Xpel $XPEL

Leading a niche business and an incredible 7,700% return in 5 years

Founded in 1997 and headquartered in Texas, this small but emerging business has been around for over twenty years and over its history has been a tremendous value to its long term shareholders. It has been a favorite among microcap investors due to its compelling growth and profitability over the past few years returning incredible returns for those capable of holding on for a few years. It is currently listed on the Nasdaq under the ticker XPEL and has a market cap of 2.4 billion and a enterprise value of slightly less (no net debt).

Stock Price Chart History")

What do they do?

They provide products and services related to protective coatings and films. Traditionally, they targeted the automotive industry but have since moved into other segments such as screen protection for electronics, business office space window protection and other related areas.

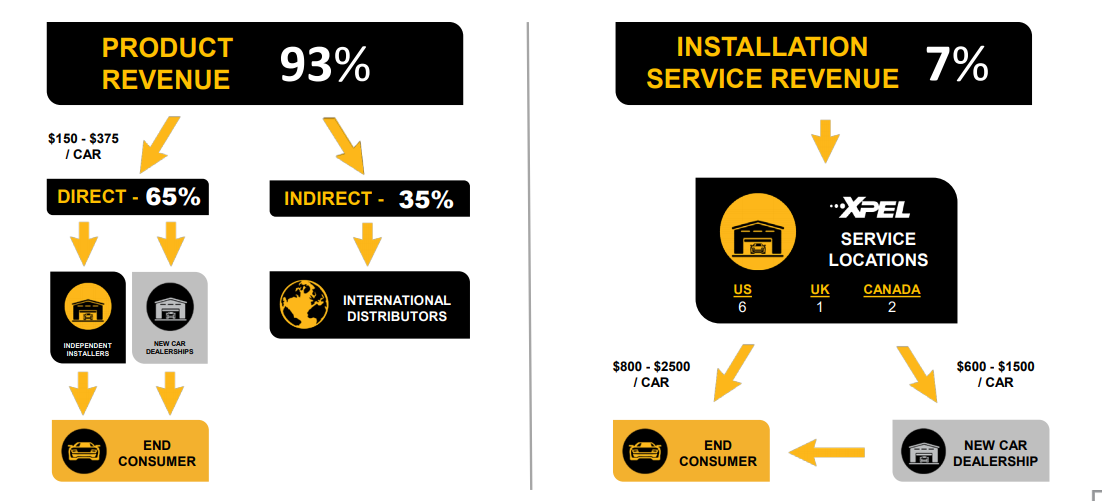

On the surface (hehe) it seems like a boring business. Maybe it is, but it has been an amazing niche that has propelled their growth for the last 10 years tremendously. They sell their products both directly to installers and dealers as well as through international distributors. This makes up the vast majority of revenues. They also have some service locations to service customers directly or through the dealers. Its not a crazy complex business model by any means.

(source: June 2021 Investor Presentation from Xpel Inc.)

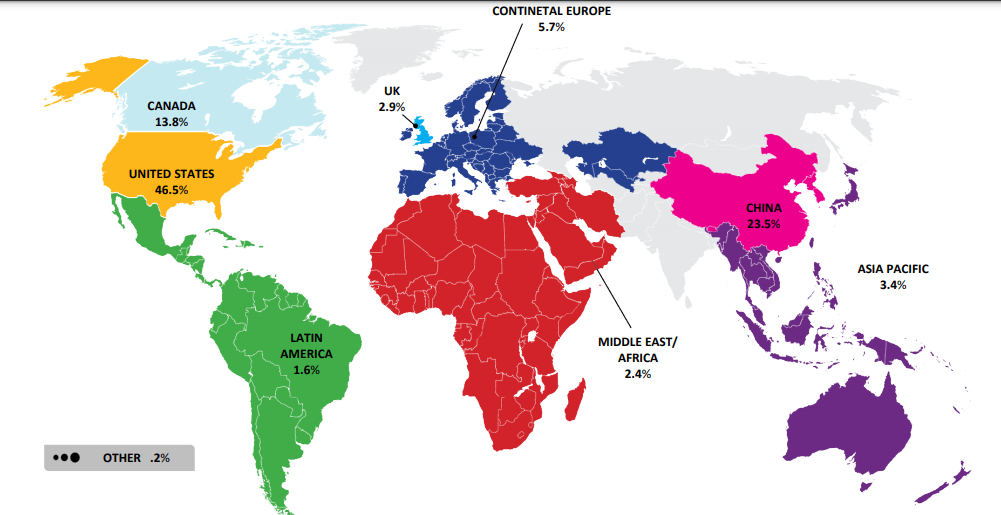

They have said to have strategic plans to continue their growth trajectory via international expansion as well as into related end uses (windows, electronics protective films, etc.). Interestingly, their sales are still over half from North America however, China is closing in on almost 25% of sales. If they can continue to grow in these global markets, there is much growth ahead still.

