Kelly Partners Group Holdings $KPG.AX

Taking advantage of “A great business poorly done"

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

“Pick an industry where you can play long term games with long term people.”

- Naval Ravikant

Kelly Partners Group Holdings (KPG) is a microcap business listed on the Australian exchange. It IPO’d in 2017 but has been in business since 2007. It is founder led, has high insider ownership, and is trying to emulate some of the great capital allocators and business models out there. It has a market cap around $ 220 M AUD.

I believe this is a gem that could go on to do wonderful things for shareholders for those who are patient and have a long term time horizon. There are many signs that this is a wonderful business run by talented, focused and shareholder friendly management. This stock is too small and illiquid for even most small funds to purchase and is not well known.

The business should be able to reliably grow at 15%+ top line growth for a very long time as they continue to focus on what they have done to date. The underlying unit economics and quality of the recurring revenue is high and they could sustain an advantage over the competition while offering value to their customers and partners. They operate in a boring, steady, slow growth industry where they can take market share through organic reinvestment and through many small acquisitions. They can do this by continuing to aggregate a large fragmented industry with a model that would not be easy to replicate by most competition.

Liquidity is a concern of the short-term investor and a minor matter for the long-term investor.

Peter Bernstein

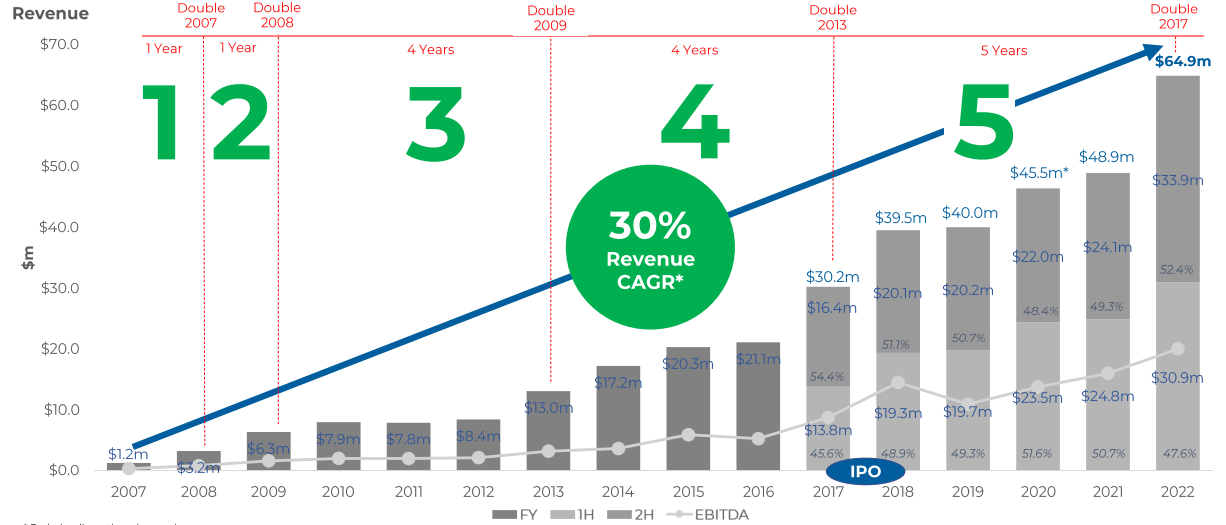

To give you a sense of the history since becoming public via IPO in 2017, the table below highlights the business fundamentals that has rewarded shareholders since that time. The number of operating businesses, the revenue and earnings per share growth is the highlight. Interesting to note that the valuation has appreciated somewhat as you see the share price has outpaced most fundamental metrics.

For the remainder, I’ll go over the business, the management, the quality growth opportunities that it may have and how durable the model could be. I’ll also discuss some of the capital allocation levers available to the business and some potential risks and drawbacks.

