Galaxy Gaming $GLXZ

A small cap gamble?

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

Galaxy Gaming has a market cap of $117 million USD and trades on OTC markets as GLXZ. It is relatively illiquid in its average trading volume so keep that in mind if considering a position. It is headquartered in Las Vegas, NV. It has 36 employees and operates in several regulated end markets.

What They Do

They license proprietary casino games and products such as side bets to both land based casinos and i-gaming operators in regulated markets all over the world. They operate in a fast growing industry that is guarded against new entrants based on regional regulations.

Proprietary Table Games are grouped into two product types referred to as “Side Bets” and “Premium Games.” Side Bets are proprietary features and wagering options typically added to public domain games such as baccarat, pai gow poker, craps and blackjack table games. Examples of our Side Bets include 21+3®, Lucky Ladies® and Bonus Craps™. Examples of our Premium Games include Heads Up Hold ’em®, High Card Flush®, Cajun Stud® and Three Card Poker®. Generally, Premium Games generate higher revenue per table placement than the Side Bet games.

Enhanced Table Systems are electronic enhancements used on casino table games to add to player appeal and to enhance game security. An example in this category is our Bonus Jackpot System (“BJS”), an advanced electronic system installed on gaming tables designed to collect data by detecting player wagers and other game activities. This information is processed and used to improve casino operations by evaluating game play, to improve dealer efficiency and to reward players through the offering of jackpots and other bonusing mechanisms.

Excerpt from Galaxy Gaming 2021 10-K

Recurring Revenues and High Gross Margins

Revenues to casino platforms in both the i-gaming and table operations mean that basically all revenue is recurring with monthly billing. The cost of goods on the marginal product that is being sold is very low with reported margins being essentially 99%.

EBITDA margins have been around 25-30% over the past 5 years if you ignore the disruption in 2020 from Covid.

Importantly, marginal sales of their products have very little marginal cost and should provide ample cash to the bottom line. This is the key driver for their success - unlocking this operating leverage.

Clouds Clearing - Dispute with the Founder

The company settled a dispute with its founder and former CEO, Robert Saucier, on November 15, 2021. Saucier was in some hot water after dubious activities and an investigation by regulators. This overhang clearing should provide some relief from this contentious distraction.

On May 6, 2019, we redeemed all 23,271,667 shares of our common stock held by Triangulum Partners, LLC (“Triangulum”), an entity controlled by Robert B. Saucier (“Saucier”), Galaxy Gaming's founder, and, prior to the redemption, the holder of a majority of our outstanding common stock. Our Articles of Incorporation (the “Articles”) provide that if certain events occur in relation to a stockholder that is required to undergo a gaming suitability review or similar investigative process, we have the option to purchase all or any part of such stockholder’s shares at a price per share that is equal to the average closing share price over the thirty calendar days preceding the purchase. The average closing share price over the thirty calendar days preceding the redemption was $1.68 per share.

Activist Investor

Tice Brown has accumulated 5.9% of the company after starting to buy in January 2022 till present.

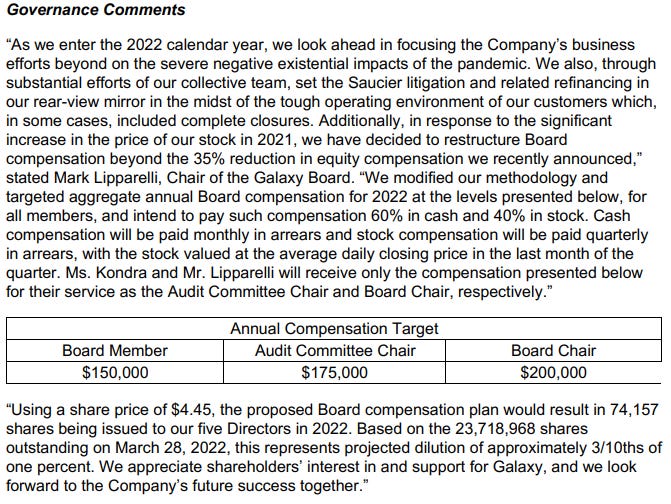

The filing states he is concerned mainly with the dilution of shareholders at the benefit of the board members with generous stock options and grants at prices below what he considers to be fair value given the trajectory of the business. He is requesting a board seat in attempt to influence the management in this direction. The below excerpt is from the 2021 earnings release and is pretty clearly in response to Tice Brown. It is still a bit odd to be paying directors on the board with this much of it in stock compensation, in my opinion and I doubt this response will fully satisfy the activist.

