OTC Markets $OTCM

Routing for the little guy

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

Disclosure: I own a small number of shares of OTCM.

OTC Markets is a micro cap ($ 646 million), thinly traded stock (average daily volume of 3.9k shares). It has a long history but a relatively modern transformation with the new CEO essentially re-founding the company. It has a significant advantage in its operations due to its moat around its brand and size relative to its market it serves (essentially a monopoly). It has high insider ownership and is run by capable management. It has had a good history of margin expansion as it grows not only the volume but quality of its business.

Underpinning the value of OTCM is the trust it has with its customers and regulators. It provides an efficient, reliable, and transparent ecosystem for all stakeholders to operate within. If it is able to maintain this brand trust and grow it’s business over time, it will be a bigger and better business. The insights into its core mission and the competitive advantage it can build over time can be teased out by the following quote:

I appreciate the opportunity to testify before the subcommittee today on the topic of “reducing barriers to capital formation.” As an operator of public marketplaces for small companies and a publicly traded small company in our own right, I hope I can provide the committee with greater insight into barriers to capital formation that should be removed. Our self-interest in changes to regulation is very clear. We want more openness so our public markets are more inclusive, we want better transparency so our public markets are better informed, and we want more connectivity so our public markets are more efficient. Finally, we want to remove unneeded regulatory burdens in order to reduce the cost and complexity imposed on smaller public companies.

CEO Cromwell Coulson - Hearing before the subcommittee on capital markets and government sponsored enterprises committee on financial services “reducing barriers to capital formation” June 12, 2013

