Texas Instruments $TXN

A calculated compounding machine

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

“…growth of free cash flow per share is the primary driver of long-term value.”

Texas Instruments

Texas Instruments TXN 0.00%↑ is well known for their graphing calculators like the TI-83 plus model shown below. That is a tiny percentage of what the business does today but it is what most people know as its the consumer facing product. The business makes thousands of different analogue chips and embedded processors (semiconductors). The company has been around for decades (originally Geophysical Services Inc. in 1930 and changed to Texas Instruments in 1951) but have focused heavily in the semiconductor chips and processors business since 2011 when it bought National Semiconductor for $6.5 billion.

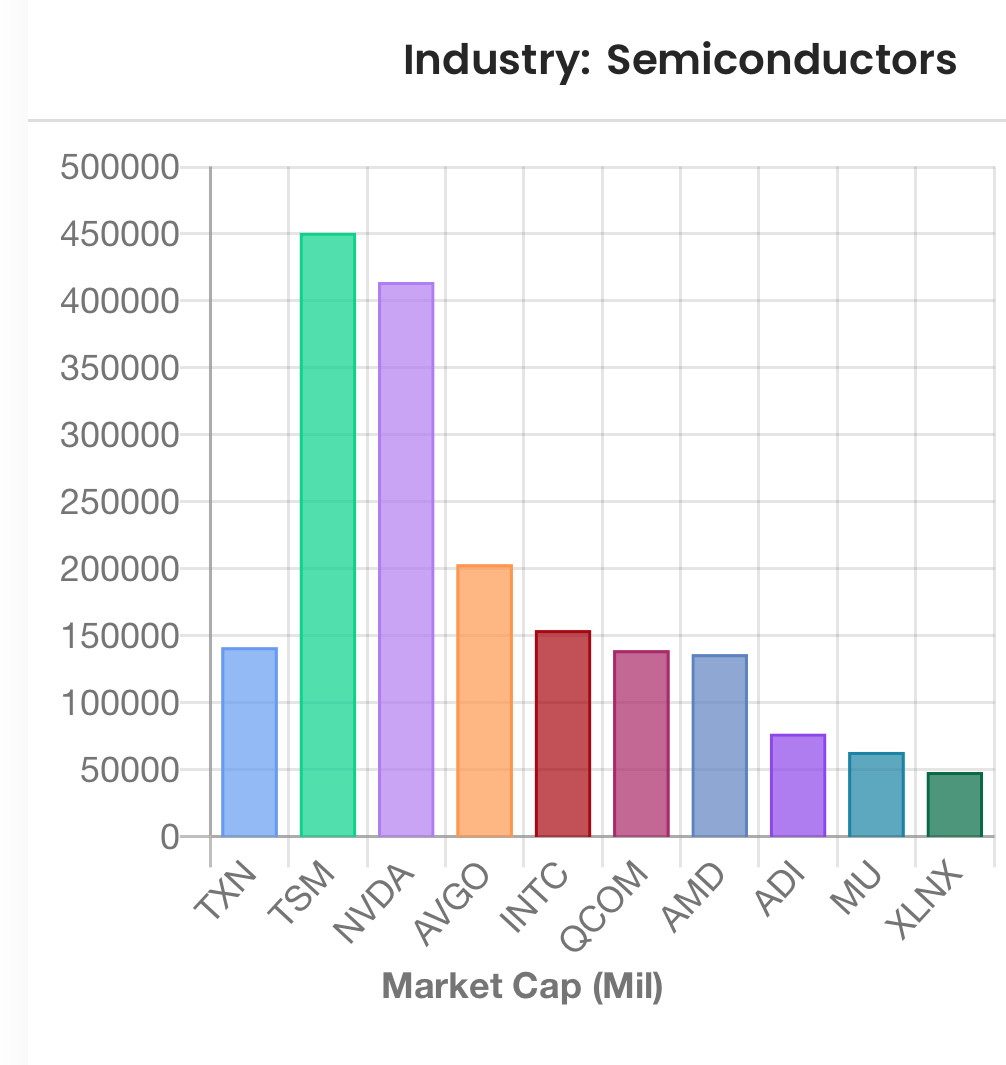

The stock trades on the NASDAQ under the symbol TXN. It has a market cap of $138 billion USD and an enterprise value of $136 billion. It is a well known business that has had a 10 year return of ~20% per year (including dividends).

Let’s take a deeper look at the business and management quality, growth prospects, investment and business risks, and a take on valuation.

What They Do

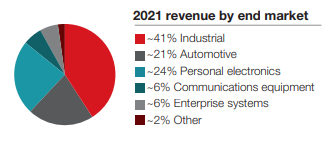

They design, manufacture, and sell analogue chips and embedded processors to multiple industries. The automotive, industrial, and personal electronics segments make up the majority. They have a relatively large number of distinct product offerings and many customers across the globe.

