Pool Corporation $POOL

A shallow dive into a strong compounder

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

Disclosure: I own a small number of shares of POOL.

Pool Corp is a $17 billion market cap with an enterprise value around $18 billion. The stock trades on the Nasdaq with the symbol POOL 0.00%↑. The business has been a compounding machine generating average annual compound returns of 29% per year since their IPO in 1995 and demonstrates strong ability to sustain for a long time to come.

Let’s dig into the business, the management, the risks, and the current valuation…

What They Do

Pool Corp is a large distributor in everything related to outdoor lifestyle products (you guessed it… pools!). They operate in North America, Europe and Australian markets. They also offer related products such as irrigation, outdoor lighting, hardscaping, landscaping, and related products.

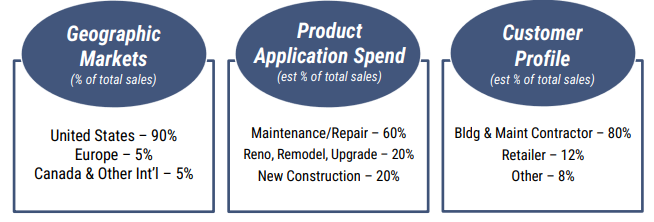

90% of sales are from the US, with the remaining markets being in Canada, Australia and Europe. What’s even more interesting is the sales breakdown by type. The new construction only makes up 20% of the spend while 60% is in the maintenance/repair category which is very much a sticky and recurring source. The customer being heavily focused on the contractor end is also a good thing as they will be slightly less price conscious.

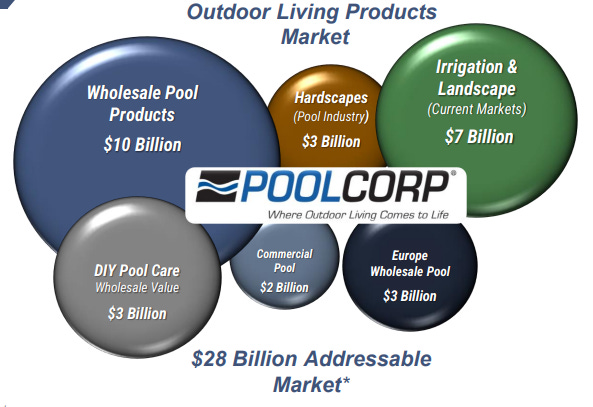

Their product offerings and channels to sell are wide and varied. They have a large runway to grow into a very fragmented market. Pool Corp. claims to be tackling a $28 billion dollar total addressable market.

Business Quality

With a growing distribution network and more scale advantages with their suppliers, Pool has been able to slowly and surely benefit from operating leverage over the years and there are no signs of this reversing in the near term.