What They Do

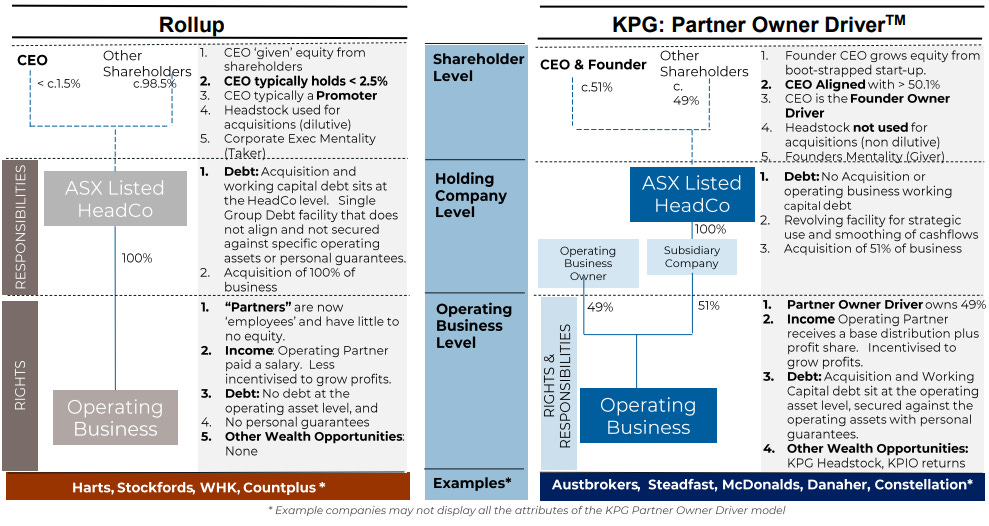

The business model is a serial acquirer of partnerships with small accounting firms. They buy a controlling stake, make improvements to operations and allow the working partner to focus on the client business relationship and service. The management team presents the model as a “Partner-Owner-Driver” model. It distinguishes itself from a rollup in that it aims to align incentives with the operator partners of the underlying businesses, avoids equity dilution for acquisitions, and ensures that debt is used in sensible ways.

What KPG is really trying to do is to take advantage of “a great business poorly done”. The accounting business fundamentally is wonderful in that it has recession resistant recurring revenue with low customer churn and low capital requirements to sustain operations. The issue tends to be structural with smaller firms in that the partners tend to pay out all the profits every year instead of reinvesting for growth and durability. There is an opportunity here to take the right partners, and repeat in a serial acquisition model with a highly fragmented industry, it could be a recipe for long term success, so long as they continue to scale. The advantage they have is that they are led by a long term oriented and focused leader with the experience and understanding of the underlying businesses that other financial deal makers would lack. Those with the experience and expertise are unlikely to have the drive and focus to repeat what Kelly has done when you consider the patience and deal making required to duplicate such a model.

To demonstrate the a measure of quality revenues in this SME (small and medium enterprises) accounting business, consider the following set of quotes from a recent Invest like the Best podcast with William Thorndike, an investor in KPG and the acclaimed author of The Outsiders (which I recommend you read, by the way).

We've really become zeroed in on revenue quality. So the purest form of that is it a recurring revenue business? And if so, what's the churn profile?

…And what we've found is there's disproportionate power in truly low churn businesses. And when I say churn, I mean, logo churn, gross churn, net revenue retention is, there are other metrics that are important as well, but really at the core of it is you start the year with a 100 customers, how many do you end the year with and why are there structural reasons for that? And so if you look across those companies, they tend to have this element of revenue persistence.

…And so you have great visibility, predictability on your revenue stream around which you can then do a whole range of other things in terms of how you organize the company, whether you choose a decentralized organizational form, how you think about financing the company. It has a dramatic impact on your capital allocation menu of alternatives.

…industries that are characterized by very low churn are just interesting places to be looking for these sorts of long holding period platforms.

William Thorndike

Management Quality

The founder and CEO, Brett Kelly, has 30 years of experience in the industry. He appears to be focused on the long term success of this business, which to be fair, has his name on it. In his mind, this is his baby. He discusses how he studies the greats in investing and business. He typically references, quotes and provides book recommendations during his shareholding meetings which are related to the best all time investors and CEO’s. Berkshire Hathaway (Warren Buffett), Constellation Software, LVMH are often referenced. What I find interesting is that while he has studied the great successes, he is also analyzing why they worked where and when they did. He is not simply copying one particular model but rather looking for mental models and structures that could apply to KPG.