The majority of of their products are manufactured, tested and assembled in house which makes the business more integrated compared to a lot of the competitors.

Analogue chips handle things digital ones can’t (varying voltage levels, namely). They do power management, read voltages from sensory equipment and communication signals. They are normally cheaper and less high tech and change at a slower pace compared to their digital brethren. These are the boring old tech that some people think are dead. The truth is that there will be more and more need for analogue as the world moves to a connected, digital world with sensors and connections for everything, everywhere. Because the tech changes less quickly, building out analogue manufacturing is cheaper and longer lasting. The product catalogues don’t get stale quickly and the products stay in the end product for the lifecycle (i.e.. years for things like automotive and industrial systems).

Business Quality

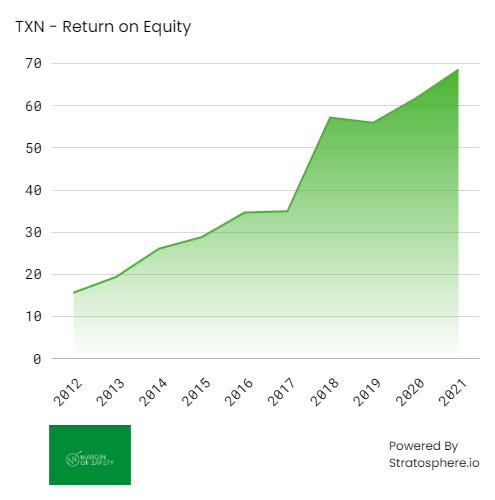

Gross margins have been increasing steadily towards 70% and returns on equity have been as well. There is no doubt that quantitatively, this is a high quality business. The balance sheet is strong with interest coverage at 55X and debt to equity at 0.6.

I will start with this return on equity chart and try to offer some insights as to why the business quality is what it is today and where it might be in the future.

Vast Product Offerings

When it comes to supply, Texas Instruments (TI) wallops a lot of the competition with the shear number of offerings. This can be an advantage when the product like an analogue chip is a tiny fraction of the overall product cost. Companies may prefer to stick with TI instead of sourcing different supply for applications when they have confidence that TI will have what they need.

They offer over 80,000 products in their catalogue to over 100,000 customers. This is mind-blowing. This is higher than their competition and will not be something that will be easily overtaken quickly.

Direct Sales, Long Customer Relationships

TI has direct sales, sales through distributors and other channels that can mean they have eyes into lots of separate demand channels. This can help with operational planning and future capital planning as well as sourcing new customers.

Vertical Integration

TI has more internal production than most of the competition. A lot of the competitors chose to do a lot of the manufacturing through outsourced contracts with manufacturers as a way to save on capital requirements. This means a higher margin for TI and better control of the costs for manufacturing. They may chose to invest in improvements to operations on the manufacturing side of things when their competition may not have aligned incentives for this with their manufacturing partners. The outsourced manufacturing companies may not always be interested in the investment in things like 300 mm plants if they don’t see a payback from these cost savings once the price can be passed on to their chip designers.

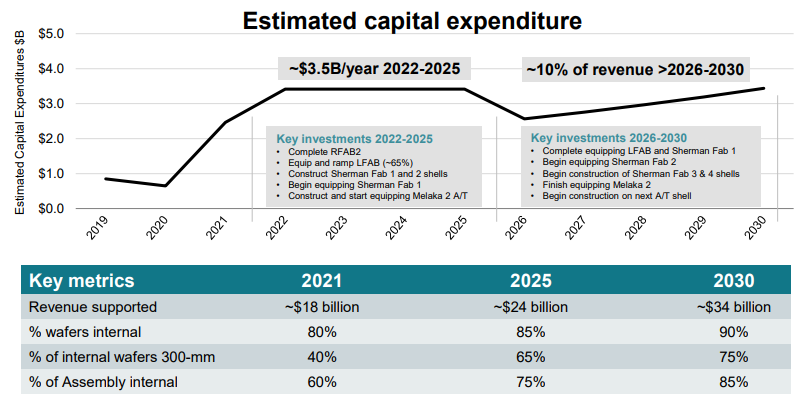

300 mm Wafer Advantage

Their production is shifting towards a focus on 300 mm wafer manufacturing. They plan to go from 40% of chips to 75% of those internally internally produced. This is distinct from much of the competition and offers a compelling cost advantage of 40% less due to the chip cost compared to 200 mm. Most competitors are not vertically integrated and their outsourced manufacturing may not be able or willing to invest the capital required to manufacture on 300 mm.

