WeCommerce Holdings Update $WE.V

Patience is bitter but its fruit is sweet

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

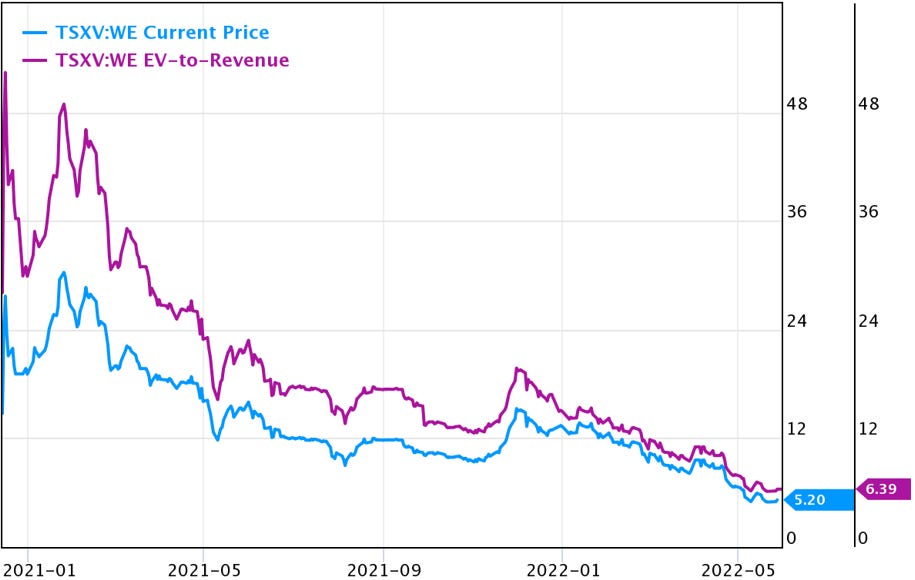

WeCommerce is down significantly in share price since my initial publication on the company. It has been correlated with the precipitous decline in e-commerce and high multiple and high growth software stocks, specifically Shopify SHOP 0.00%↑.

Perhaps this means that my initial purchases were an unforced error or I was overpaying for a speculative business or maybe I made an error in judging the underlying business quality. At this point, I’m leaning toward the possibility that I overpaid slightly. But if you look under the hood, the business underneath is doing quite well and still has a rosy future ahead.

Current Performance

During the Q1 2022 earnings call, the following takeaways on fundamentals were noteworthy in terms of where the business is today and where it is headed.

In general, tough comps and overall challenges with ecommerce compared to 2020-21 related to supply chain, competition, and other economic factors (inflation, etc.). It was noted that there is an ongoing concern with rising costs for merchants (advertising, supply related costs, increasing working capital requirements).