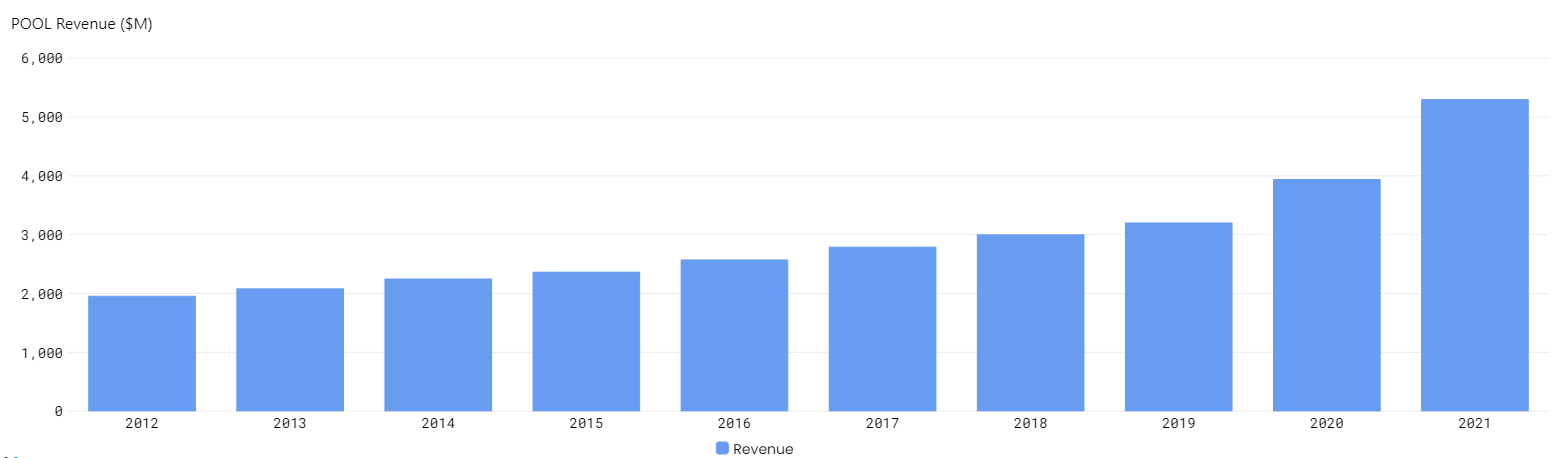

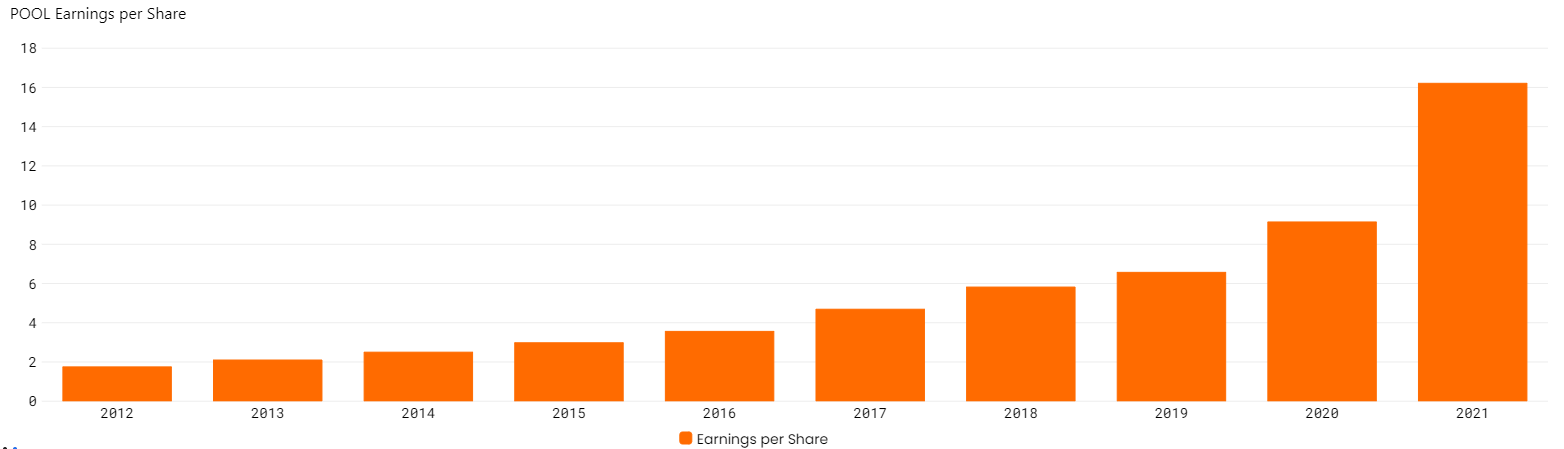

Revenues have increased every year over the past decade at an average rate of 10%+.

The growth has been fairly consistent and the demand during the work from home and southern migration in the US coupled with housing equity rising has meant some pull forward in the last two years. Looking ahead, inflation and new sales are projected to combine close to 20% growth for 2022 (with inflation making up half of that). In the longer term, growth is expected a bit lower, closer to the 6-9% range (still not shabby).

