. I would comfortable with more debt in this business than most as long as the company can continue to do acquisitions at reasonable incremental values. They quote ROICs of 15% which if sustainable can lead to tremendous shareholder value over long periods of time.

Is management sketchy?

Perhaps too early to tell.

They have been successful at growing the underlying business for the past decade. It isn’t really enough historical financials available to quantitatively judge this very much. The founder and CEO owns somewhere around 5.9% of the business and has a multi-voting class of shares which effectively allows control of 37% of the votes which means significant control of the company should persist. Other early investors own a significant stake in the company which could lead to an opportunity for new shareholders if they decide to exit after the lockup expires.

There is no current dividend strategy as the focus will be on growth, likely for an extended period of time. In some future state, this could change. It is not yet clear if further dilution will occur with stock offerings beyond the most recent sale at around 14 dollars. One further related item to note is that there is a lockup that is set to expire 180 days after the IPO (November 23rd, 2021). This has some potential to drop the market price as some insiders and early private investors can sell some of their stock all of a sudden. Keep an eye on this as an opportunity if it presents itself.

Does it have a moat?

Maybe.

Scale is likely the most significant moat the business will enjoy. Since most of the competition is small individual locations or regional in nature, there isn’t really a big competitor that can offer the same network of dental services everywhere in the country. The barrier to entry for competition is not high to start but would not be quick to be able to get to this type of scale.

I don’t think there is a real “brand” moat here nor is there any regulatory capture beyond what every other individual dentist has. In each province, there is a different set of regulations that govern the industry.

Is it cheap?

If the growth of the underlying businesses can continue to compound at 15-20% for the next 10-20 years, then this is not a terrible price to pay (in fact, it would be a GREAT price).

Because there is much “white space” to consolidate in the industry, it’s not much of a stretch to think that over the next decade, the number of locations grow significantly and the earnings grow with it. Can the locations be 5 times higher in number in say 10 years? Sure. If so, paying 3 or 4 times sales now will certainly be a reasonable price. If it can grow 10 times as large in 15 or 20 years and potentially enter different geographic or tangential industry segments, then this is a steal of a deal.

If you are only comfortable with traditional valuation metrics, then this is not a cheap stock and perhaps you should move on and keep this on your watchlist for now.

In any case, there is certainly a risk of valuation compression (multiple compression) in the near to mid term if a rollup growth strategy were to go out of fashion in the market.

Final thoughts:

For many, this will be too early to tell if there is real long term value here given the recent IPO, and that is probably the safe bet. That being said, it is hard to imagine a case where this business model does not enjoy at least some long term success. There are many examples of long term compounders out there that have done exactly this type of thing. Roper technologies, Constellation Software, HEICO, Transdigm, GFL, to name a few have successfully employed similar models in other industries that could be aggregated and grown inorganically over long periods of time. This one is currently relatively small and should continue to grow for a long time to come.

Whether it can return value to shareholders will be something yet to be determined due to its relatively short time on the public stage but it does have some promising signs. It is somewhat difficult to value but that will become easier over time with more data.

That’s enough for me, I have to go to a dentist appointment…man, I hate the dentist.

Follow me on twitter @MoS_Investing and be sure to share and subscribe for free!