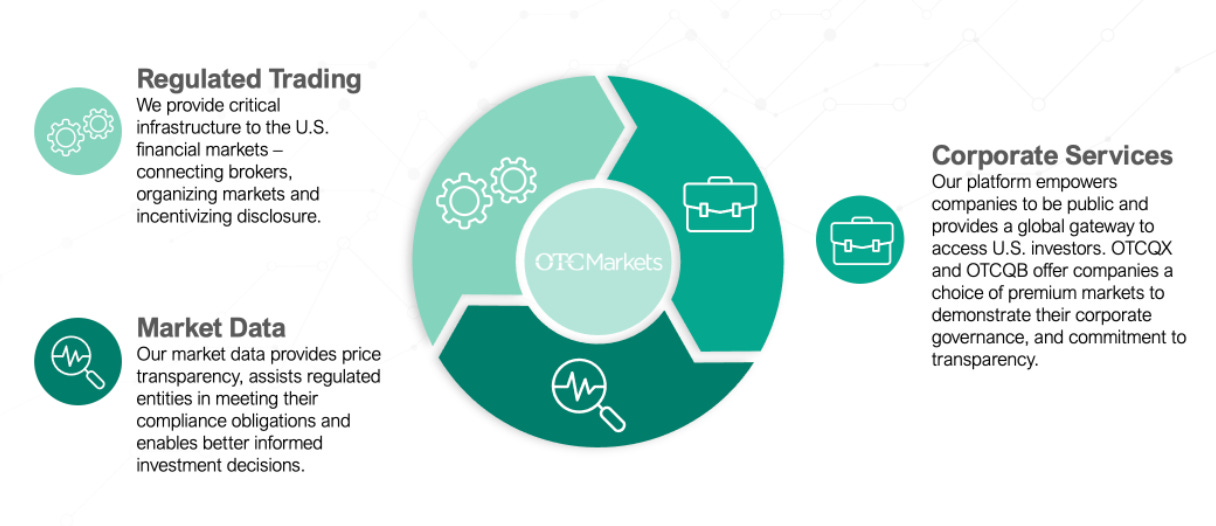

What They Do

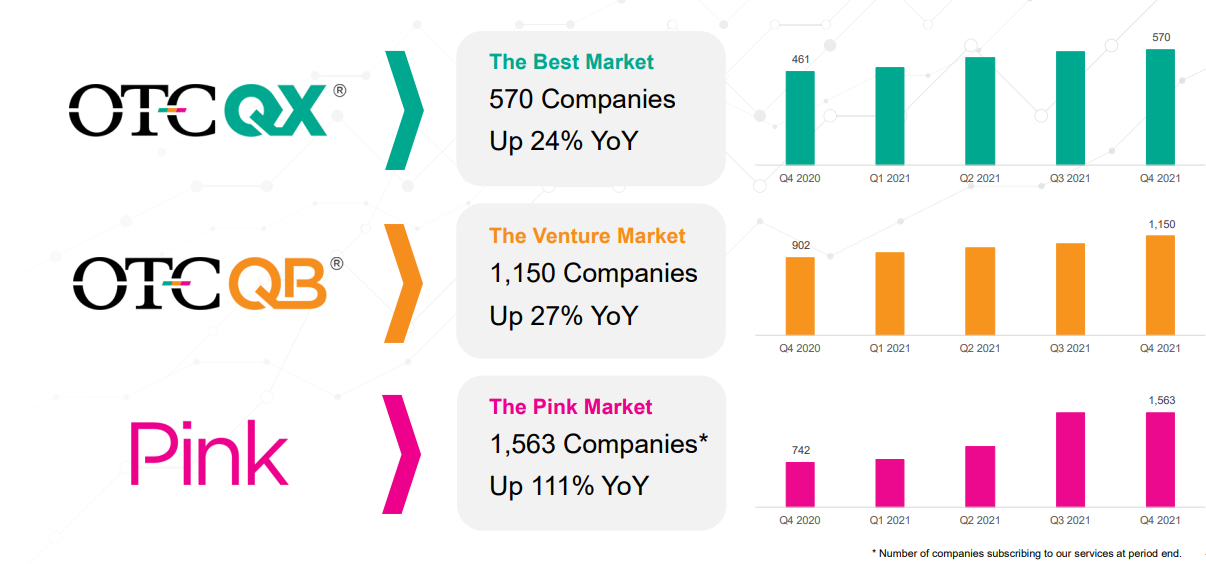

Corporate Services - the platforms that offer the listings of securities, including OTCQX “Best Market”, OTCQB “Venture Market” and Pink listed companies. These are ordered in terms of liquidity, transparency, requirements of filings, and cost to list (in descending order). There are one time listing fees and recurring annual fees for all platforms that are paid by the listing companies to register the market listing. The listings generate more value in the trading and attract new customers to the listings as the number of listings grows.

Regulated Trading (OTC Link) - the trading infrastructure that allows broker/dealers to display prices for bids/asks and execute trades. OTCM has two versions, the OTC Link ATS (alternative trading system) and the OTC Link ECN (electronic communication network). The ECN is the more modern technology closer in resemblance to the bigger exchanges and operates automatically. The ATS is older and allows broker/dealers to utilize some of their own infrastructure to execute the trading while taking advantage of the messaging system. ATS has a fee for connection to their network and a small fee for posting quotes while ECN has a fixed fee for each transaction. The trading grows or falls with the volume of trades (somewhat cyclical). It also generates the valuable data which is the next segment.

Market Data - the trading produces an opportunity to capture data which is then sold to market data redistributors and other clients on a recurring subscription basis. The more data there is, the more valuable the product. This a very sticky and high margin business.

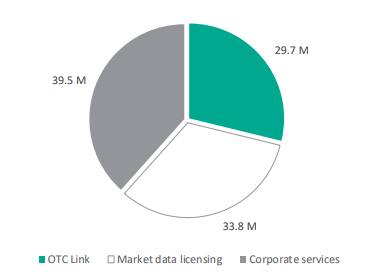

All three segments grow in tandem and some drive the growth in the others. The revenue split is fairly even amongst the three segments.

Business Quality

The Moat: Network and Flywheel

The value of the listings business grows as the number of listings grows when it becomes more entrenched as a trustworthy place for small businesses to list publicly. This then drives more trades which enhances the value of the data. Due to current regulations, competition from the larger exchanges such as NASDAQ and NYSE cannot easily compete.

Because there is a harmonious growth engine with very little capital required to grow, the best analogy is that of a flywheel. It would take a lot for someone to come along and compete toe-to-toe with an incumbent like OTCM given it dominates this market. Look to the number of listings, the trading volume, and pricing growth as an indicator of the health of this moat.

