Vitalhub $VHI.TO

A microcap serial acquirer in the healthcare software space

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

DISCLOSURE: I own a small amount of shares in the business discussed below at the time of publication. The below is not a recommendation of any kind and you should recognize that it is likely that I’m biased.

Vitalhub is a small publicly listed company that is becoming a serial acquirer of software businesses in the medical enterprise software market. The company is headquartered in Toronto. So far, they have a presence in Canada, the US and the UK. They are publicly traded on the Toronto Stock Exchange with the ticker symbol VHI. The market cap is around 100 million Canadian dollars.

I believe there is an opportunity here to get in early with a serial acquirer with a reasonable valuation, net cash on the balance sheet, and an experienced management team. Coupled with insider ownership demonstrating potential aligned incentives for future growth. There are, of course, a series of warning signs that should be considered first.

What They Do

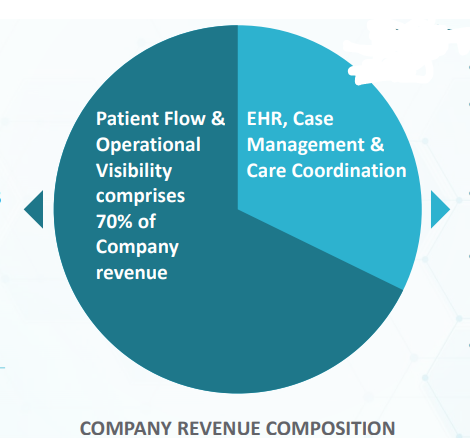

The company owns small enterprise software businesses in the healthcare marketplace. They currently own a slew of these and divide them broadly into two categories.

Electronic Health Records, Case Management and Care Coordination

Patient Flow and Operational Visibility

According to the company, about 70% of revenues are derived from the patient flow and operational visibility portion of the businesses. They also claim to have recurring revenues around 80% of the total with gross margins in around 70-75% recently.

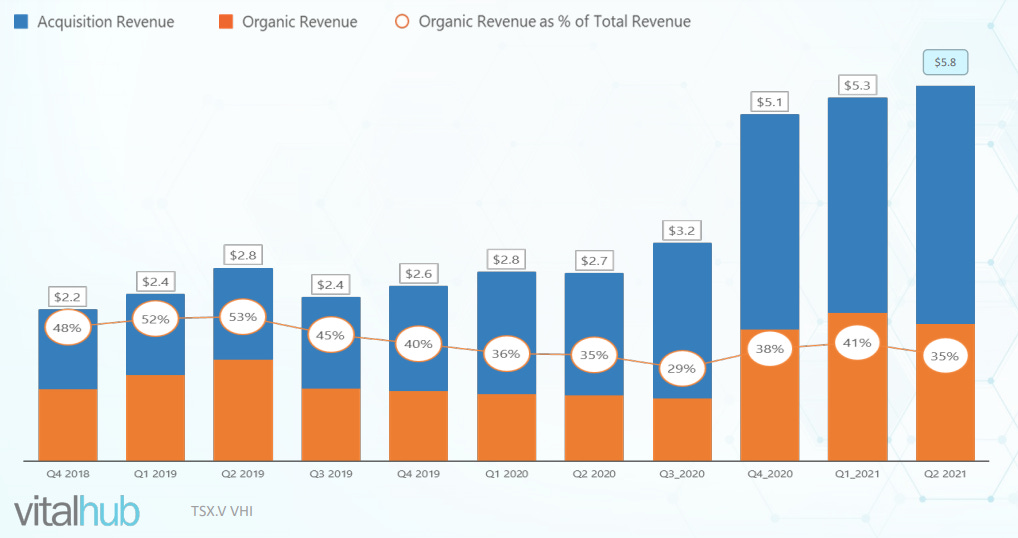

Their plans for the future include growth in topline revenues from both organic and inorganic means via repeated acquisitions. In September 2021, they’ve been uplisted from the venture exchange to the main board on the Toronto Stock Exchange.

