Nintendo $NTDOY

A princess in the castle?

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

Nintendo is a long lasting and conservatively run organization. Operating with great assets in its iconic IP, in a growth industry with an edge in pricing power and distribution. It’s exploring related markets and is aiming to extend the success of its console to reduce the cyclical nature of its core business. The downside remains tied to a chance of a repeated failure to avoid the downturn past the current console cycle peak as well as the ever-increasing competition as video games grow and evolve.

What is Nintendo?

Nintendo was founded in 1889 as a playing card company in Japan. Over time, they morphed into a toy and game company.

The modern version that is well known around the world was put into motion in the 70’s and 80’s. After the success of the home consoles in the 80’s and 90’s and especially after the birth of a Mario, the Italian plumber, the company was a household name in both the West and developed international markets.

Most well known for their video game consoles and the associated iconic IP, the business is also venturing further into the toy market as well as other media and theme park ventures to become more broadly diversified but also to extend the reach of its fanbase. The company trades publicly in Japan but is also available as an ADR on the OTC Pink marketplace as NTDOY.

Some key numbers:

Market cap: $ 53 billion USD

Enterprise Value: $ 40 billion USD

P/E: 13

P/S: 3.5

Gross Margins: 55%

The Bull Case

Transition to digital sales

As the video game industry continues its transition to fully digital sales of its software (and likely at some point, getting rid for the need for hardware consoles at home someday too!), the gross margins for Nintendo should continue to increase. The last several years of gross margin expansion bear this out.

It’s also noteworthy that there has been a lag in this shift with Nintendo compared to its peers. I suspect this is due to a strong relationship with the customers with its IP and the value they perceive with owning a physical copy. I believe this is the same underlying strength in the brand that is also demonstrated in historically maintaining high prices (no flash sales) on Nintendo’s first party games.

Secular growth in video games

There is no doubt that over the past 30 years, video games have continued to grow in sales. The industry has evolved to fill many niches and to extend how people interact not only with the game but the entire culture. There is also little doubt that the industry will continue to grow; what is unclear is the directions which it will go and who will be the winners and who may be left behind.

It’s clear the growth in the console market has been less strong than other areas. While it seems likely that Nintendo would move more into the mobile space, it’s not clear that they will make meaningful entries anytime soon and so it seems reasonable to discount that for now.

")

Iconic intellectual property

If you check any list of the most popular games sold on Nintendo consoles, far and away the top of these lists are dominated by Nintendo first party games. Over and over again Mario, Zelda, Animal Crossing, Smash Bros., Metroid and other names appear. They have been doing this successfully over decades and continue to evolve. They have also been somewhat successful with new entries such as Splatoon! where the second installment has sold over 12 million copies.

Distribution

You want to buy a Mario or Zelda game? You must go through Nintendo’s ecosystem (one way or another). Unlike some other big game franchises, there is no alternative. You must have a Nintendo to play. This can be a double edged sword if the console is not a hit. Certainly there would be more games sold if they were available on all consoles and PC. That being said, I suspect this leads to a higher quality product (optimizing for one ecosystem and device) and also allows Nintendo to control price and have control over their own digital marketplace. With the shift to digital, the used game market is slowly becoming a thing of the past and I believe this benefits Nintendo in the long term.

The key to long term advantage here would be the focus on high quality hardware and marketplace for games to keep players in their ecosystem. As long as that is a positive experience, the first party games will continue to be huge and be very profitable for Nintendo going forward. If they were to lose their base of fans that own a Nintendo console, at some point they should evaluate moving to only producing games and shipping to all markets to increase the volume and make up the high margins they would enjoy in their own ecosystem.

Less cyclical

With the recent launch of the Switch Lite product and now an improved OLED screen for the Switch, it seems as though Nintendo is doubling down and making every effort to extend the life of the current successful hybrid console. In the past, the company would have the handheld and the home console. They have proven that the technology and consumer desire is there to sell a premium hybrid console and this should continue in the future.

There are suspicions of a forthcoming enhanced and beefed up version of the Switch that will actually be a new console with hopes for backward compatibility. While the timing is unknown, I believe whether it comes out next year or the year after is not terribly relevant in the long term. It should bridge the gap very well and if it merely improves the hardware to pump out better display/higher power and doesn’t attempt any crazy new control design then it will only lengthen the period for the “Switch” success.

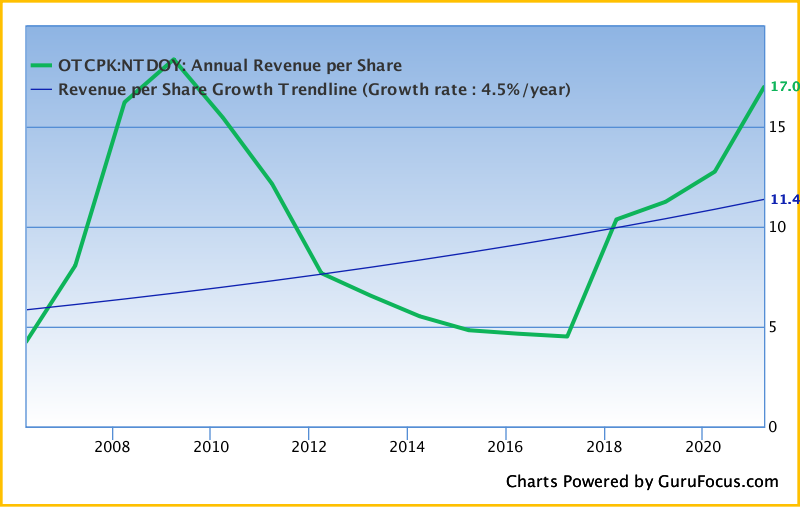

What is not often mentioned when people cite the cyclical nature of the past console boom or bust nature of releases has been the fact that this was previously true for the entire industry. Over the last generation of consoles, this cyclical nature of sales has reduced significantly. I don’t see why this wouldn’t be at least somewhat true for Nintendo going forward as well. Furthermore, if you look at the longer history, the dramatic cycle has not always occurred and has been more muted in the companies own past (compare N64/Gamecube transition and even better the handheld transitions on the visual chart below).