The SEC/FINRA regulates much of OTCM’s business and over the recent past has given up some control to OTCM. An example of this is the designation of ATS Link as a IDQS subsequent to introduction of rule 2-11. This means that new entrants would be very challenged given that high barrier to entry.

Recurring Revenues

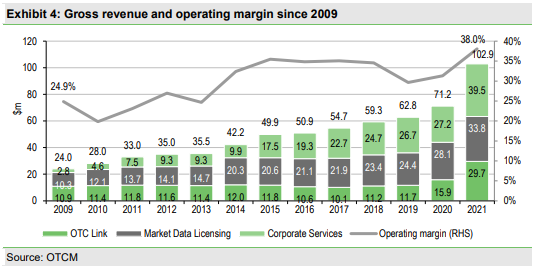

Most of their business segments have some forms of recurring revenue streams. The listings, data and the ATS Link customers have a recurring stream of revenue with some pricing power given the stickiness of the products. This does wonders for the consistent improvement to margins as overall sales increases in each segment.

Free Growth

The business requires next to no capital in order to grow. This is coupled with the fact that it has limited opportunities to reinvest its cash flows for growth. It will achieve growth with price increases as the value of its network grows with listings, trading volumes, and data sales growth (which have some positive feedbacks from each other).

Their investments in the technology made years ago was basically all they needed in order to get more and more returns as their network grows. As can be demonstrated with the ever increasing operating and free cash flow margins, the business scales very well.

Predictable High Margins + Improvements

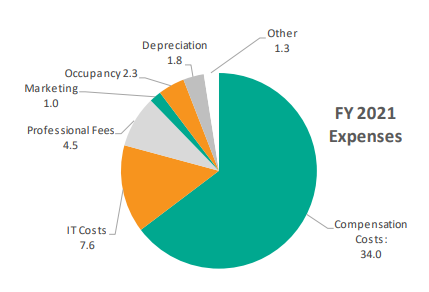

Over the past decade, as the number of listings expand, so does the value of the data that it provides. As it is a asset light and initially high fixed cost business model, the incremental revenues (even when not extremely high) have been extremely beneficial to the bottom line (the magic of operating leverage). A large portion of their costs is compensation.

While there are some cycles to be expected with the nature of equity markets and trading volumes, to date, the business has been fairly predictable and steady. Over time, as the business has grown, operating margins have slowly increased with it. This should continue over time as costs remain relatively fixed compared to sales.

