OneWater Marine $ONEW

A serial acquirer in choppy waters

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

OneWater Marine trades on the NASDAQ with the symbol ONEW 0.00%↑ and has a market cap of $500 m USD. It has a long history dating back to 1987 where it was a one store family owned business operating a single boat dealer location. It stayed that way until the economic downturn in 2008 when many mom and pop operators went under or didn’t have any succession plans in place. The ONEW team opportunistically acquired 8 businesses and since then have been a successful serial acquirer, rolling up the space. They have steadily acquired more stores and have grown their network to 75 as of May 2022 and now offer many more offerings and have made efforts to expand their maintenance and parts business.

For those looking for compelling growth with a view on consumer discretionary spend continuing to be stronger than what the market is pricing, this one could offer high rewards over a few years.

Margin of Safety Investing is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Let’s dive a little deeper into the business, the management, the risks and a look at valuation.

What They Do

ONEW owns and operates a network of independently branded boat dealers and other marine related parts and service businesses. They acquire smaller dealers in a very fragmented industry. They have OEM suppliers that they place orders with and maintain a certain inventory of boats and parts for their businesses based on expected demand. They utilize backend data to leverage their growing network of dealers across mainly the southeastern states.

The business is as seasonal as you can imagine. They build up inventory over the winter and draw down with higher sales in spring and summer months. The new boat sales account for 70% of revenue, whereas used sales have been 16% and parts and maintenance accounts for a growing but smaller 11%, albeit at a higher margin. Expect the parts and maintenance mix to increase over the next few years as they set out to grow that side of the business.

Business Quality

The unit economics are simply not amazing for a boat dealer but are slightly better for a parts and maintenance operation. That being said, the roll up model coupled with some operating leverage capabilities with a larger network of locations do result in a business that can produce good free cash flow through most of the cycle.