Bull Case

Quality and Moat of the Business

A pure software business filling a niche market means that gross margins will be high. Gross margins should be in the 80% margin region in a mature state if you look at the software industry in general. The recurring nature of the majority of revenues and the boring nature of the offering is compelling as there is less desire for customers to switch. This is a potential moat for niche software in general. With health care, there is even more stickiness likely given the heavy administrative nature and constraints limiting quick changes or upgrades. As the software is a vital part of the operation for customers, there is little appetite to switch to a competitor if not forced to.

Management Team and their DNA

There are several members of the management team and the strategic investors that have had past success in previous business ventures.

The CEO, Dan Matlow is the founder. He had previously worked in the industry (30 years of experience is referenced) and spent time at Open Text, with Healthcare IT sales as a VP. After leaving Open Text, he started Medworxx which did similar things as VitalHub.. He sold Medworxx, after it went public, to Lorian Capital group for a reasonable profit. Listening to conversations with Dan, you get the sense that he regrets focusing so much on growing that company primarily through organic means and wishes he would have done more acquisitions to enhance the growth. I think this is a reasonably good sign that he is learning from his experience to focus on acquisitions that are beneficial to shareholders and not solely focusing on organic growth. Dan owns a small part of the business, currently owning around 850,000 shares or less than 3%.

Other members of the management team have spent years in this sector doing similar things, and have a wealth of acquisition experience as well. The other notable characters to discuss in this plot is Francis and Tony Shen. They are associated with Aastra Technologies, a business that Francis and Tony founded, took public in 1996, and sold for around 400 million dollars in 2013. While at Aastra, the businessmen did several acquisitions and managed to grow the business rather successfully in different regions throughout the world. Francis owns a significant stake at just over 4,000,000 shares or just over 10%. Francis has a history of successful acquisitions with Aastra and heads up the M&A committee for Vitalhub. When combined with the significant ownership, it tells me the true path for growth is for many acquisitions going forward.

Growth From a Small Base

The company is still quite small, around 100 million dollar market cap and have around 20ish million in cash (at the time of writing). They plan to continue to grow by using the cash on further acquisitions and organic growth initiatives. The organic growth will be more challenging but also potentially high rates of return if they can execute properly. The ability to cross sell and get new contracts with new or existing customers will be the key for the organic growth and only time will tell how sustainable they can be.

For individual investors, one of the advantages will continue to be lack of large funds being able to invest and make the valuation sky high for some time. The stock has 5 analysts covering it currently but it is far too small and illiquid to attract big funds.

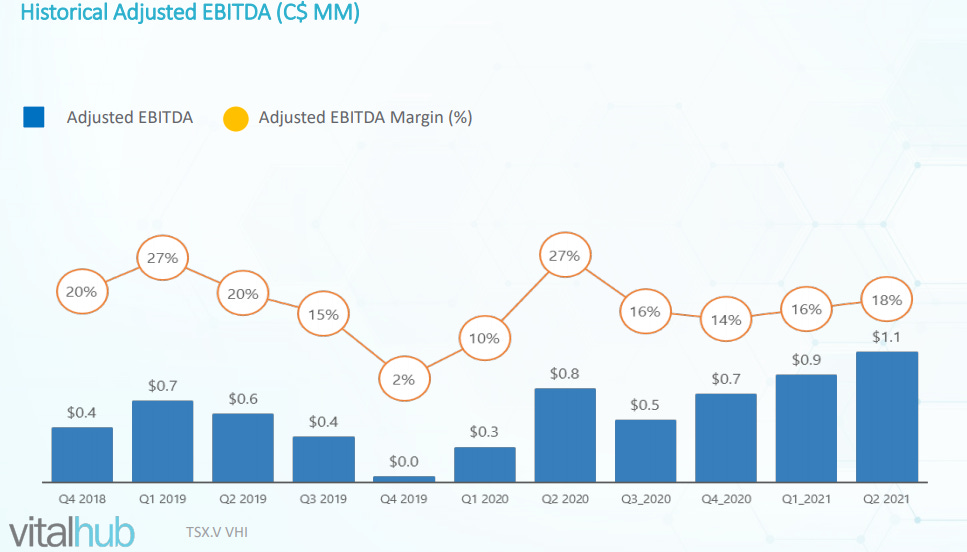

Margins Expected to Improve

The hope to get to 20% EBITDA margins as they expand and save on overhead, gain synergies through cross-selling and other means of inorganic growth.