Management Quality

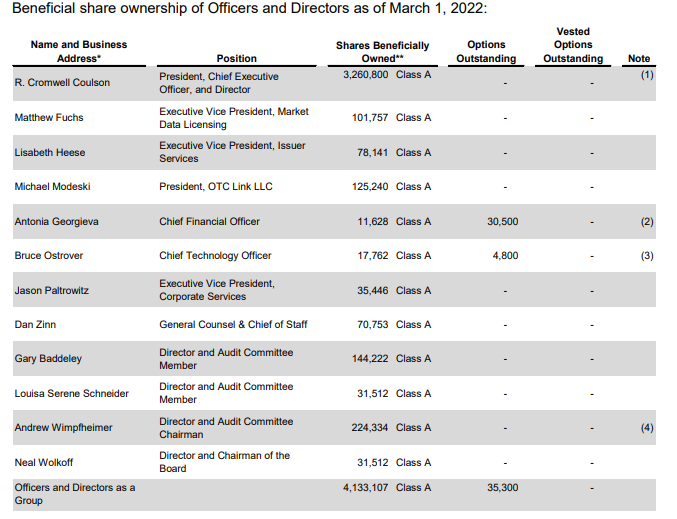

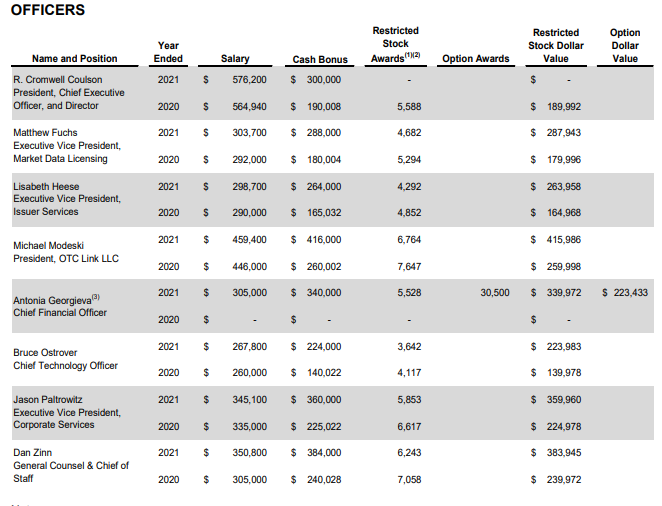

Insider Ownership

Insiders own 47%, including the CEO Coulson who owns about 28% of the voting interest. The stock awarded as part of the compensation is not egregious but is something to understand as the it contributes to a slowly growing share count over time.