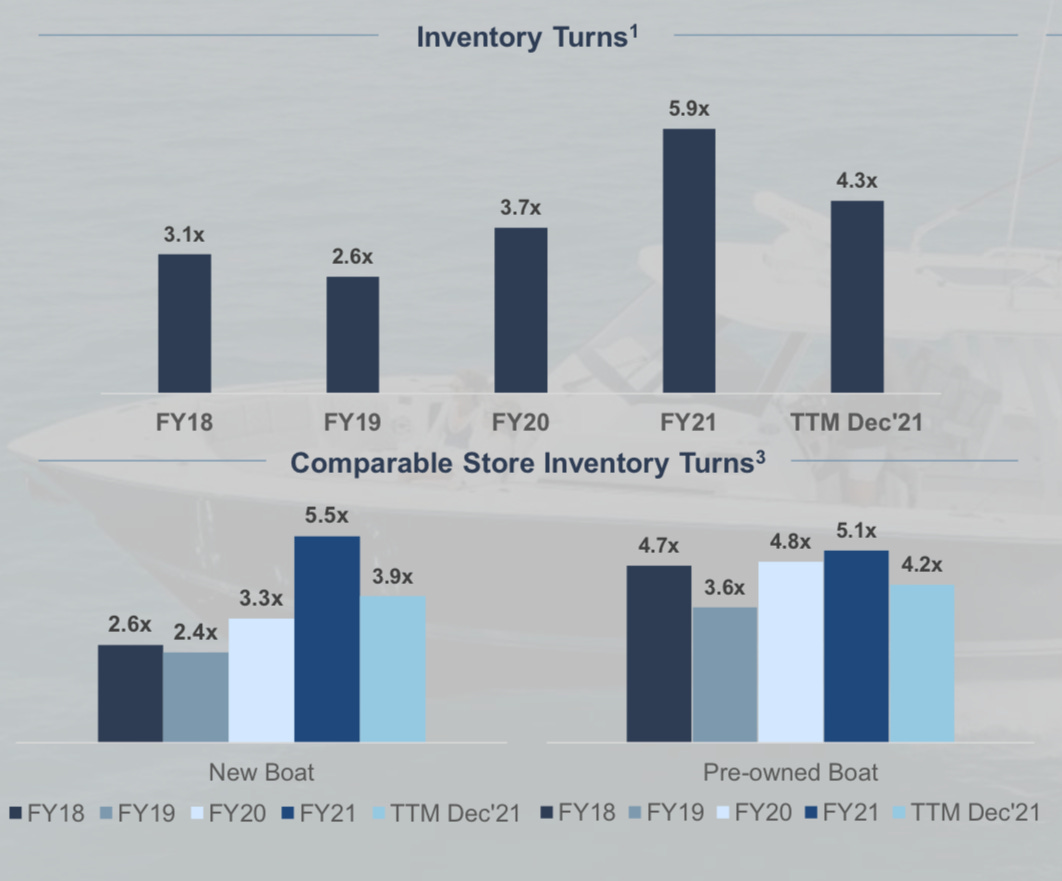

The other aspect of the business that has evolved with the strong demand since 2020 coupled with restricted supply has been that turns have increased as a result. The capital efficiency has therefore increased and management has taken notice. I suspect this may end up becoming a “new normal” as opposed to temporary phenomena. Management has made this comment as well and there are signs that the OEMs would be happy with this too.

Overall, the business quality is objectively not high. That’s not to say it is a bad business, but you are relying more on the capital allocation of the management and shrewd cost management of the operations teams to ensure that the value accrues to shareholders over time.

Growth Prospects

The management team has been clear about their acquisition strategy going forward:

Acquire 4-6 boat dealers

Acquire 2-4 parts/maintenance businesses

Expect these targets to grow again in a few years as they continue to fund more and larger acquisitions. What you need to watch for is discipline in their purchases. It is often tempting to pay up for more sizeable purchases that can have a bigger revenue growth impact. The truth is that these larger businesses could mean lower return on investment as improvements to operations will be less and price paid will be higher.

Organic sales growth and margin expansion is based on the industry tailwind that the business is hoping to ride is related to newer modern boat designs making a leap forward.

Of the approximately 1,105,000 powerboats sold in the United States each year, 79% of total units sold (approximately 875,000) are pre-owned. Relative demand for new and late-model boats has increased in recent years in part due to the continuous evolution of boat technology and design including, but not limited to, seating configurations, power, efficiency, instrumentation and electronics, and wakesurf gates, each of which represents a material design improvement that cannot be matched by more dated boat models. We believe the increasing pace of innovation in technology and design will result in more frequent upgrade purchases and ultimately higher sales volumes of new and late-model, pre-owned boat sales.

Source: ONEW 2021 10-K filing

Industry Fragmentation

The boating industry is highly fragmented and there is plenty of small businesses to acquire for a very long runway of growth. ONEW claims to have just under 4% of the dealer market with it’s only significant competitor of size being Marine Max (HZO on the NYSE). Marine Max supposedly has a slightly larger share of the market but is comparable.

The boat dealership market is highly fragmented and is comprised of approximately 4,300 stores nationwide.

Source: ONEW 2021 10-K filing

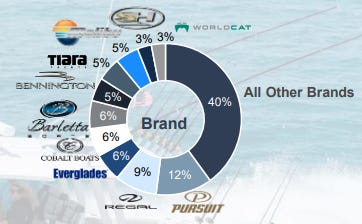

OEM suppliers are also not terribly concentrated so they do not have too much leverage over other parts of the value chain. As you can see below, the suppliers that work with the ONEW network are not at all concentrated with the largest being 12% of revenue.

The operational advantage that this fragmented industry provides the larger players is the ability to have lower inventory and maintain customer demands. Boats can be moved to wherever the demand is. This leads to an advantage in lean supply times such as these where customers can benefit from inventory that is nowhere near the actual point of sale. During normal times this also allows lower inventory requirements per store and therefore lower working capital requirements overall. Couple this with having lower unsold inventory at the end of the season and this is an all-weather advantage that will become more robust with the size of the network.

Building Resilience

The main strategic focus over the last few years has been to reduce the cyclic exposure to boat sales by growing their parts and maintenance business. This is a higher margin and less cyclical revenue stream. Boaters will maintain their boats more routinely even in the face of economic recessions whereas new and even used sales will fall drastically at the end of economic cycles that pressure consumers’ wallets and their appetite for large discretionary purchases.

They have recently made a large acquisition in T-H Marine in this area. This was a significant purchase for the company as it nearly tripled their parts and maintenance revenue contribution. The purchase was completed in 2021 at a price of $185 m ($182 m in cash and $ 7 m in stock). With some smaller purchases going forward, they should be able to enhance this contribution further still to reduce risk of cycle exposure. This is still too small of a percentage to suggest it is a robust measure yet.