They use an “adjusted EBITDA” to try to smooth out the bumpy nature of acquisitions. I would prefer they get to a point where they can use some other measure as this could be misleading. That being said, they continue to improve as of late and could see hitting their targets soon.

Organic Growth and Secular Tailwinds

There is little doubt that hospitals and other medical businesses and facilities have been hit hard by the Covid19 pandemic. Their systems, resources and staff have been pushed to the limits and beyond at times. I suspect there has been short term pain on the business aspects of these institutions and they will likely continue to look to modernize to make operations more efficient and to alleviate some of the heavy administrative burden on staff. Further, if there is a continued shortage of trained professionals in some regions of the world, I would think organizations will seek to move in this direction and quickly.

I would hope this is a tailwind that pushes organic growth for Vitalhub, but only time will tell. They have said they are focused on Europe as the best potential for future growth and I believe a very fragmented market coupled with ageing populations will be a secular driver for organic and inorganic growth in the region.

Fragmented Market for M&A

They have quoted around 400 acquisition targets that they are following that are within the markets they serve. The CEO also has mentioned that there are around 100 targets that would fit nicely in with the current product/service offerings. This gives you an idea about the potential for a number of years of steady acquisitions, if they can be competitive at bidding for these businesses. I think it is fair to say there is a nice runway for at least a decade, if they can execute and get the cash flows to fund these acquisitions and be disciplined to not pay too much. Given the amount of past experience, I feel that there is a real chance of success on this front.

They claim to target businesses with 1-12 million in revenues, with at least 60% of it recurring (SaaS) and be profitable. I would prefer they stick to small targets in the 5-10 million dollar price tag for as long as possible as they will have a chance at getting them at fair prices. They claim to target paying 1-2.5X sales which is in line with targets from the likes of Constellation Software’s history with small acquisitions.

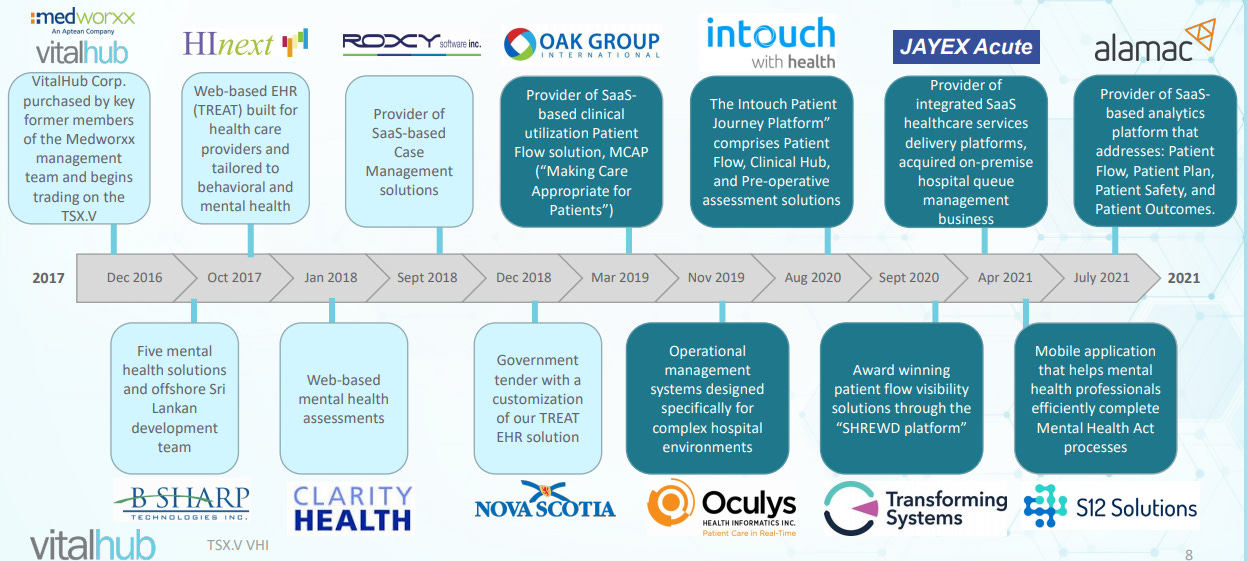

The recent history of acquisitions are listed below since becoming public in 2016.

