Patrick Industries $PATK

A manufacturing conglomerate that had an amazing decade and interesting future prospects

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

Disclosure: I own stock in the company described below in my personal account. None of this is advice in any way and be aware that I’m likely biased due to nature of owning it.

| Seeking Alpha")

Patrick Industries, Inc. trades on the Nasdaq under the symbol PATK 0.00%↑. It has a market cap of around 2 billion USD and an enterprise value of around 3.2 billion USD. It was founded in 1959 (whoa!) and is headquartered in Elkhart, Indiana where it was founded and started out as a distributor to the area’s panel supply for residential building. With that, enjoy the rest of the show!

What do they do?

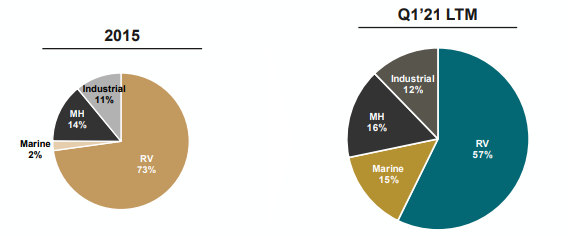

The business has grown to be a wide variety of both manufacturer and distributor of components that are supplied to OEM (original equipment manufacturer) in four major segments:

RV’s

Marine Vehicles

Manufactured Housing

Industrial

They have established relationships with OEMs. They make parts and help with distribution for all the big names in these industries. In the recent past, they have grown organically fairly well and also have made a series of acquisitions in all segments which have bolstered their diversity and strengthened their relationships with their end customers (mainly OEMs).

Do they make money?

Yes.

The company has been producing free cash flows every year since 2009 after the GFC had a significant impact on the business. Similarly, 2020 did impact the business but over the last 12 months, it has rebounded reasonably well to 2019 levels and increases are expected to continue.

Gross margins are very steadily in the 15-20% range and are fairly consistent. Revenue has been increasing at a very impressive 29% over the past 10 years and similar rates over the past 5. The ROIC has been 15-20% over the past decade and I would think that the lower end of this range would be achievable over the next few years as organic growth continues at reasonable rates over inflation and acquisitions contribute to cash flow as well.

The returns on equity have been around 30% (lower in downturns) due to diligent use of financial leverage and their returns on assets have been 6-10% fairly consistently which is a good sign that the business is predictably adding value for its customers while it grows.

Are there reinvestment opportunities?

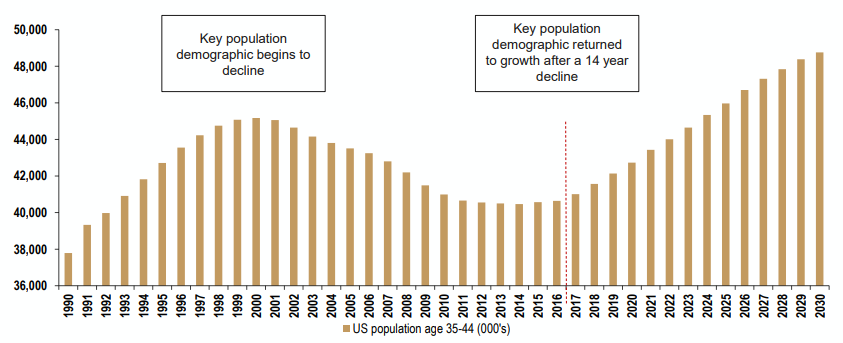

It does appear that organic growth COULD continue at reasonable rates into the next decade based on demographics and trends for the end products. This is a good tailwind for the business but it certainly comes with some caveats. The broader economy must continue to do well to support people buying these types of products (especially the marine and RV segments which are more discretionary spending). Inflation for its raw materials must stay reasonably priced (it will have limited pricing power in a lot of cases).

The other opportunity for reinvestment will be acquiring bolt on manufacturing and distribution businesses that will expand the stake of the end market and make Patrick an appealing partner for OEMs and other customers. The number of acquisitions that the company has undertaken in recent years is a good thing, in my belief, as it gives the management team opportunity to learn a lot when pursuing future acquisitions. The ability to do deals at reasonable valuations that will be beneficial to PATK shareholders is what needs to be monitored. So far, it appears that they are doing okay at this but it is often tempting to chase larger and larger acquisitions at more expensive pricing. For context, the company deployed over 300 million USD in acquisitions in 2020, and 700 million USD over the last 3 years. For a 2 billion dollar market cap business, this is fairly significant.