Capital Allocation

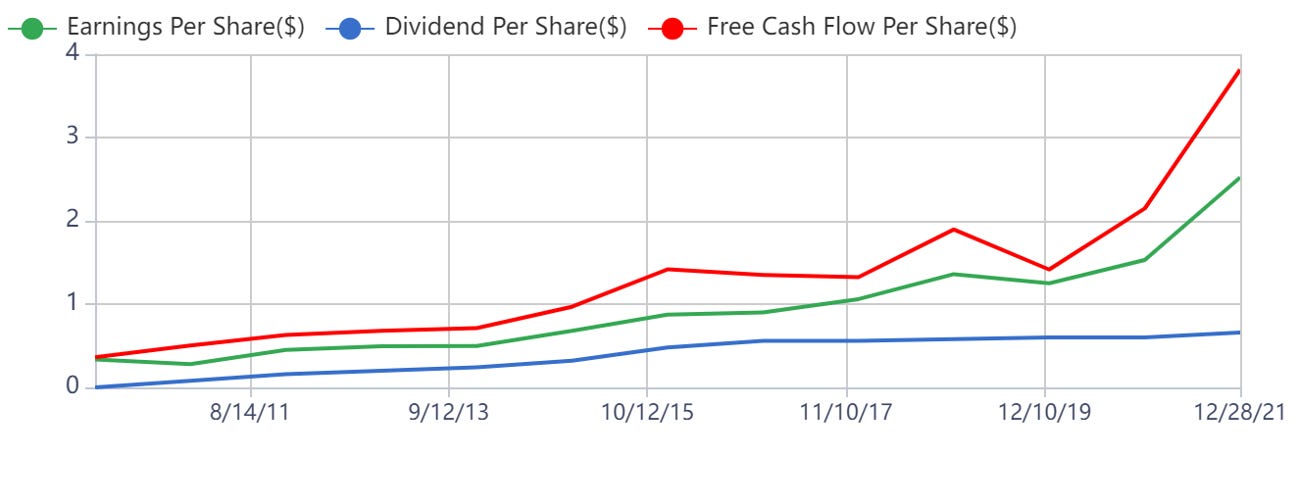

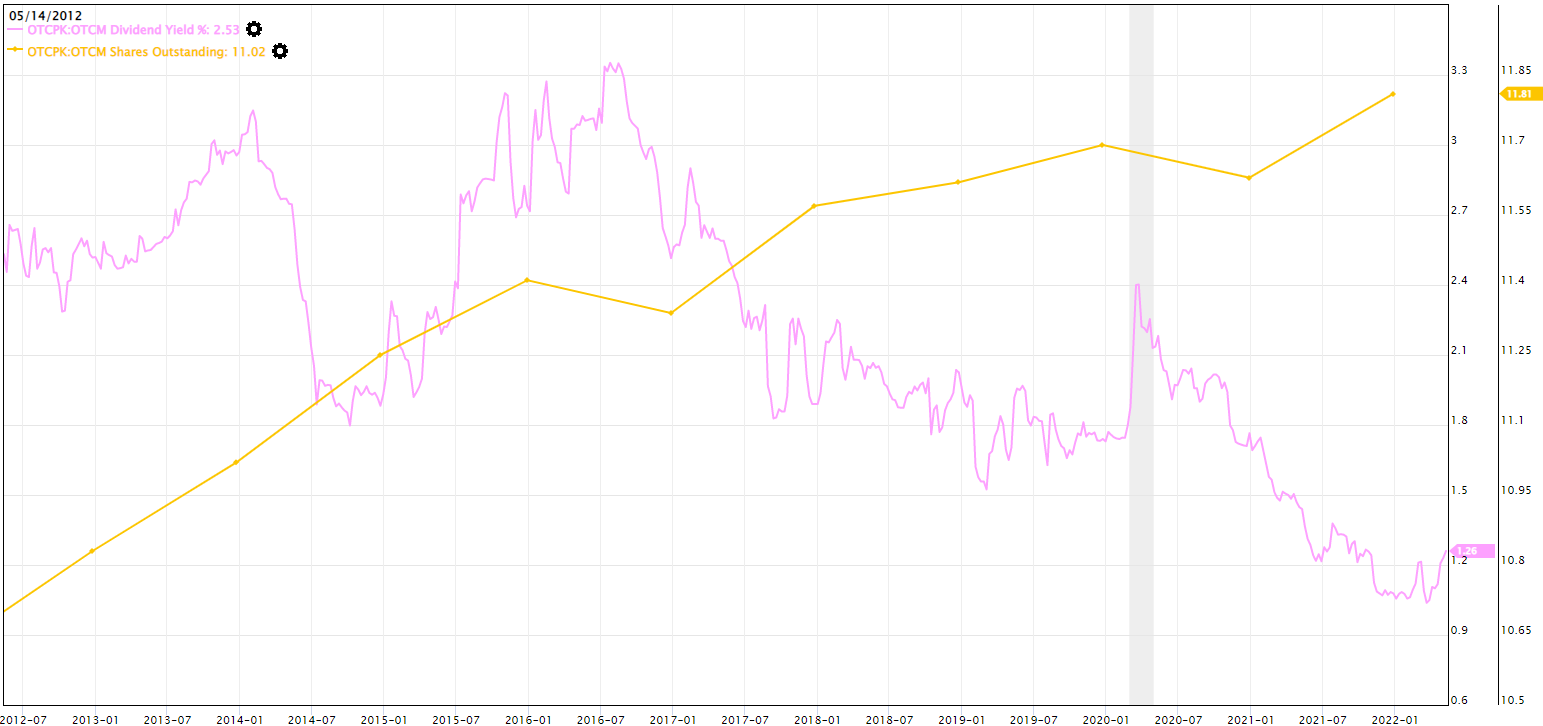

Dividend yield is currently around 1.3% and buybacks have not offset stock offerings as share count has slowly risen over the past number of years. Of note, they have also issued significant special dividends as cash builds up on the balance sheet.

It’s safe to expect the dividend to grow over time. Over the past decade it has grown 15% per year on average, although at a lower clip over the recent past. They did spend on significant capital improvements and expansion in 2019 which decreased their ability to grow the dividend temporarily.

Fundamental Risks

Trading volumes

If trading securities goes out of fashion, there will be a corresponding drop in the value of the trading data and revenues from all of its business to some extent.

In a hot stock market, they may acquire more listings but they will also lose small listings to bigger exchanges so the cycle impact may not be as big as initially feared.

Number of Listings

In a market or economic downturn, it is likely that either new listings on its three markets or existing listings will drop off. In recent years these listings have expanded quite a lot but there is likely to be slowdowns relative to these high growth numbers.

Regulatory Risks and Competition

For the most part, regulation has only helped OTCM stave off competition as the incumbent is entrenched in the system already. New regulations would only make it tougher for new entrants. Given the markets have limited growth, it seems reasonable that there is a limit to how much regulations are beneficial to OTCM versus potentially being harmful in terms of extra costs eroding margin profile.