Brett owns roughly half the business. That is a great sign to me. He is rewarded with shareholders along the way.

The incentives of the partners are clear, continue with long term growth at the operating business and get rewarded with cash. There are no stock based compensation or options for the management team at the parent either. While this is good in terms of dilution, it wouldn’t be bad to have something other than cash based performance to ensure skin-in-game for the management team (other than the CEO).

Lawrence Cunningham was put on the board this year as a non-executive director. He is the Constellation Software vice chair and author of Quality Shareholders - How the best managers attract and keep them. He apparently advised Brett on keeping to the high number of small acquisitions. I can’t imagine this wasn’t helped with his experience at Constellation since 2017.

Given the nature of this business model - the serial acquirer/partnership model - I recommend you become 100% comfortable with having your capital invested with this management team before considering an investment. In every business, the management team is important but even more so here as they are going to be making very important capital allocation decisions which will have meaningful impact to outcomes.

Business Quality

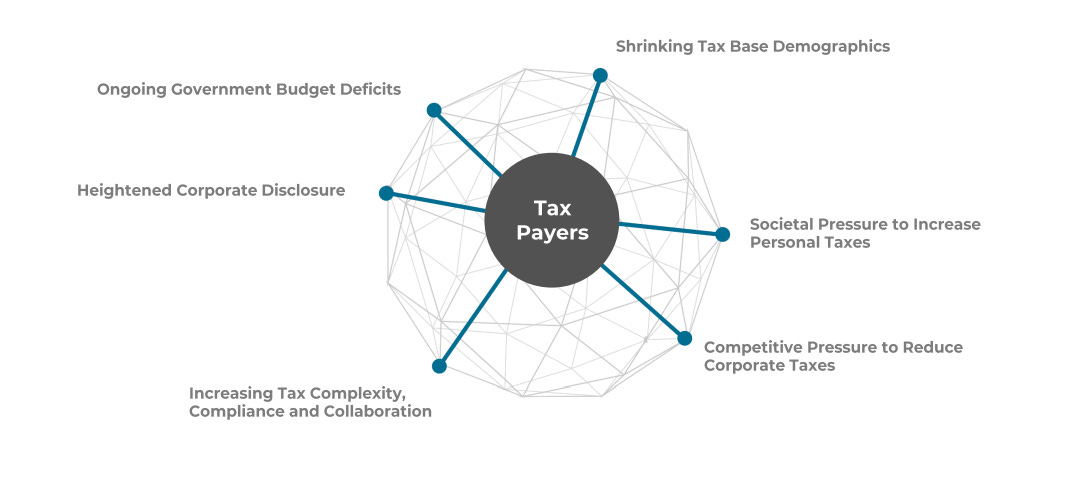

Taxes are recurring and the need to get support for filing and other assistance is just as much a recurring business, often with repeat clients based on longstanding business relationships that end up being the default either by the mere fact of low local competition, comfort, etc. Tax code isn’t going away and is constantly changing. For most customers, this is a relatively small cost of their operations and yet is critical and valuable.

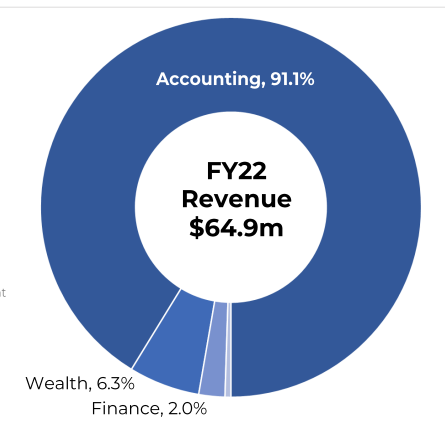

Gross margins are better than industry average and have consistently been ~60% since the IPO. EBIDTA margin is ~33% and is anticipated to grow slightly. ROIC (return on invested capital) has been 20%+ consistently and ROE (return on equity) has been 40%+.