Is there a risk of a blow up?

The amount of debt is a bit of a concern for me. I’d like to see them pay down the debt to more reasonable levels so that they can lever up again when there are more opportunistic targets to acquire. Over the long term, I don’t think the level of debt they currently have will bankrupt them as cash flows are good but this could change quickly in a downturn.

There Altman-z score is a healthy 3.2 (no short term bankruptcy risk) and their interest coverage is above 6 which is acceptable for now. I would prefer that they hold more cash and I suspect the amount of acquisitions in recent past has lead to this.

In general, this is likely the most significant risk to the business that needs to be monitored. I would prefer if they focused on reducing debt from here going forward while the times are good. Organic growth should allow this deleveraging over the next few years.

Another operational risk that the company is open about is the reliance on the RV segment which makes up over 50% of sales and also a somewhat concentrated relationship with two of the larger RV OEMs that account for around 10% of sales (Thor and Forest River).

Is management sketchy?

The management team has historically diluted shareholders at times as shares outstanding increased significantly in 2006-2009 then again slightly in 2017. Since then, they have (wisely, I think) bought back shares. Recently, they have committed to buying back shares this year and the next (up to 50 million dollars). While not some insane amount, this is a good sign that there should be no further dilution in the near term.

There has been a small regular dividend over the past couple of years and I would prefer to see them focus on debt repayment and further acquisitions when they are available. I would even be okay with them storing more cash as opposed to dividend payments. That being said, this is likely not a terrible sign for the stability of the business. The payout ratio is quite small (between 10-20% operating cash flows) so it should not significantly hinder the growth in the future.

Does it have a moat?

No. I don’t think so.

Some could argue the business has a moat in its current relationships with the OEMs and its network of distribution and manufacturing capacity. Although, true that this does provide benefit to the business over the short to mid term, over the long term, there is very little the company can do to defend against competition. The advantage it could enjoy for a long time is that the business is somewhat boring and unsexy. Large investments for newcomers and competitors are less likely compared to a lot of other industries.

The disadvantage that a business like this has is that is has no real connection to the end user that the OEMs have and cannot enjoy some of the pricing power that the OEM (especially a strong quality brand) can have. In a lot of ways, the products that they manufacture are a commodity. The only real leverage they have with their customers is their past history of producing quality and perhaps their range of products (one stop shop) compared to newcomers to the industry.

Given the long history and growth over the past few decades, it seems likely that their is some good management and/or culture at the business and they are possibly doing acquisitions and cost management rather well (otherwise they could have failed completely by now). This is a strong potential moat but is difficult to measure directly without intimate knowledge (that I don’t have).

Is it cheap?

Yes. On most measures, the business is cheap compared the market and reasonably priced compared to its own history.

The P/E is currently around 11 (you read that right). This is cheap compared to big names in the S&P and certainly less expensive than the tech darlings. The EV/EBIT is around 11 and the P/S is around 0.6 (about average for its history).

If the business continues on the same or similar trajectory of growth, it is not unreasonable to expect similar returns over a long holding period (say 10 years) that it has enjoyed over the past decade (around 50X since 2011) With this one, there is exposure to the broader economic health in the US so I wouldn’t consider this a super resilient fortress business that will not be impacted by a downturn. There is some leverage and it is going to be correlated to the economy so be sure to monitor these risks to the underlying fundamentals and one must be comfortable to be a long term holder as there is likely to be some volatility in both directions.

Final thoughts:

Patrick Industries has good signs of becoming a very good serial acquirer/conglomerate. We will see if they can continue building out a robust national network of products/distribution to the big names in the segments that they serve.

They have an opportunity to produce good returns for shareholders if they monitor their debt appropriately and ensure that the cyclical nature of their business doesn’t destroy long term shareholder value. Given that the company is still relatively small and growing, there is a good chance for excellent returns over the next decade with a nice predictable, boring business.

If you liked this post, please ensure to share it with others and subscribe to get these directly in your email! I’m also on twitter @MoS_Investing.