Pinetree Capital Valuation

Even Pinetrees don't grow to the sky

I wrote about Pinetree Capital since the stock was around 4$ CAD and was trading objectively below book value. My thoughts on the quality of the business has not changed to any real degree since that post. You can catch up on the background by reading it. In this post, you will find my current outlook on the business, an updated detailed review of their holdings, and finally a valuation and forward returns assessment for investors.

The Capital Doesn’t Fall Far From the Pinetree

**Disclosure**: The author of this post personally owns shares in Pinetree Capital.

Recent Investor Sentiment

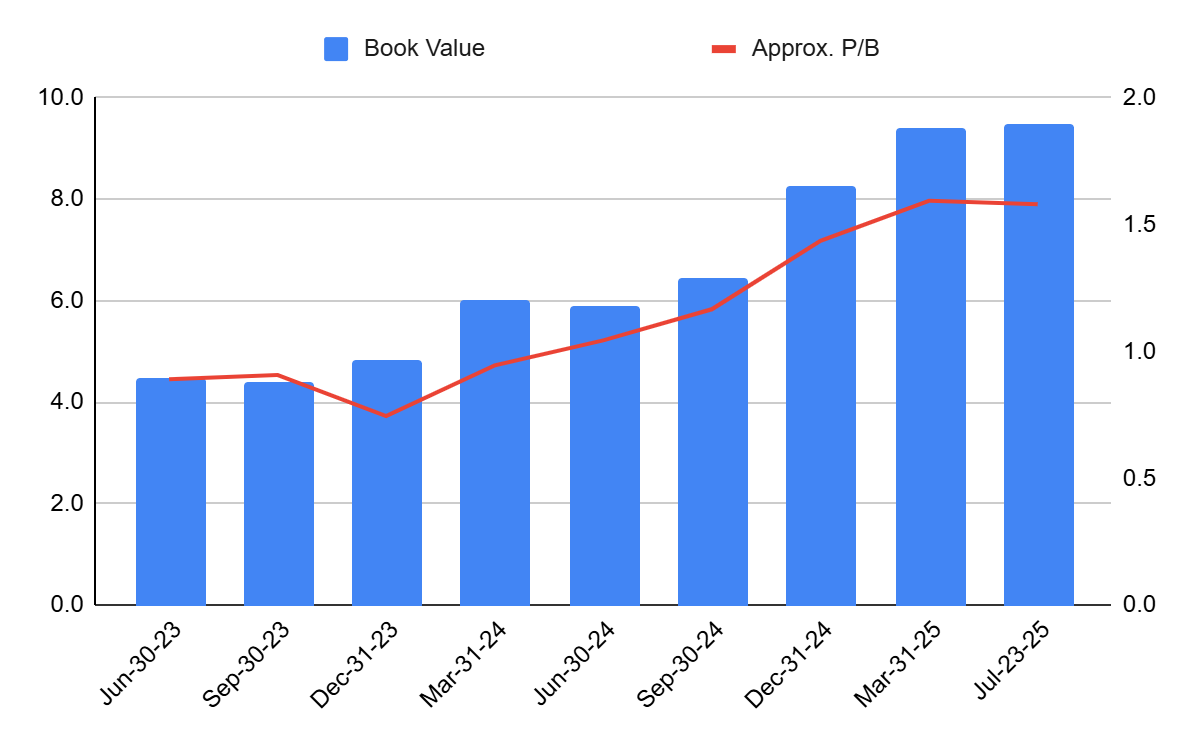

The stock has recently gotten a bit ahead of itself, reaching mid-twenties price levels. These levels represent something around 2X book value. Even for something that has the advantage of tax-loss carry forwards to take advantage of, allowing relatively frictionless capital recycling, this is likely pushing the bounds of what makes any real sense to pay for a holding company the likes of Pinetree.

Above 20$, L6 Holdings (the Leonard family vehicle that is partnering with Pinetree on friendly activist investments such as their stake in Bravura) has been net sellers of Pinetree stock (small amounts). This seems like they are opportunistically taking advantage of any euphoria in the stock in which the price is far above their hurdle rates and there is liquidity available. I would keep an eye on this going forward for signs of the stock price getting ahead of itself again. The caveat here is that they also did this when the stock price was just above 10$ or so and in hindsight that was a likely a bit premature.

If we take a look, you can see the rise in valuation premium as the company has executed very well with somewhere around 50% growth in book value per year starting in 2023. The other aspect here is the relative awareness of investors. Still today, Pinetree is too illiquid for most investors with any significant amount of capital to deploy.

Holdings

Pinetree holds both public and private investments, with the majority being in the public equities side (small VMS businesses they have an edge on and can help