While the majority of revenues currently come from the accounting services, expect the complimentary services to increase slowly over time but the majority will ultimately still be where it is today.

Where the durable advantage lies is with the fact that accountants (generally) don’t want to be business owners. Thesis is to aggregate and improve an existing large fragmented industry.

What’s in it for the sellers? According to the the CEO, the acquired business partners have many benefits compared to going it alone. He refers to the following:

~40% time back to accountants

Improved margins and increased revenue means double the profits

Reduce working capital by ~2/3

For the right partners, this is an alluring synergy when combined with a buyout for the controlling interest would be compelling.

Growth Opportunities

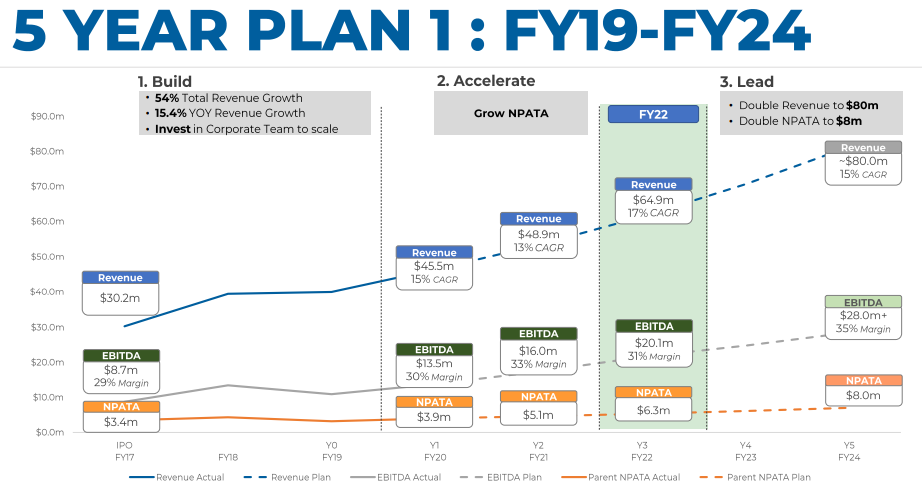

The management team has had 5 year plans in place. You can see what they are shooting for in 2024 from where they are now. Essentially they are aiming to increase EBITDA margins and get to $8.0m in NPATA (net profit after tax and amortization).

One of the keys to being able to scale will be building a capable management team that can duplicate the recipe at scale. This will be a challenging one to see prior to observing results, unfortunately.

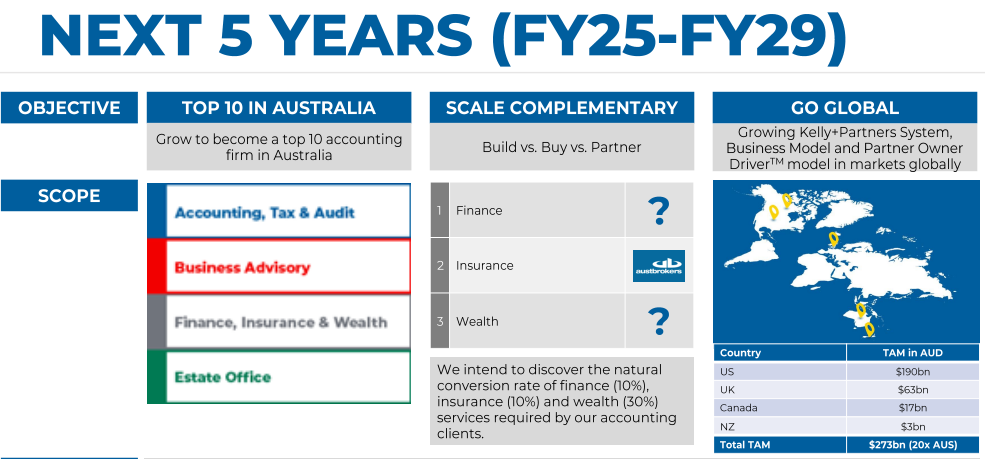

If that wasn’t enough they also communicate ambitious next stage of the future growth (2025-2030). It is centered around taking a global expansion with more capable offerings in the complementary business services that their clients often need. They have a goal of being in the top 10 accounting firms in Australia by then.