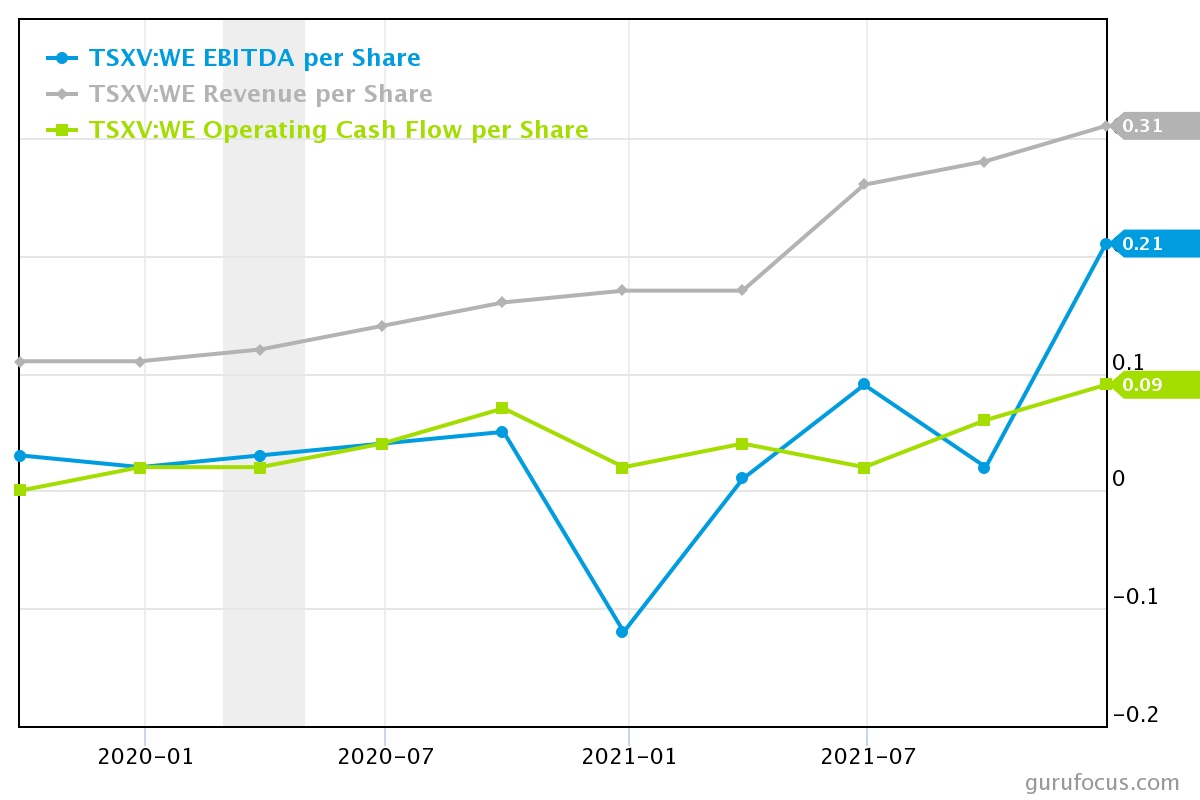

Topline revenue grew to $12.1 m for the quarter, up 100% from 2021. There were >30% operating cash flow margins (continued from Q4 2021), at $3.9 m up 200% from 2021.

Strong growth in the recurring revenue Apps business at $7.4 m from Apps (+222% YoY). 72% increase in Themes ($3.7 m) and a 37% decrease in the lower quality Agency business ($0.9 m). Adjusted EBITDA grew 42% to $2.8 m for the quarter and accounted for 23% of revenues.