Do they make money?

Yes! They have managed to generate significant free cash flow over the past 6 years and it continues to grow. The top line revenue has grown at greater than 30% for past 5 years while the free cash flow has grown significantly higher rates as margins have expanded.

The business seems to be of good quality as the ROE has been 40%+ over past several years and the company has not had to take on significant debt to get these returns. The incremental ROIC in the past few years has been very good at anywhere from 10%ish to 50-60% fairly regularly. The gross margins have been consistently near 30% and slowly increasing over the past few years.

(source: June 2021 Investor Presentation from Xpel Inc.)

Is there a risk of a blow up?

The company has no net debt and is generating plenty of free cash flow. I believe it is safe to say “no” and move on for this one. People will continue to cherish their cars and see value in protecting them with a fairly small upfront cost for these products. Unless there are significant changes to wastefulness and ill-advised bad acquisitions, it seems unlikely that the company will blow up.

Is management sketchy?

Management has strong insider ownership of the business at around a third of the outstanding shares. They have issued a small amount of shares over the past few years but nothing to write home crying about compared with the reinvestment into the business. Now that the business is generating plenty of cash flow, it will be nice to see the company never issue significant shares and potentially buy back if the price lags the fundamentals. Management has been wise with its capital allocation so far and the numbers for returns on invested capital reflect this skill. They continue to focus on growth which for now, seems like a wise choice given the unpenetrated markets internationally as well as the improving margins and free cash flows.

Does it have a moat?

I would say YES, for now at least. ROE of 40-50% year in and year out. Very little leverage to do so. Probably at least a few years of growth ahead. It would seem like an attractive business to try to take market share away from. That being said, there is a certain brand that they have managed to garner respect for. The fact that they deal with mainly dealerships in terms of generating their revenues is probably a good thing as it is likely to be a sticky business. A network of dealerships in certain regions are likely to recommend to other dealers in other areas and are not likely to move onto other products given the relatively low cost compared to the sale of a vehicle.

In the long run, it might be questionable whether they can successfully fend off competition but for now they are still a small business and it would be somewhat challenging for a new entrant to build the scale at which Xpel is starting to enjoy. That being said, at least for now, the business is still niche enough for it not to be a worthwhile venture for large corporations to bother trying to compete with.

Is it cheap?

On most traditional metrics, it is definitely NOT cheap. With a price to sales of 13 times, it is valued similar to a high margin software as a service company. It does however (unlike some SaaS names) have real earnings and predictable free cash flows. This one might be more akin to buying a Volvo as opposed to an Oldsmobile (a cheapo for those too young to know what that is). If the growth is sustainable for the next 10 years, this price is not outrageous at all and could provide more than adequate returns.

One potential option for those looking for a bargain would be to leave this one on a close watch list and wait for a bit of a crash. These types of high flyers do tend to over-correct sometimes but if you believe in the business long term, it would be one that you would be willing to pull out of the ditch.

Final thoughts:

While this company has enjoyed much success lately and even more-so its shareholders, there is some potential for some future growth that could keep pushing the value higher. The fundamentals of the business seem to be getting better as it grows and expands to deeper and broader markets. It has good aligned insider ownership and enjoys the benefits of a niche business that can continue to scale. If you can evaluate the duration of the growth trajectory and are happy with managements’ direction, this one could be one to hold on to. If you think its a little too pricy, I wouldn’t blame you for waiting for a better opportunity, but don’t blink or you may miss it.

Disclosure: I currently own 100 shares in a personal account as of the time of publishing. As always, this is not intended to be financial advice (or advice of any kind), please do your own due-diligence!

Hit me up on twitter for any feedback or ideas @MoS_Investing