Organic growth has been done by reinvesting 9% of revenue back into the parent for improvements. I would expect this to slow down as a percentage and the limits to organic growth as a whole once the business reaches a larger size. Organic growth is not something that is expected to be linear so would need to monitor this over a few years to understand the success/failure of the reinvestments.

Most of the longer term growth opportunities that they intend to tackle will be an international expansion. Notably, they are aiming at similar western world English speaking countries. No doubt this is an applaudable approach as it is likely to be business that is similar to Australia compared with the rest of the world. So far, Brett has commented that New Zealand, Canada and the UK would likely be the first markets to tackle. I think this is wise as it is likely that these markets are most familiar in how they operate. The US is a large market but may not be as easy to enter.

Capital Allocation

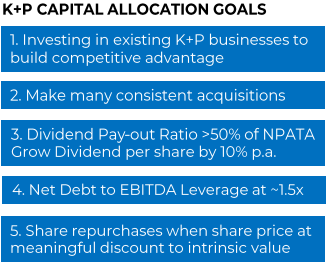

Brett and company speak in a straightforward manner regarding capital allocation. The only issue that I personally have is with the dividend. With relatively high return opportunities, I simply don’t understand the fixation on the monthly dividend. While I understand it can bring long term dividend investors, I don’t think it creates the most value for shareholders over that period and for that reason, I’d prefer if they de-emphasized it over time. If they took a page from Constellation Software, they could simply maintain the dividend and avoid special dividends to instead look for better opportunities to reinvest. Perhaps they don’t have the infrastructure and organization capacity at this time to take on that level of reinvestment and acquisitions, which I can appreciate may be challenging.

Realistically, the illiquid and small market cap makes share repurchases at opportune times a challenging lever to pull but with time perhaps there will be meaningful opportunities. Right now, the top three seem like the real drivers.