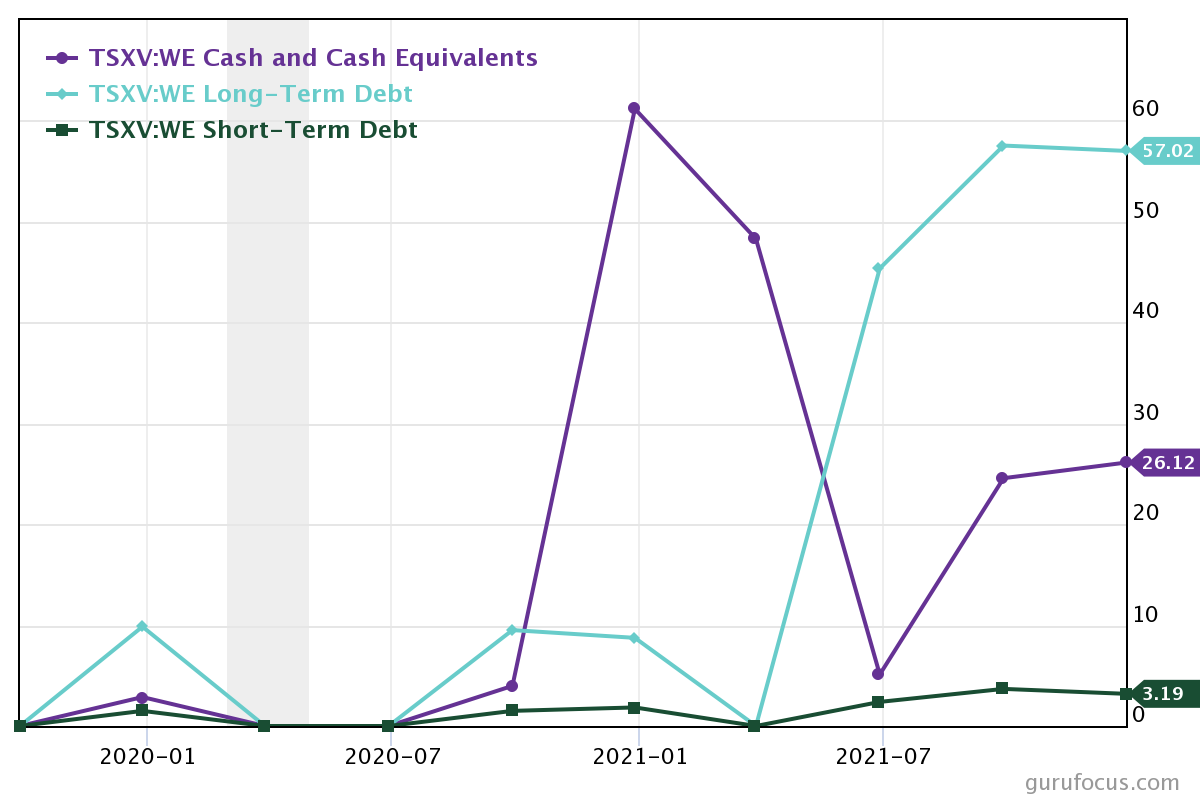

Taking a look to the balance sheet, they presently stand with 26.2 million in cash at quarter end, 59 million in long term debt ($3 m short term). This is not an ideal mix at this point. My concern would be they need to raise capital to balance the debt with equity in order to pursue more acquisitions.

Looking Ahead

Organic Growth

Insights into the forward organic growth were mixed. Specific key metrics within the portfolio businesses were good, including Stamped average revenue per user (ARPU) increased by 20%. They do not expect the acquisition of Knocommerce to contribute meaningfully to the business this year, rather they see it as a longer term play to scale. 2022 Shopify new merchants projections have been revised lower and that will have a more significant impact on Themes compared to the other segments.

Acquisitions

There are supposedly 1000 companies in the active pipeline for future acquisitions. Valuations have been coming down and management is hopeful that issued letters of intent can transform into deals soon. The pipeline represents north of $100 m in annualized revenue. It was noted that competition for acquisitions have increased with a couple of announced private companies but nothing directly competing with their deals yet.

I think that the most insightful and meaningful comment was that in the short term, the acquisitions will be focused on “tuck-in” acquisitions. I believe there could be multiple reasons for this:

Valuations will be hit hardest for smaller and less robust software businesses

The balance sheet doesn’t currently support large acquisitions without raising further capital by issuing shares

The share price is relatively low and investors sentiment is near recent history lows for small software and ecommerce businesses so they will likely not get a good price for equity (a lot of dilution)

Further debt may not be possible at favorable terms in the near-term

I believe that the short term focus on smaller tuck-in acquisitions is the right thing to do for the business and for shareholders. There is still some risk that they need to issue shares in the near future.

Current Valuation

The biggest risk to valuation from here will be dilution from a share issuance in my opinion. The apps segment is strong and growing and the lower quality agency business is a shrinking part of the business. Some of these underlying businesses have very high margins at scale and I believe normalized EBITDA margins to be around 30% and could improve over the longer term.

On an price to operating cash flow ratio, you are getting the stock at 25x currently (4% yield). The growth in cash flows should continue to be high even with some dilution. It has been growing 70%+ annualized but if you factor for dilution, this is much less. I think per share growth can sustain 20%+ but only time will tell. The good news is that there is a very long runway for growth with what they are trying to do and the key will be in the execution.

Note: I use Stratoshphere to help with my research, to follow my holdings, screen for ideas and get insights to company specific KPI’s that drive the business results. I also use it for charting in my content to visualize data. Get 25% off a great stock research platform, stratosphere.io

That’s it for now, check back soon for more. As always, follow me on twitter and please share this with anyone who might interested in my work.

Disclaimer: I own shares in this business. This is not intended to be advice of any kind.