Texas Instruments $TXN

A Lollapalooza in plain sight

Note: this article was originally published as part of a multi-writer holiday collaboration earlier in December 2023. I thought I would re-publish it alone to my own platform for free for everyone who may not have seen it. I hope you enjoy.

Texas Instruments: A Lollapalooza in Plain Sight

Texas Instruments is a high quality business undergoing a critical capital intensive investment cycle. I believe TXN 0.00%↑ may be a beneficiary of very simple (with hindsight) Lollapalooza effects over the next decade. Markets tend to be short sighted and therefore are undervaluing the investment which is long term in nature.

I bought the three main text books for introductory psychology and I read through them. And of course being Charlie Munger, I decided that the psychologists were doing it all wrong, and I could do it better. And one of the ideas that I came up with which wasn’t in any of the books was that the Lollapalooza effects came when 3 or 4 of the tendencies were operating at once in the same situation. I could see that it wasn’t linear, you’ve got Lollapalooza effects. But the psychology people couldn’t do experiments that were 4 or 5 things happening at once because it got too complicated for them and they couldn’t publish. So they were ignoring the most important thing in their own profession.

- Charlie Munger

For those unfamiliar, Texas Instruments manufactures and sells analogue chips (mostly). They are essential in sensing the real world and converting this signal for use in computing, control systems, and automation processes in many end uses. They are used in a plethora of end industries such as manufacturing and automotive. They are the “old” tech compared to digital chips and are slow moving and not cutting age in comparison.

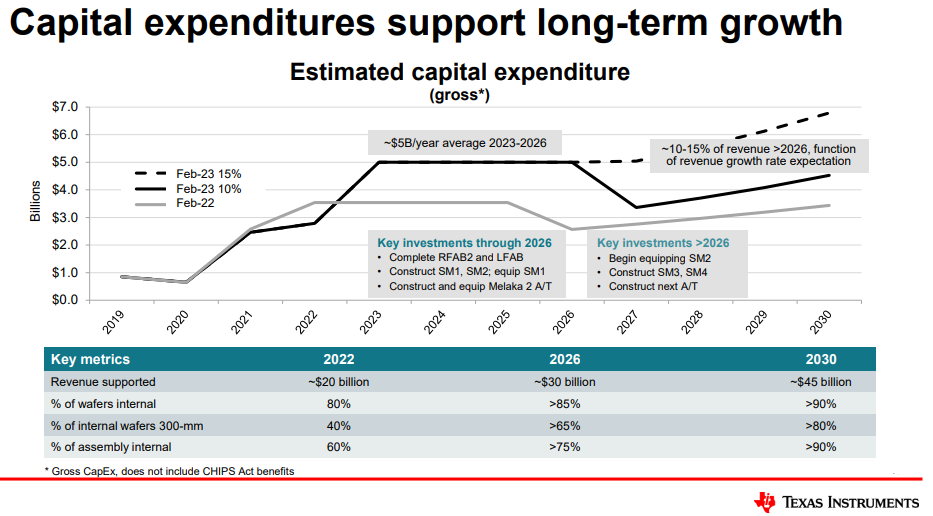

Texas Instruments is planning to reinvest heavily in new manufacturing facilities over the next 3-5 years, in addition to allocating capital to share repurchases and dividends. Some will be skeptical of such high capital expenditures but these are long lived investments that are not constant drags on future capital (as can be demonstrated by previous years operations and capital expenditures).

Lollapalooza Recipe

Pricing Power

End applications are going to become more valuable to the customer

Volume Growth

End applications will increase in quantity with automation, computing power, AI/ML increases in its effectiveness.

Operating Leverage

Expenses reduction per unit sales as replacement ordering will become more plentiful due to 1 and 2 above (more re-occurring sales over the lifetime).

Terminal Value Increases

As capex cycle comes to an end, free-cash will ramp up. Markets are too short sighted to value this properly.

Competitive Position Improvement

These changes will occur slowly enough and be costly enough to avoid an in-rush of new competition chasing returns. With the growth of the market, their competitive position should increase.

Risks

Large capital projects are inherently risky in terms of execution schedule and budget.

There is a large portion of sales (about half) in the Chinese end market geography. Geopolitics is a risk.