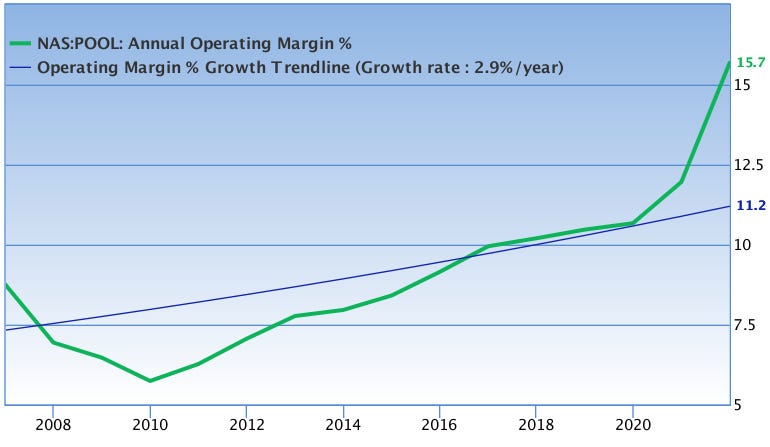

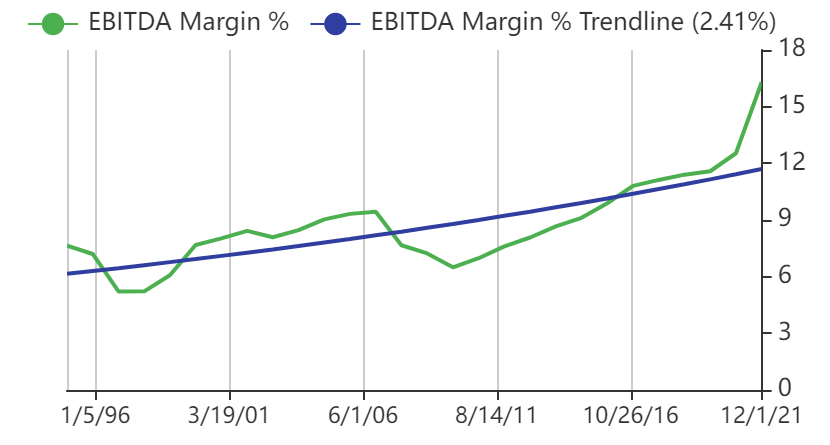

The operating margin expansion paints a picture of how well the business has scaled. They have been able to benefit from their growth from acquisitions, organic investment, and better cost management with suppliers coupled with improvements to their distribution network. This has resulted in faster EPS growth. This is the magic of operating leverage at work.

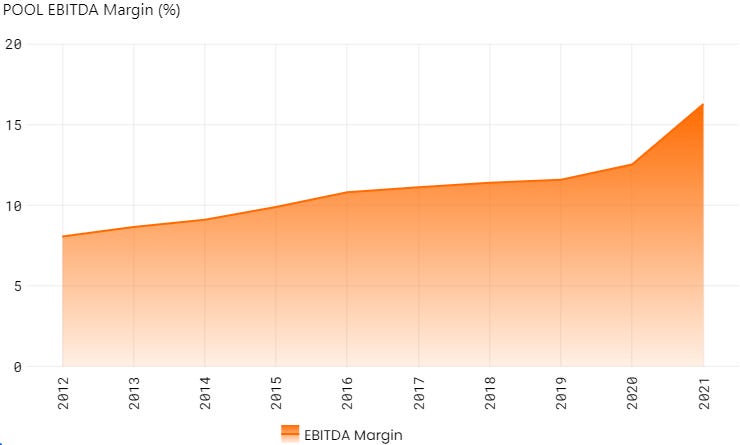

Another place to see the increasing quality of their operations is in the EBITDA margin expansion. EBITDA margins have basically doubled over the past 10 years. That being said, this is not a high margin business overall. It is one that can turn over assets fairly quickly however so as long as there is a growing install base of pools to maintain and reno over time, they will continue to generate good returns.