Reasonable Valuation

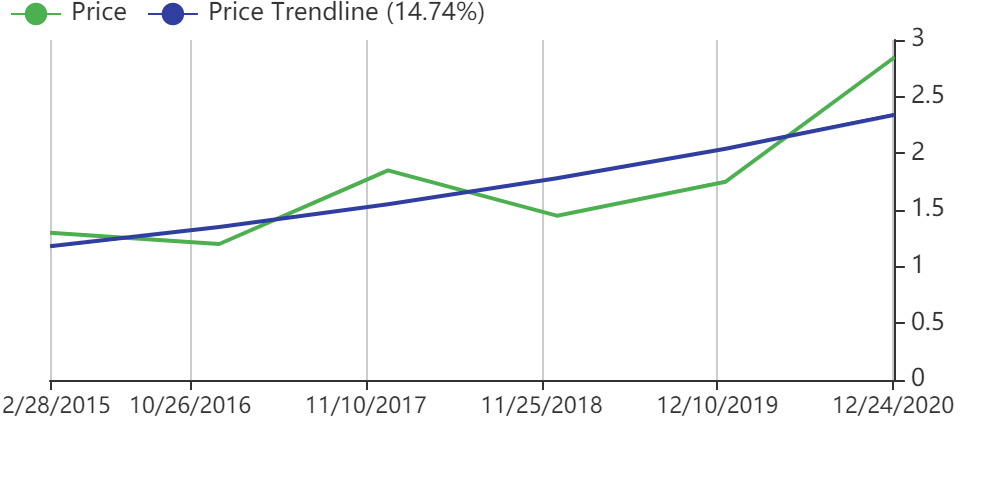

With the stock price around 3$ CAD per share, the business is available for around 4-5 times sales with a good chance it doubles revenue over the next 3 years or even potentially sooner. While it is true that there is risk of further dilution, this is a relatively cheap price to pay for this type of serial acquirer when compared to the veteran big players doing similar things. Both Constellation Software and Jack Henry demands a market valuation of roughly 7 times sales with less capacity for future growth given their size. The trade off here is, of course, a proven track record and a well understood culture of aligning growth with shareholder value. So I believe there is no real “free lunch” with this comparison. You are getting a better price for the cost of some execution uncertainty. That being said, there is potentially much more upside to be had over a shorter period of time with this small cap compared with those behemoths.

I’m not a huge fan of deciding if valuation is great based on relative comparisons, but that is one perspective. The other thing to consider here is the potential future prospects vs the price paid today. If you believe that growth rates can continue around 20% or more a year for the next decade, then you would be looking at a business with around 120 million in revenues. With no real multiple rerating from here, you would have yourself a 5X or 6X return over that decade. If you assume they can get more cash flow to go after more acquisitions, then you would end up with a much higher return potentially.