Acquisitions

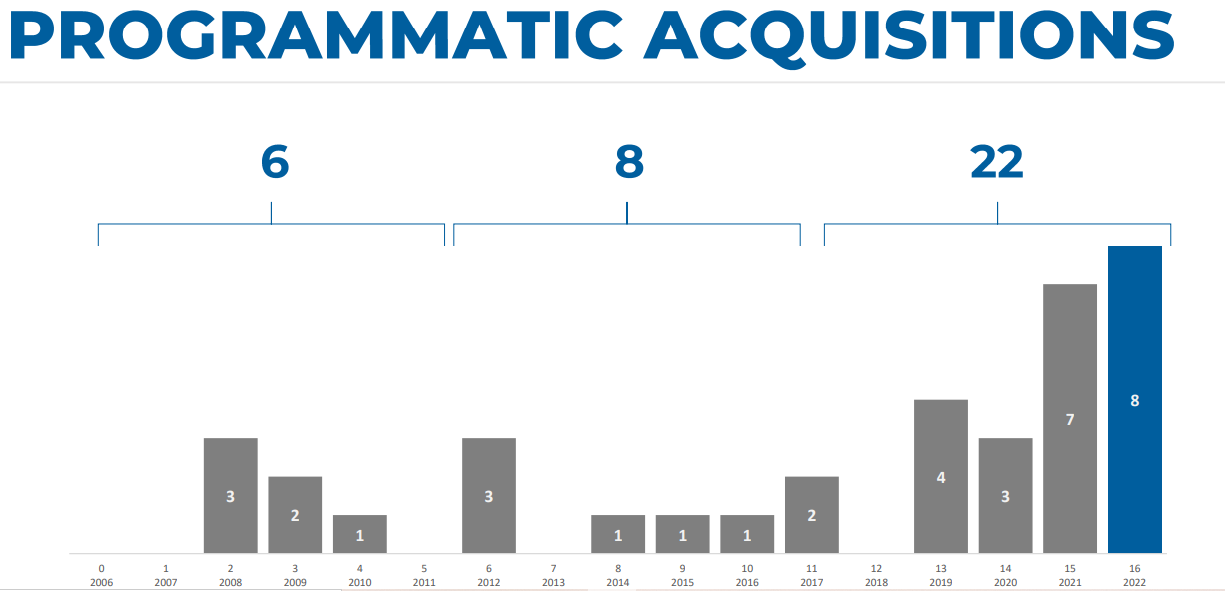

I think it’s fair to say the largest future value creation is likely to come through continued acquisitions. The biggest concern most people (rightly) have with serial acquirers is that they chase larger and larger acquisitions or they drift outside their circle of competence operationally and get into complex situations which they can’t handle. The addition of Lawrence Cunningham to the board is a welcome sign in this regard. Having the vice-chair of Constellation Software, a company with (in my opinion) the best track record of being able to sustain growth with acquisitions over long periods can’t possibly be bad. Brett has eluded to this in a few conversations where he is clearly going to take the lesson from the likes of Constellation and continue to focus on many small deals.

So far, it is clear they are and should be able to continue to grow the number of acquisitions. Eventually, they may need to make some tough decisions organizationally in terms of how to handle the volume of acquisitions if it continues to grow. So far their largest has been around $8 million and they aren’t looking to scale in size of deals. Otherwise, the growth rate will need to drop. Unlike Constellation, KPG is only decentralized when it comes to the individual operating businesses, not the capital allocation.

Dividends

The company is aiming to payout 50% of NPATA and grow it by 10% per year. I don’t see why they couldn’t do that for a while from here as long as the model continues to execute. The dividend is paid monthly with a larger portion paid in July or August typically.

Stock Repurchases

They have repurchased a small number of shares to get the shares outstanding down to a nice round 45 million. Brett has commented several times that they will look to do repurchases whenever possible which means when they aren’t in a blackout period (when they are allowed due to ongoing deals, etc.). Given how illiquid the stock trades, I don’t see this as being an easy lever to pull but they could look at other non-market opportunities such as tender offers or Dutch auctions.

Risks

I’ll keep this short and sweet. These are the risks I’d be concerned and monitoring as a shareholder:

The pace of acquisitions. As they grow in size, how are they able to scale?

Expansion into other markets. This is often a challenge for businesses who understand one geographic market but not the new ones they enter. Look for patience and honesty.

Slowdown in organic growth. As they grow in the number of firms, they will have a tougher time on the whole in squeezing the same organic growth rates and/or will have less opportunity to reinvest this way.

Key man risk. Brett seems like a key to the long term success. He has spoken about succession plans being in place but it would be hard to replace someone who founded the business and has this focus with someone else.

Valuation

Given the company is clear about their capital allocation and growth projections, I think its reasonable to look at a few different scenarios from today’s price and put a rough estimate on expected forward returns from here.

For each of the three scenarios, I will simply use an approximation for forward returns. This is a rough estimate and should include many other details if you wished to model it out.

Forward Return = Dividend Yield (%) + Growth in EPS (%)

Scenario 1: Exceeding Expectations

Return = 1.3 + 17 = 18.3%

Scenario 2: Meeting Expectations

Return = 1.3 + 12 = 13.3%

Scenario 3: Missing Expectations

Return = 1.3 + 8 = 9.3%

Obviously, the trick here is to be comfortable in understanding the risks more so that you could be comfortable in narrowing down the expected outcomes. The current price and the current management projections makes me believe that the base case of meeting expectations seems like a reasonable return but does not give a huge margin if things go wrong. This is certainly not a suggestion to buy or sell but merely a way to quickly try to think about potential returns.

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

That’s it for now, check back soon for more. As always, follow me on twitter and please share this with anyone who might interested in my work. My work is now completely free for all but there is an option for a low cost paid subscription as a way to support my work.

Great writeup, Simon! Kelly Partners is such a beautiful company

Nice writeup! Thanks for opening this one up. Just curious how are you deriving these forward returns (growth in EPS)? What are the key assumptions and differences between the three scenarios?