Valuation

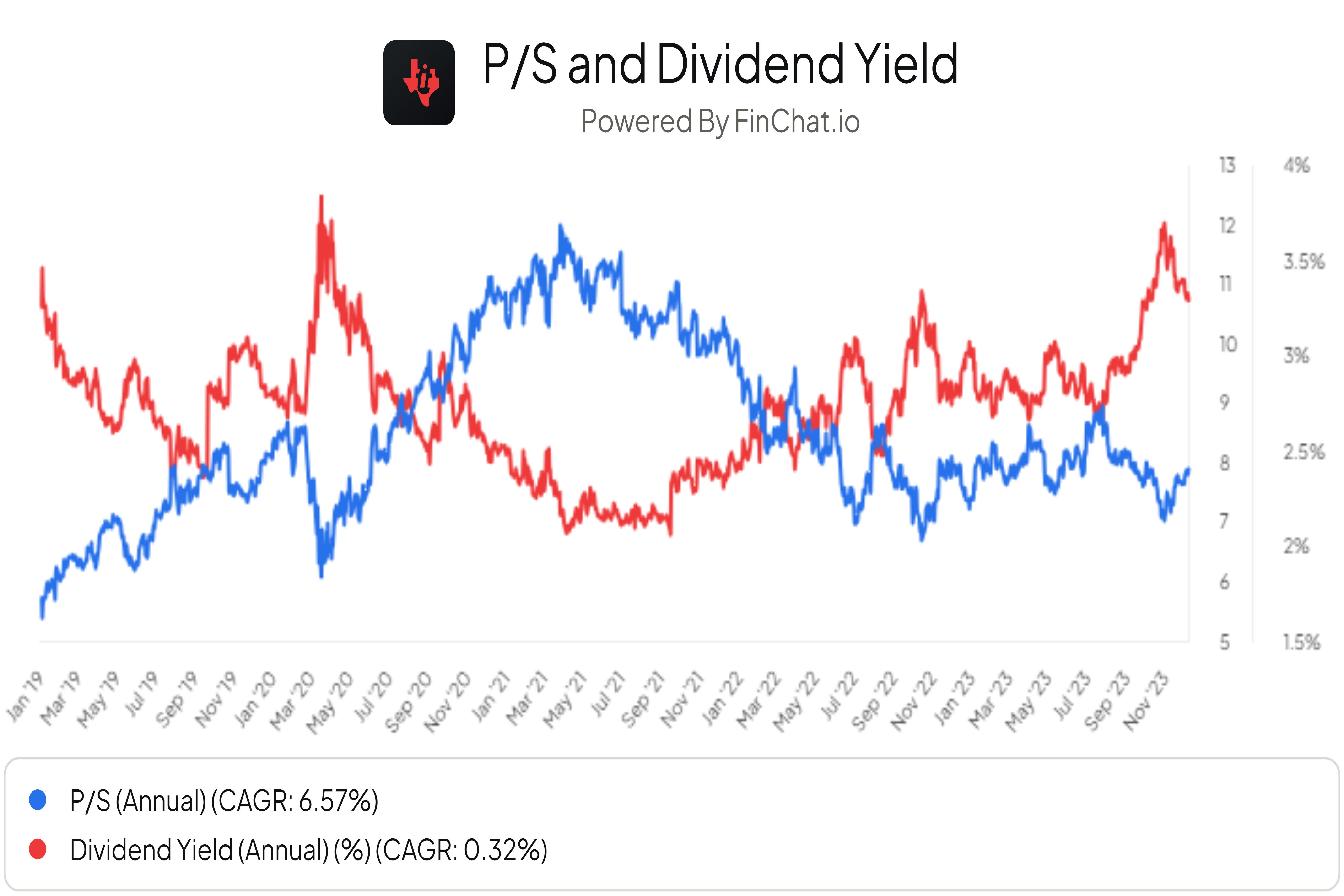

Given the capital investments underway, looking at current earnings is likely not a good measure necessarily. Looking at dividend yield and p/s compared to its own history may give you some clue as to whether it is cheap here or not. The valuation doesn’t appear screaming cheap on the surface but if you believe in the above thesis to any extent and are willing to hold multiple years to allow the thesis to play out, you may end up with a very good result with limited risk along the way.

That’s it for now. As always, let me know what you think. A like or a share with others who might enjoy my content is always very much appreciated.

Simon

Good points.