This shows up in high gross margins that have been expanding from 50-70% as they have increased their mix of inhouse fabrication and increasing their efforts to produce using 300 mm wafer. This margin should continue to increase further with the capital plans to increase internal 300 mm wafer based production.

Growth Prospects

Semiconductors are indeed in the middle of what should be a very long global secular tailwind for the entire industry. Being a large player and one that is setup to not be in the most competitive space with digital chips and processing is probably a good thing when it comes to threats from competitors.

The management team is planning for 7% revenue growth. This seems fairly in line with estimates from market analysis that seem to suggest similar or higher numbers for the next decade. There is an secular industry tailwind at their backs that should continue over the next while.

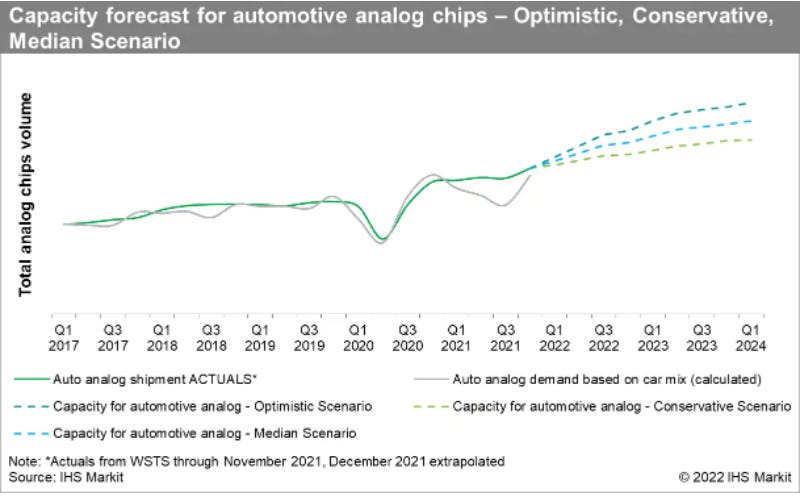

As an example, the auto segment for analogue chips expect about 10% growth over the next few years. The below chart is from IHS Markit.

There are a few takeaways from the auto segment that are crucial to the TI story going forward:

There will be continued strong demand for analogue chips going forward as the word gets more and more digital (bit of a paradox)

There has been underinvestment as a lot of capital chases the fast-moving, higher margin digital chips (more competitive in some ways)

This combination with the advantages that TI is building could be a great combination for shareholders if the end market and competition continues the way it has been

In comparison with 2021, the average number of analog chips per car is going to be much higher in 2023. The available extra capacity is insufficient to meet the fast increase of analog chips in cars, driven by ongoing trends such as electrification and a higher number of infotainment and advanced driver-assistance systems (ADAS) features.

The semiconductor chip capacity will grow, but hardly fast enough to meet the increased demand for analog chips in cars. After MCUs in 2021, analog chips are likely to become the main constraint for vehicle production in the next three years. The number of analog chips per car increases faster than MCUs irrespective of propulsion type, sales segment, and E/E architecture. These analog chips are also in high demand in many other industries such as the smartphone and consumer electronics industries.

There is a front-end capacity deficit for mature process nodes as most of the investment goes toward more advanced nodes. According to our analysis, out of the total capital expenditure announced in 2021 and 2022, 86% is directed at advanced technologies requiring just a few chips in the car, while only 12% is for the mature process, which is used to produce more than 90% of the chips in the car. With the increase in demand for analog chips, irrespective of the change in E/E architectures, this imbalance in announced capital expenditure could cause future bottlenecks for analog chips and other legacy nodes.

- IHS Markit “Analog chips – poised to become the next big threat to automakers?” by Jeremie Bouchaud

Management Quality

The CEO, Rich Templeton and CFO, Rafael Lazardi have been with TI since 1980 (CEO since 2004) and 2001 respectively. They have both moved up to the top from within the organization. I think this is a good thing in this case as they understand the business and have been with TI since its focus on its current core business. How many CEO’s have a laser focus like this quote? This is clearly a part of the core belief as their conference calls echo these type of statements over and over again. They are truly aligned with shareholders, in my opinion.

The best measure to judge a company’s performance over time is growth of free cash flow per share, and we believe that’s what drives long-term value for our owners.