Recent examples of regulatory impact on the business as described directly from the 2021 annual report:

SEC Rule 15c2-11

FINRA Rule 6432

Blue Sky Exemptions For OTCQX/B

Valuation

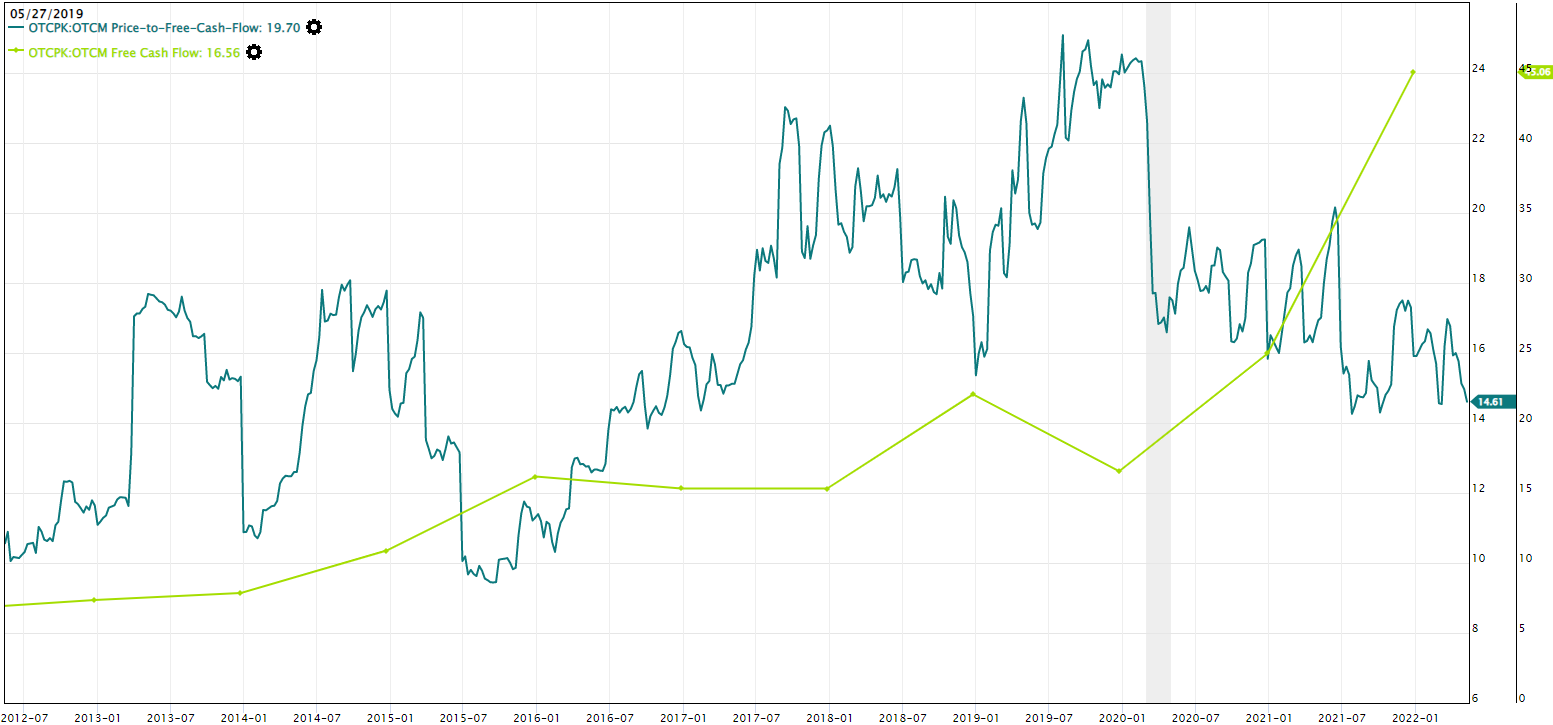

Taking a look at the valuation with a focus on the free cash flow yield and consideration to the future growth and any dilution that you might reasonably expect would be one approach in determining whether or not you are getting a good deal.

The business is not one that is going to be 100% predictable in terms of future growth but a conservative estimate based on past performance should suffice.

The business currently trades around a 5-6% fcf yield has had a 15% growth rate per share over the past decade (conservatively say it is something like half this going forward). If you consider 1% dilution per year, you might expect something like a 10% return per year going forward. Current price seems reasonable but may not make you rich quickly.

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

That’s it for now, check back soon for more. As always, follow me on twitter and please share this with anyone who might interested in my work. My work is now completely free for all but there is an option for a low cost paid subscription as a way to support my work.