This part of the business model going forward may end up resembling to a small degree what Pool Corp. has been able to do with it’s sales mix which makes it’s revenue much more predictable, recurring, less cyclic, and higher margin. The biggest disadvantage that boats have compared with pools is they are more easily disposed of, even if at a loss. Unfortunately, this means a lower quality business compared to that of Pool Corp.’s.

Management Quality

Insiders own approximately 21% of the shares outstanding. They have steadily grown margins over the past few years and have returned capital to shareholders and have demonstrated a sensible approach with the recent $50 m buyback program.

The executive team has plenty of industry experience and appears to know what they are doing when it comes to acquiring and integrating the new stores. I think it is a wise choice to pivot to focus on the higher margin, less cyclical parts and maintenance businesses as it gives them a lot robustness in their revenues.

Capital Allocation

The entire strategy for growth is to reinvest capital generated from operations and take on debt when appropriate to acquire the highly fragmented market of smaller operators. For the boat dealers, they aim to do 4-6 deals a year and pay less than 4x EBITDA and to integrate and effectively double the EBITDA from the acquired dealer within 24 months of closing. For the higher margin parts and service businesses, they are targeting 2-4 deals a year going forward. These businesses demand a slightly higher premium and they target 5-7x EBITDA.

The company has historically paid out dividends, including a special dividend in 2021. Early in 2022, they announced a $50 million dollar share repurchase program. Whether they will actually use the program seems to depend on what acquisition opportunities remain. The management team when pressed implied they would treat the buyback opportunistically, noting that it would could offer similar shareholder value as using the cash on further acquisitions without any operational risk in integrating the acquired business.

Risks

Debt has risen as they have been aggressively acquiring businesses. It initially was a concern for me and still is something to consider. Looking at the balance sheet and the current sales on order with inventory and other short term assets considerably higher than short term debt, it doesn’t appear to be a material risk. With the highest volume quarter coming up in Q3 and the comments from management so far being that sales orders are as strong as ever, coupled with supply chain constraints not normalizing until 2023/24, financial ruin seems unlikely in the near term.

Share dilution is a concern with any serial acquirer that issues shares as part of the capital funding. Over the past 5 years, the number of shares has grown from 5-12 million. So far, this hasn’t been destructive to shareholder value as the businesses they acquire have made the business progressively better. As the price of the stock declines, the cost of capital may rise just as the returns on the acquisitions also take a dip in concert with the existing businesses declining at the end of a cycle. The efforts to bolster the revenues with the parts and maintenance businesses should be applauded.

Serial acquirers can run out of steam or go after larger deals in order to sustain growth rates. It seems likely that they will be tempted to do larger deals in the future and eventually this could curb returns on investments as larger acquisitions will be priced higher and will be more challenging and/or expensive to integrate. Given the relatively small size of the business, it appears that this is not an immediate concern and the highly fragmented nature and simple business models make this roll-up strategy as likely to be a success as any over the short to medium term.

If you want to know what a worse-case scenario might look like, you can look at the financial crisis period from 2007 peak sales to the bottom in 2010 for the larger Marine Max business. It took until 2019 to recover to the peak revenue again. Over a decade from peak to peak! I’m not suggesting this will definitely re-occur but it is something to consider. Counter to this risk is the fact that most normal recessions won’t impact boat sales as much as 2008 as boat buyers typically aren’t in the lower and lower-middle income brackets that have little margin to absorb an economic downturn. Further to set the context for a recession would be the 16% of steadier and higher margin maintenance and parts business with the acquisition of T-H Marine compared to 6% for Marine Max.

Valuation

On simple metrics like trailing and forward 12 month price to earnings, coupled with recent growth rates, it might seem like a screaming bargain.

You should factor in a few things when considering how valuable this business is:

cyclicality of boat sales

debt load

share dilution

If you have a view that consumer discretionary purchases remain strong for the next few years, then you are definitely getting a good deal here. If you are like me and are somewhat skeptical, you might be paying a moderate to high price at these levels. In the long run, there is a good chance that this business continues to grow despite a near term hit from a cycle downturn. This one is going to continue to be on my watchlist for now. What I would look for is a bigger percentage of revenues from parts and maintenance and less debt on the balance sheet to take advantage of a downturn when it does come.