Management Quality

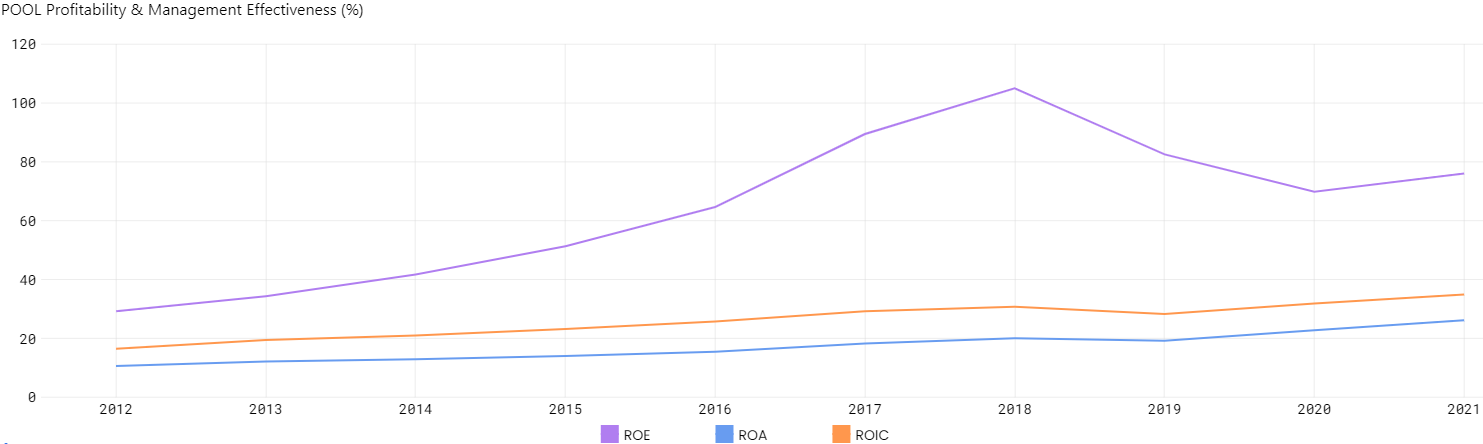

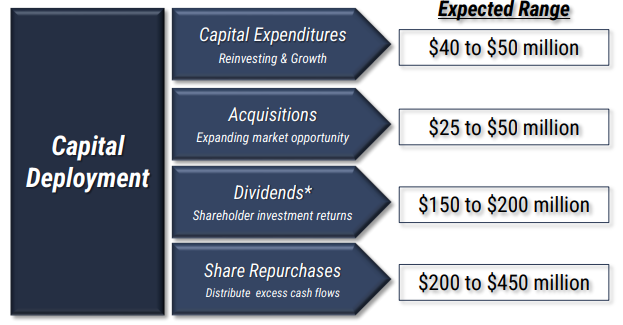

Management has done a great job at allocating capital. They have been able to consistently increase dividends, buyback shares, reduce debt, and do well with acquisitions.

But don’t just take my word for it; the proof is in the pudding. The return numbers have been good and increasing over the past decade.

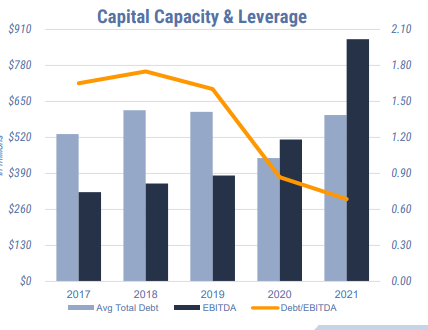

Management has worked at reducing cyclical business impacts by building and prudently maintaining a strong balance sheet recently. Debt has remained low while EBITDA has grown. They have been conservative in not levering up excessively despite plenty of growth via acquisitions to chase in a fragmented business. The management team has been focused on maintaining acquisitions which are beneficial to long term investors.

The management team speaks in easy to understand language and is reasonable in their approach to capital allocation. They are clear in their plans for the future direction of the business and where capital allocation is intended to be used.

The math works out to capex of 65-100 million and total shareholder yield of 350-650 million (about 2-4% yield at current price of around $415/share). Not bad given that this will almost certainly continue to grow over the long term. More on valuation later.

Downside Risks

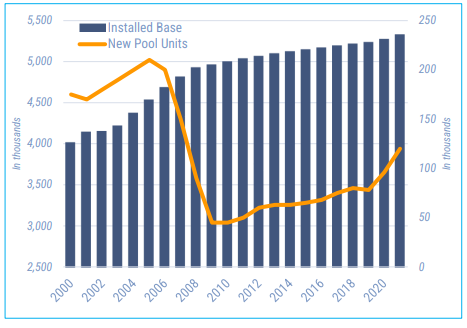

The pool business will be loosely tied to the housing market. If there is a housing downturn, there will likely also be a dampening of the sales from Pool Corp. That being said, unless there is another 2008 scenario, it is unlikely to be a death-blow of any kind for the business. The new installs will go down to very low numbers in a downturn and the renos will decrease as well but the maintenance will continue to be there and will be profitable.

As you can see, in 2008, new pool installs fell off a cliff. Most housing downturns won’t be that aggressive but that’s not to say that the business and the valuation won’t take a pretty big hit in any similar downturn. We are currently not even fully recovered from the prior peak for new pool units and there was management commentary on the 2021 earnings report that the backlog is strong for 2022 while projecting much further than that is difficult.

Growth Prospects

2022 and Beyond

It’s important to consider what the future growth in the business might look like and where it is likely to come from.

Outdoor living remains a priority with homeowners across North America, which continues to keep demand for our products strong. New pool construction backlogs are solid and will keep builders busy for much of this year.