Some may see this as a distraction to management. Others will see it as progress in the right direction. I believe it will serve shareholders to hold management accountable as they have been rewarding themselves perhaps a bit too loosely in the past and getting away with it. Time will tell how this aspect plays out. It doesn’t sound like Tice Brown thinks the business operations are being run poorly. On the contrary, it appears that he thinks its a great business that isn’t fully aligned for the benefit of shareholders. This involvement will garner extra attention over the next few quarters at least and potentially make the business ripe for a takeover bid or a change to the board/management makeup.

Recent Acquisition

On August 21, 2020, Galaxy purchased PGP for $10.4 million. With a cash portion of the purchase of $6.4 million the remainder of the purchase funded by the issuance of 3,141,361 shares of the Company’s common stock. The stock was issued at $1.27 per share.

The background with PGP was that they were a customer/partner of Galaxy prior to this purchase. The contract was not favorable for Galaxy as PGP had exclusive distribution rights over Galaxy’s IP. With the exit of the founder, Saucier, there was an opportunity to cancel the contract and renegotiate terms.

Quality of the Business

A quick look at the margin structure and growth paints a pretty picture, indeed. A look at the 2019 margins likely paint a clearer picture compared with 2020/21 due to covid/purchase of PGP.

The EBITDA margins were at 29%, the operating margins at 20%. The business has produced free cash flow pretty consistently, if you ignore 2020 (which you should because casinos were shutdown or restricted in volume for much of it).

With the purchase of PGP, they should be able to control the brand quality to the end users better. The quality of the brand will ensure the value of the IP of its games and products are where they need it to be. They should be able to have substantial operating leverage as the development costs of these games and sales costs per customer should go down as the games are installed in more and more platforms, casinos, etc. If they can keep the current portion of the market they have while the market grows at double digits, they should enjoy even more free cash flow growth with this operating leverage.

Industry Tailwinds

I-gaming should continue to grow at low double digit growth for the next 5-10 years as it becomes more commonplace (both social acceptability and legalization in more regions of the world, including more states). The CEO has been on record as suggesting somewhere around 12% annual growth rate for the industry in which they operate. This is a conservative estimate given the organic growth and the opening of new markets to legalization, especially in the US.

There are a few drivers for individual states to adopt legalization of I-gaming.

Job creation

Tax revenue

Safer options for gamblers compared with alternatives

The tax revenue is quite lucrative and an easy lever to pull. The more states sign on to allow it, the more it will be an acceptable option socially. It’s really only a matter of time.

Moat and Competition

Gaining a license is challenging for new entrants. It is different depending on the region and in some cases both expensive and lengthy. With their experience, they will be able to enter new markets as they open up (although it will still be challenging and sometimes expensive) and they should maintain an advantage in the markets that they already operate in.

There is also some intangible moat with the recognized brand of the intellectual property such as 21 + 3. This should give some longevity and guard against operators trying to do these things themselves. Once players enjoy a game and feel comfortable with it, it can be like playing your favorite sport. Serious players don’t just switch.

Quality of Management

Insiders own a small amount of stock as shown in the table below. Notably, the CEO/CFO (Cravens, Hagerty) have options or were granted stock as part of their compensation. This is not the worst thing in the world but does dilute shareholders quite a lot given the size of the business. I’d prefer to see more purchases on the open market. In total, insiders own about 22% currently.

The current leadership team appear to be doing the right things with the operation of the business. The decision to buy PGP to take control of the middleman in that relationship was great for the longer term. The key thing to look for going forward is whether they can continue to grow the top line organically without much dilution or with large expensive valuations. It may be tempting to chase high top line growth given the growth of the industry. I suspect shareholders will do better with realistic growth that allows the costs to remain somewhat lower and thus benefit from the operating leverage that such a wonderful recurring revenue model can get.

Valuation

Right now, at a market cap around $117 million, you are paying around 4.5X 2022 estimates for revenue and about 12X EBITDA. If they are able to sustain 15% growth annually for another 5-10 years (to match the industry), and improve the EBITDA margin towards 40% as they scale (with operating leverage discussed), then the current price seems fairly reasonable. The share price has risen a lot in the recent few months so it’s unlikely you get a gangbuster return over the near term based on fundamental valuations but there is potential for a long term compounder here that shouldn’t be completely ignored based on multiples alone.

The medium term kicker would be that if they are able to go up in size, more investors would be take notice and a high margin recurring business like this one could very well be valued by a bull market at much higher valuations.

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

That’s it for now, let me know what you think on twitter @MoS_Investing or in the comments! Please tell your friends about my work if you could, it helps me a lot.

Right I also read that and that news bring me to GLXZ, you researched GLXZ and TBTC. It seems you absolutely researched the igaming industry, so wondering why you prefer GLXZ to EVO. Also, I really enjoy all of your research and will introduce to some other friends.

Why not just buy EVO?