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

That’s it for now, check back soon for more. As always, follow me on twitter and please share this with anyone who might interested in my work. My work is now completely free for all but there is an option for a low cost paid subscription as a way to support my work.

Thank you for the write-up, Simon. I think ONEW is a great company and am a shareholder myself.

A few additional considerations worth mentioning:

1. On industry growth in the short term: although waiting lists are still long for this year, I'm sure the covid peak is not sustainable, certainly with today's inflation/recession risk. ONEW's average selling price is almost twice the industry average, so that may shield them a bit. On the other hand, HZO's ASP is another factor of two higher, so ONEW is certainly not catering to the top segment. Nevertheless, valuation still looks attractive even with a revenue and margin reversion back to trend or temporary dip below.

2. On industry growth in the long term: the 'ageing boating customer' is a real risk. From 2000 to 2015, the typical boat owner got as much as 10 years older. If you look through the cycles, personal expenditures on pleasure boats have come down from 15-20 bps of total personal consumption in the 70s to 10-15 bps in the last decade. I see no reason for the covid peak to change this trend. Another risk (partly overlapping probably) is a mix shift from boat ownership to leasing/sharing. In my rough estimates this has only made a small dent in the ownership market thus far, certainly below 10% and probably below 5%, but it could continue to take share among Gen Y and Gen Z. Finally, you can ask how big of a risk a shift to online retail poses to ONEW. $200K+ boats will be one of the categories least at risk/last to shift online and ONEW is investing significantly in the online channel. Nevertheless, you should expect online competition, including direct sales, to grow. In the long term, all in all, I think it's fair to conservatively assume a flat nominal revenue outlook for ONEW.

3. On ONEW's organic growth: in the last 5 years they have outpaced HZO on organic growth and they outpaced the overall industry even more. I like to believe part of this is driven by ONEW's decentralized model. They keep the brands and the teams they acquire intact, provide them with back-office support + purchasing power + a large network for new & used boats + internal best practice sharing, allowing the local teams to double down on sales and customer service. In addition, ONEW helps acquired dealers provide high-margin financing & insurance options, which are often underleveraged by small dealers. This model seems to be strength and I'm expecting ONEW to continue outgrowing the market organically.

4. On value creation through M&A: let's consider only the dealer acquisitions, as they still need to learn the ropes in parts & maintenance. Being able to acquire dealers at <4x EBITDA, then doubling the EBITDA in 2 years and seeing this valued at a multiple that is closer to 8x is a great value driver. Please note the "<4x EBITDA" target was set pre-covid and I expect ONEW to not be paying 4x the covid peak EBITDA today. If you follow management's general targets and they acquire 2-4 dealers at $1.5-2M EBITDA each, that would mean paying ~$20M for ~$5M EBITDA. Turning that into ~$10M EBITDA worth ~$80M two years later would mean $60M or $4/share value creation on the dealers acquired just in one year. You can discount the numbers a bit, but ONEW has demonstrated its ability to successfully acquire and integrate and I think this capability is worth a small multiple of that $4/share. If you’re bullish you could even argue that this capability alone represents over half of today’s share price. There are more than enough acquisition targets, ONEW is often the preferred buyer and if the coming years get rough, that may allow ONEW to pick up some dealers at bargain prices.

Reflecting on #4, ONEW creates value through (a) sales of boats and related products & services and (b) cheap M&A followed by smooth integration. I believe ONEW does a great job at (a), with growing advantages from its scale, but currently not to the extent that you can speak of a moat vs. the hundreds of other dealers it competes with. On the other hand, ONEW has a unique proposition and excellent track record in (b) and I know of only one serial M&A competitor, HZO, which is playing a slightly different game in terms of target customer segment and branding/integration. As investor, I view boat retailing as the backdrop (that you need to be comfortable with) and serial M&A as the main value driver (and as much the core business as boat retailing).

I feel like the market already prepares for the worst. And that means a worldwide crisis, so this could end up in a situation like you explained (2007 - 2009). Therefore I believe that the risk-reward is on the high end.

Secondly, The management is very experienced and they have a lot of skin in the game. Which gives me confidence for good long-term returns.