Other ventures

Recently, Nintendo has launched new theme parks with Universal Studios and have already announced expansion plans. I believe this will strengthen the brand and iconic IP further. Only time will tell how this contributes to the bottom line.

The company also announced a movie next year with an all-star cast of voice actors. I’m happy they are broadening their reach into media and if executed well, could be beneficial for the brand. I would not expect large impacts to the bottom line at this point. If successful, it could lead to other opportunities (a Nintendo cinematic or tv universe?) but that is likely a longshot at this point.

Other recent successes in building on the Nintendo brand has been the successful partnership with LEGO.

Capital allocation

Investors have traditionally gotten a reasonable dividend and that has grown significantly in the recent past. The business has also recently announced and completed a buyback program which is a good sign that they are considering the shareholder return options available. The best option would be to find good returns in the business to reinvest the capital and I believe they are doing that with their recent ventures into the toy and media partnerships and the theme parks. I would not be surprised if the dividend is cut in the future if the cyclical nature of the video game sales rears its head.

The Bear Case

Cycles persist

The boom-bust cycles seen in the past with hit or miss consoles could come back and stimmy future growth opportunities for the business. While I believe this is likely to be true in the future, I believe the extent to which it is true is likely to be overstated. Nintendo is making efforts to extend console lifespans and have also hinted at iterative progressions for new releases, to align with the trends of the broader industry.

I believe the key to flattening the cycles will be to bridge these gaps by releasing old games on new consoles (which they have had recent success), offering backwards compatibility and online catalogues of past games (which they seem to be moving towards) as well as offering fans other forms of Nintendo joy in the form of movies, toys and the theme park experiences. I wonder if the inevitable end state is for Nintendo to transition away from consoles altogether. I believe this is likely going to happen at one point or another and I think it could work out just fine as it would allow the organization to focus on more and better games. The downside of course would the potential loss of the marketplace that would erode some margins but the upside is also cutting the costs for new console development as well as broader reach for their content.

Lagging tech

In the last couple of decades, the tech for Nintendo has not been the most powerful or cutting edge. In some ways that has hurt the business. In other ways, there is an argument to be made that this has resulted in continued high quality games due to the constraints of the hardware (for first party games). I tend to think this has been a hindrance as it makes it more difficult for higher end games to be desirable on the Nintendo consoles. On the other hand, smaller games have grown in popularity over the last decade and power has been less of an advantage for the consoles of the industry.

Going forward, if Nintendo continues to produce consoles, they need to be at least comparable to their competition to stand a chance at reaching higher sales for their consoles and having a big marketplace for their games (how they make money). Strategically, it may not always make sense to take on Sony and Microsoft in the power struggle. They have been able to carve out niches with their Wii and Switch (and previous handheld offerings) that have been very profitable. Even if they could continue to do this, I’m not convinced its the correct strategy given the direction of the industry.

Goliath competition

The downside to the growth in video games as an industry has been the incredible capital pouring into the arenas for new and exciting competition. While Nintendo enjoys their iconic IP, there is no guarantee that new competition will not come in and steal the show. Giant tech has been entering the space with the hopes of controlling a big piece of the pie in the future. Amazon, Facebook, Microsoft and Tencent to name a few, have been pouring billions into the industry for the last decade and signs of increased investment are there.

Behind on social/online

Nintendo has really been behind on the social and online scenes over the past two decades. They have recently announced new plans to bolster their online offerings with an “expansion pack” offering access to N64 and Sega Genesis games for the first time for a price. I’m not convinced this type of offering solves the issues with the subpar online experience for Nintendo games. I think they have a long way to go to catch up to the Xbox, Playstation, and PC experiences with online gaming.

Smaller platform

As mentioned earlier, the downside to having Nintendo games (for the most part) only be available on Nintendo platforms means a much shorter reach for their games. This results in a fragility for future game releases being cut short in terms of reach compared to other popular franchises. It also means that the success of the business has and potentially will be overly sensitive to the success of adoption of their consoles.

Takeaways

The current valuation, solid balance sheet and future prospects leads me to believe that Nintendo is a “heads I win big, tails I don’t lose much” type of scenario.

The key driver to success will be flattening out the sales cycle that has harmed them in the past.

Over the medium term, I believe Nintendo needs to lengthen the console lifespan and continue to focus on putting out high quality games as well as work on improving their online presence.

Over the long term, they need to determine a way to expand their reach for their truly valuable games. I for one think that it is only a matter of time before they should rotate away from making consoles and deliver their value more broadly, even if that means giving up their beloved console with its current marketplace walled garden structure.

The ventures into theme parks, other media and toys should be treated as options or moonshots at this time. It appears the market is giving them no credit for these things which could actually strengthen their brand in the medium/long term.

NOTE: I do not currently own any stock in Nintendo.

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

If you enjoyed, please share with others and subscribe!

You can follow me on twitter @MoS_Investing