Bear Case

Share Dilution

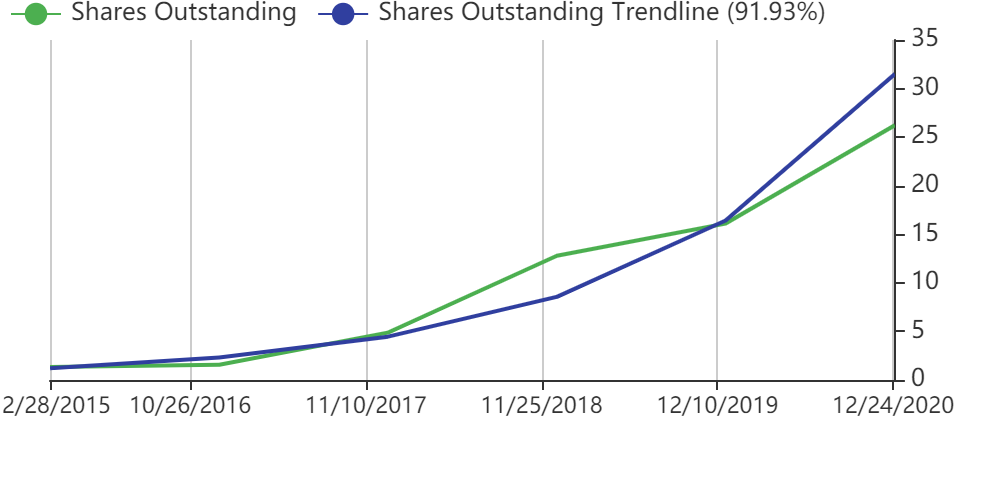

The ugliest part of this story. This is something that many small cap companies do that is sometimes required to grow at a reasonable pace in the early years. The management team, since it was founded, has consistently diluted common shareholders to fund the balance sheet. That being said, the price gains per share have made up for that dilution to provide a reasonably adequate return to date (about 5 years).

Cost of Capital

Access to cheap long term financing and covenant light structured debt may not be readily accessible for a relatively small company compared to bigger players in the industry. While it’s possible this improves, it may take a long time, if ever, to get the best financing. I suspect this is why they have been accessing capital with issuance of common shares. Now that the company is listed on the main exchange and will soon not need external financing, I hope this is a thing of the past. It could be a bad habit that lingers.

The best serial acquirers run with no external financing (use cash flows for acquisitions or use conservative amounts of debt structured appropriately). I will need to see them change their ways in this regard to fully buy into the concept.

Stiff Competition

Private equity or public companies would love to scoop up software businesses and have the funds to do so. Some will not think twice about spending higher prices then what would otherwise offer a great return expectation.

There is also the Constellation Software’s and Jack Henry’s of the world that are better connected with the network of founders that will offer good long term homes to those looking to sell their small software businesses. It is possible that the reputation for a being a good owner is not necessarily the same for Vitalhub at this point in time.

I do believe that growth via acquisitions will be required for this investment to be successful, so this execution of buying up targets at fair prices is crucial to the thesis.

Potential to Overpay for Acquisitions

On a related note to the above, it is possible that they extend their reach too much and overpay for acquisitions in an effort to grow at all means necessary. Growth should be a choice, not an imperative. It is very tempting to grow as fast as possible if the cash or financing is available to do so.

Focus on Synergies

There are numerous times in the filings and investor presentations that synergies for cost savings and cross selling opportunities are referenced as positives. While it is theoretically true that there are benefits there to be had, it tends to be tricky to execute and not be as meaningful once all the complexities are taken into account. I’m healthily skeptical that all of these benefits will come to fruition but am cautiously optimistic that some will come to bear.

There is no doubt that some corporate overhead costs will remain relatively flat as the company grows in size with acquisitions and margins should indeed improve. I’d still like to point this out as a red flag and potential trap.

International R&D Staff Exposure

The company has a subsidiary operation that provides some R&D from Sri-Lanka. This is presented as a cost-savings advantage for the business. I’m less certain of this. There is challenges with having such an organization so far from home-base, not to mention the geo-political risks and there should be questions regarding the quality of the work given the misalignment of incentives here. It is not a good sign to see stakeholders such as employees spoken of as a resource that is a low cost advantage. This is the extreme case, and perhaps it is not as bleak as I make it sound. Nevertheless, I cautiously view this as a risk, not an advantage.

Early Exit Potential

It is potential that due to stock market volatility or some bad operational events or news, that the stock market drops to a point where they become a takeover target and long term shareholders could suffer by having their returns cut off prematurely. Even if the buyout is positive in the short term for shareholders, I would prefer to invest for the long term and allow the business to compound for long periods. If you are shorter term trader or investor, this could potentially work as a bull case depending on the scenario but it is not for me.

If you enjoyed the writeup, check out my other content on constellation software here: Constellation Software - Quick Take

My take on what makes serial acquirers successful here: Serial Acquirers - Growth via Acquisitions

As always, please share and subscribe for future content directly to your email. You can also follow me on twitter!