Families continue to invest in their backyards and enjoy the benefits of a healthy outdoor living lifestyle. Pent-up demand for renovation continues on the installed base of pools and hardscapes fueled by a tight housing market and rising home values. The maintenance and repair business is strong with the most maintenance companies commenting that the tight labor market isn’t allowing them to expand as fast as the market opportunities will allow.

Peter Arvan - Q1 2022 earnings call

For 2022 its projected to grow earnings per share to to $18.34 to $19.09. It sees inflation around 10% and it normally passes this through the channel so it should have minimal impact on its own. Beyond 2022, the company expects more normalized growth of high single digits for the topline in the long term. This should still translate to mid to high teens growth in the EPS numbers which over the long term (5-10 years lets say) can do wonders.

Regional Expansion - Europe

Europe is a very fragmented market and Pool Corp is currently the #2 distributor. Europe is a very small part of the revenue currently but could be a great place to buy up small distributors as they have a large chunk of the market currently. Making small acquisitions can be done more cheaply than buying larger firms.

Industry Modernization

I believe an undervalued aspect of the future state of the business is the modernization of the pool install base. People will see newer pools that will have nice automated features and cosmetic enhancements like LED lighting and will spend more and more to reno or upgrade their older pool to match. This will increase the maintenance spend over time as no one will tend to want to go backwards (hedonic treadmill, etc.). Social media prevalence will play a role in this change, in my opinion. It’s tough to put numbers on this but recent trends have shown strong growth as some categories have been doubling since 2019, according to the company presentation.

Aging Install Base Opportunity

According to the company, the average age of the install base is around 20 years old. This implies a few things. Either people will be upgrading and renovating their pools or choosing to rid themselves of it in the future. It is very expensive to remove pools, so often maintaining them is actually the frugal option. I believe this is actually the key to their long term durability. Pool installs will wax and wane with housing markets and trends but maintaining the pool you have is always a priority.

Valuation

Taking the low range estimate around $18 per share earnings applying the historical P/E of around 20-30 would put a “fair” price around $360-540 per share. I would suggest it’s possible that there is a slowdown that occurs sometime in the next few years and so if you bake that in to your expectations, it seems that the price you are paying today around 23X is reasonable. You are getting a 4% earnings yield, shareholder returns around 3%, with growth of EPS likely 15-20% a year over the medium term.

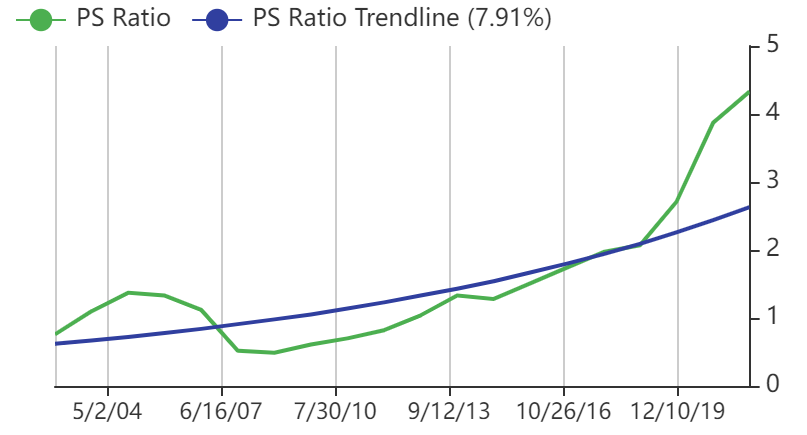

If you look at valuation on a price to sales metric, you can see that perhaps it is actually a somewhat elevated price. Currently it trades around 3.5X sales and the historic value has been between 1-2. The reason for this is clearly that margins have expanded. The real concern would be if margins were to mean revert with a downturn. In the prior 2008 downturn, margins did compress and while it’s fair to suggest the business has improved since then, it’s likely that this reversion in margins would recur in those downturn scenarios.

At the same time, there is still lots of good growth opportunities and if you can get on board with the management team (it seems like not a bad idea to me), then the current valuation seems like a good entry point. The past decade has enjoyed mostly tailwinds for the industry but there is not guarantee the next will be as smooth.

Given that the business does not have an impenetrable moat from competition, I believe the value you are getting here is a combination of a good boring compounding business and a potentially great management team; not the other way around.

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

That’s it for now, check back soon for more. As always, follow me on twitter and please share this with anyone who might interested in my work. My work is now completely free for all but there is an option for a low cost paid subscription as a way to support my work.

What are your thoughts on regulations due to droughts etc