Rich Templeton, CEO Texas Instruments

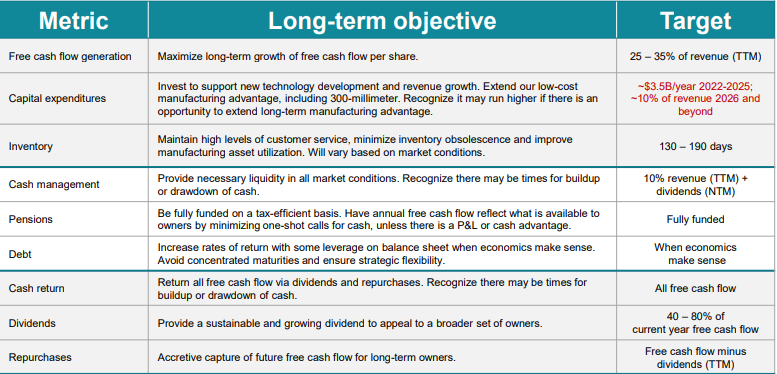

Capital Allocation

The management team has been quite clear about returning 100% of free cash to shareholders over time with share buybacks when they make sense and via an increasing dividend. 40-80% is earmarked for dividends and the remainder from free cash is directed to repurchases to support the long term holders.

Their capital spending plan is ramping up over the next few years. They plan to invest heavily in 300 mm fab with $3.5 billion a year from 2022-2025 and 10% of revenue thereafter. This is expected to drive revenue but also increase margins significantly as more of the products sold will be made in house and on 300 mm wafer.

Risks

Exposure to China

TI has 55% of its revenue exposure from China. If China follows through with a focus on tech independence, then it would not be un fathomable to imagine that their revenue from the region would decline considerably within a few years.

Reports put the Chinese investment into supply chain independence for semiconductors at 1.4 trillion USD over the next few years. I think it’s fair that the bulk of that is not going to go to making analogue tech for strategic reasons but the flip-side is that making their own analogue chips should be an easier mountain to climb.

Competition

There are competitors to TI, notably Analogue Devices ADI 0.00%↑. In comparison, ADI has lower margins, fewer products, issues shares and doesn’t seem on the surface to be as high quality of a business but that’s not to say that couldn’t change over time.

TI is the biggest in the semi industry in its segment. Bigger firms in semiconductors include capital intensive foundries and digital chip and processor producers.

Correlated to Macro Economies

The industry tailwinds could taper considerably given the nature of the products and the ties to the broader advances of the digitized world. I think TI could be affected even more than most if there were to be a slowdown that lasts longer than normal. This is because of the expansion plans for the internal wafer fab that will consume billions over the next decade. Fabless or semi-fabless competitors could scale back growth plans quickly in comparison.

Valuation

If you consider valuation based on what you will get back as a shareholder, it seems clear that you should try to estimate the free cash flow over a long period. Assume you will get that back, given that is what they have been doing. That is what they have stated their strategy is going to be going forward.

From today’s stock price of $150, you are getting a fcf yield of about 4.6%. I would expect that over a long period of time with the investments made to improve margins, buyback shares slowly and increase total revenue around their target of 7%, fcf should grow somewhere around 5-10% a year. This is dependent on how well their capital program works and the macro economy health. From 2004-2021, the per share growth in fcf has been 12%, so estimating it to be less than this number seems reasonable given the capital investment moving forward over the next few years. You could see many outcomes that offer a low-mid teen return numbers over long periods from today’s prices but it isn’t a certainty by any means (see risks).

Another indication that this could be a good or at least fair price is that the current price is around the 5 year low at a P/E of 17. Basically, you are paying a market multiple or slightly less for an above market average business run by a good management team with a sound strategy to return cash to shareholders.

If you are looking for a boring compounder at a fair price, you could be interested in Texas Instruments at these prices. It is certainly now on my watchlist.

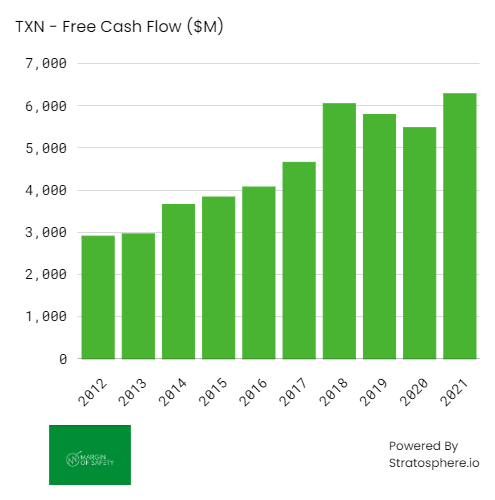

I’ll leave you with this one last chart of free cash flow and remind you that this isn’t adjusted for the share count reduction. Now think about the future, as that’s all that matters in any investment decision.

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

That’s it for now, check back soon for more. As always, follow me on twitter and please share this with anyone who might interested in my work. My work is now completely free for all but there is an option for a low cost paid subscription as a way to support my work.